What is governmental auditing? A 2026 expert guide

- Леонид Ложкарев

- Mar 13

- 9 min read

Updated: Mar 31

Many audit professionals assume governmental auditing is solely about catching financial errors. In reality, it encompasses a broader mission: ensuring public accountability, optimizing government performance, and strengthening governance frameworks. This guide clarifies the standards, practices, and strategic benefits that define governmental auditing in 2026, equipping compliance professionals with actionable insights to enhance organizational integrity and meet evolving regulatory demands.

Table of Contents

Key takeaways

Point | Details |

GAGAS standards foundation | GAGAS establishes standards for auditor conduct and reporting to enhance accountability with public funds. |

Single Audit threshold | Entities expending over $1 million in federal awards must undergo a Single Audit starting fiscal years after October 1, 2024. |

Performance auditing ROI | Every $1 spent yields $12 in savings by identifying inefficiencies and improper payments. |

CPE compliance requirement | Auditors must complete 80 hours of CPE every two years, with 24 hours focused on government auditing topics. |

Audit planning importance | Proper planning forms the backbone of successful public financial audits and prevents costly errors. |

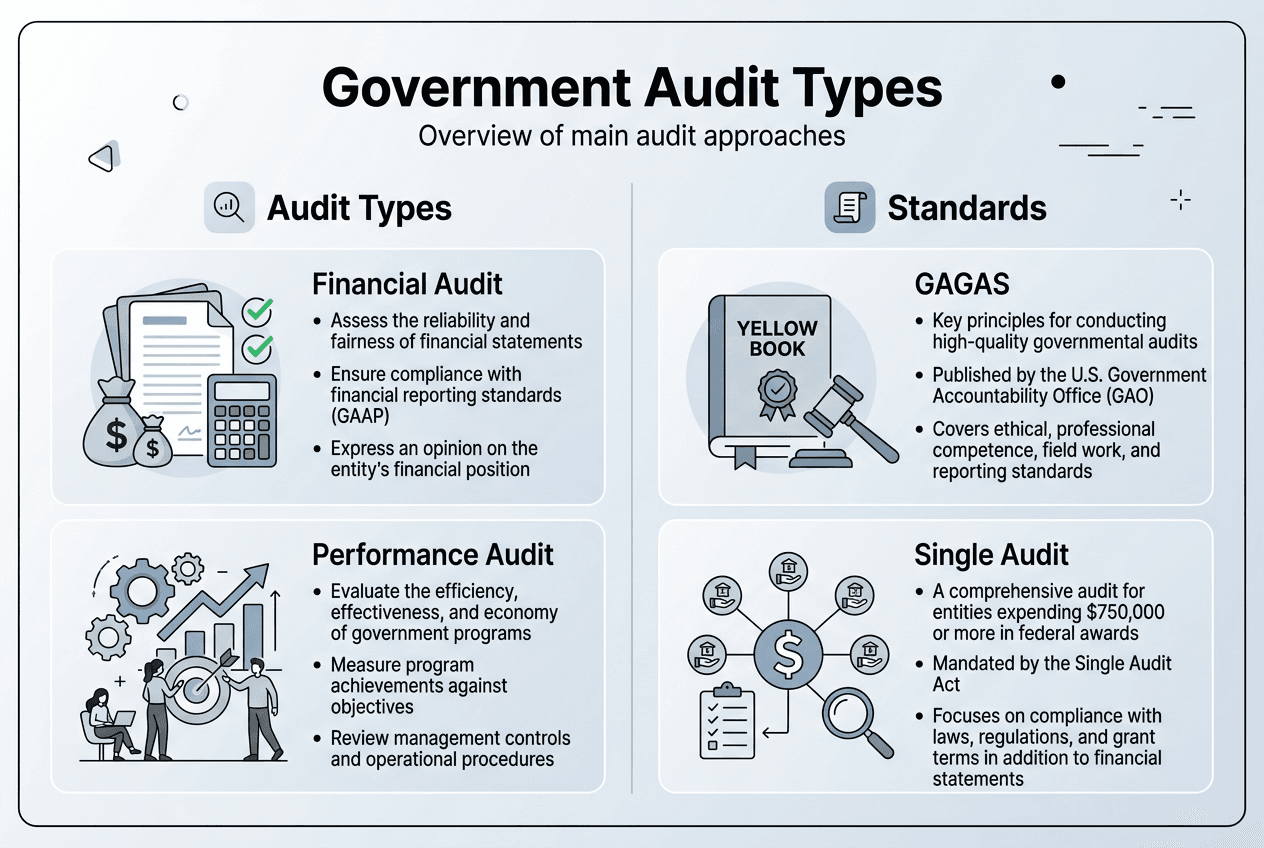

Understanding governmental auditing and its standards

Governmental auditing involves systematic examination of financial records and compliance to improve transparency. Unlike private sector audits focused primarily on financial accuracy, governmental audits serve a broader public accountability mandate. They encompass financial statement audits, performance evaluations, and compliance reviews designed to protect taxpayer interests and strengthen democratic governance.

The scope extends beyond balance sheets. You assess whether government programs operate economically, efficiently, and effectively. You verify compliance with laws and regulations. You identify opportunities to save costs and improve service delivery. This multidimensional approach requires specialized knowledge of public sector environments and regulatory frameworks.

GAGAS establishes standards for auditor conduct and reporting to enhance accountability with public funds. Known as the Yellow Book, GAGAS provides the ethical and professional framework that distinguishes governmental auditing from commercial practice. It mandates stricter independence requirements and more comprehensive reporting obligations.

Five core ethical principles anchor GAGAS standards:

Professional behavior that upholds the profession’s reputation

Objectivity free from conflicts of interest

Integrity in all professional relationships

Serving the public interest above private gain

Proper use and protection of information

Auditor independence remains non-negotiable. You must maintain independence both in fact and appearance. Even the perception of bias undermines audit credibility and erodes public trust. This requirement shapes every aspect of engagement planning, execution, and reporting.

“Independence is the cornerstone of auditing. Without it, audit findings lose their power to drive meaningful change and accountability.”

These standards create a foundation that ensures audits deliver reliable, actionable insights. They protect both auditors and the organizations they serve by establishing clear expectations and ethical guardrails. For audit professionals attending government auditor events, mastering GAGAS principles is essential for career advancement and audit quality.

The critical role of Single Audits in federal fund oversight

Single Audits represent a specialized audit type that directly impacts organizations receiving federal funding. The threshold is $1 million in federal awards expended for fiscal years starting after October 1, 2024. This threshold increase from previous levels affects planning for many nonprofits, universities, state agencies, and local governments.

Entities below the threshold avoid the Single Audit requirement but must still comply with specific federal award terms and conditions. However, crossing that $1 million mark triggers comprehensive audit obligations that examine both financial statements and federal program compliance. The Schedule of Expenditures of Federal Awards becomes the roadmap, listing every federal dollar received and expended.

Understanding threshold changes is crucial for 2026 planning:

Fiscal Year Start | Threshold | Audit Requirement |

Before Oct 1, 2024 | $750,000 | Single Audit mandatory |

On/After Oct 1, 2024 | $1,000,000 | Single Audit mandatory |

Below threshold | Any amount | Exempt but must comply with award terms |

Single Audit findings trigger serious consequences, including potential waste, fraud, and abuse investigations. Material weaknesses in internal controls can lead to questioned costs, requiring repayment of federal funds. Repeat findings escalate oversight and may result in grant terminations or debarment from future federal awards.

Common Single Audit deficiencies include:

Inadequate subrecipient monitoring

Missing or incomplete procurement documentation

Payroll allocation errors for personnel charged to grants

Failure to reconcile financial records with federal reports

Late submission of required reports

Pro Tip: Maintain a centralized federal compliance calendar tracking all reporting deadlines, monitoring requirements, and audit milestones. This simple tool prevents missed deadlines and demonstrates proactive compliance management to auditors.

The key to Single Audit success lies in robust preventive controls rather than reactive fixes. Document your processes meticulously. Implement regular internal compliance reviews throughout the year. Train staff on federal requirements specific to each program. Understanding continuing professional education importance helps your team stay current on evolving compliance standards and avoid costly findings.

Leveraging performance auditing to enhance government efficiency

Performance auditing shifts focus from financial accuracy to operational effectiveness. While financial audits ask “Are the numbers correct?”, performance audits ask “Are we getting value for money?” This proactive approach evaluates the economy, efficiency, and effectiveness of government programs and operations.

The impact is substantial. Every $1 spent on performance auditing yields $12 in savings by identifying waste, redundancies, and process improvements. These audits uncover billions in potential recoveries. Federal agencies face challenges with 92% lacking real-time performance data for decision making, making systematic auditing essential for informed governance.

Performance auditing delivers value through multiple dimensions:

Identifying improper payments estimated at $64 billion annually across federal programs

Revealing process bottlenecks that delay service delivery

Benchmarking performance against industry standards or peer organizations

Testing whether programs achieve intended outcomes

Recommending evidence-based improvements

Unlike compliance-focused audits, performance work requires deep analytical skills and creative problem-solving. You examine root causes, not just symptoms. You develop recommendations that transform operations, not just fix isolated errors. This audit type drives continuous improvement and positions audit functions as strategic advisors rather than compliance checkers.

“Performance auditing transforms the audit function from a watchdog to a catalyst for positive change, delivering measurable improvements in how government serves citizens.”

Pro Tip: Integrate advanced data analytics tools into your performance audit methodology. Automated analysis of large datasets reveals patterns and anomalies impossible to detect through manual sampling, dramatically improving audit effectiveness and insight quality.

The scope of performance auditing extends to program evaluation, cybersecurity assessments, and operational reviews. You might examine whether a workforce development program actually improves employment outcomes. You could assess whether IT investments deliver promised efficiencies. These audits answer questions that matter to taxpayers and policymakers alike.

For professionals exploring auditing standards examples for leaders, performance auditing represents the frontier of public sector accountability. It requires mastery of qualitative and quantitative methods, stakeholder engagement skills, and the ability to communicate complex findings to diverse audiences.

Best practices and planning for effective governmental audits

Audit planning forms the backbone of successful public financial audits. Inadequate planning leads to scope gaps, missed risks, and findings that fail to withstand scrutiny. Effective planning requires understanding the audited entity’s environment, risks, and control systems before fieldwork begins.

Start by gathering intelligence. Review prior audit reports, budget documents, organizational charts, and relevant legislation. Interview key personnel to understand operational realities and emerging challenges. This reconnaissance phase reveals material risks and guides resource allocation.

A systematic audit planning process includes these essential steps:

Define audit objectives and scope based on risk assessment and stakeholder needs

Understand the entity’s internal control environment and identify potential control weaknesses

Assess fraud risks considering incentives, opportunities, and rationalization factors

Develop detailed audit programs with specific procedures tied to objectives

Allocate resources and establish timelines with realistic milestones

Communicate the audit plan to entity management and address concerns proactively

Build in quality control checkpoints throughout the engagement

Risk assessment improves both audit efficiency and credibility. You focus resources on areas with highest risk of material misstatement or noncompliance. This targeted approach delivers deeper insights while respecting budget constraints. It also demonstrates professional judgment and strategic thinking.

Common pitfalls undermine even well-intentioned audits:

Failing to update risk assessments when conditions change mid-engagement

Insufficient documentation of audit rationale and methodology

Inadequate supervision of audit team members

Poor communication with auditee throughout the process

Relying on outdated audit programs without customization

Ignoring red flags that emerge during fieldwork

Quality control mechanisms protect audit integrity. Implement multi-level review processes for workpapers and reports. Use standardized templates and checklists to ensure consistency. Conduct post-audit retrospectives to identify improvement opportunities. These practices build confidence that audit conclusions rest on solid evidence and sound reasoning.

Documentation serves multiple purposes. It provides evidence supporting findings and conclusions. It facilitates supervisory review and quality control. It creates a record for future audits and external peer reviews. Comprehensive, well-organized workpapers demonstrate professionalism and protect against challenges to audit conclusions.

For professionals seeking hands-on skill development, auditing business applications training and audit quality and workpapers training provide practical frameworks for executing audits that meet GAGAS standards. These programs bridge the gap between theoretical knowledge and real-world application.

Boost your auditing skills with expert CPE training

Mastering governmental auditing requires continuous learning as standards evolve and new challenges emerge. Staying current with GAGAS requirements, emerging technologies, and best practices separates competent auditors from exceptional ones.

Our comprehensive CPE seminars equip you with cutting-edge knowledge in governmental auditing, ethics, cybersecurity, and compliance frameworks. Designed specifically for audit and compliance professionals, our training helps you maintain the 80 hours of CPE every two years that GAGAS mandates. We offer flexible learning through live webinars and in-person events across multiple cities, fitting professional development into your schedule.

Expert instructors with Big 4 backgrounds deliver practical, standards-based instruction that you can apply immediately. Our curriculum covers internal and external auditing standards, internal control frameworks, and industry-specific compliance topics for government sectors. Whether you need foundational knowledge through internal auditing 101 training basics or specialized skills via internal auditor CPE webinars, we provide training that elevates your audit quality and career trajectory.

Explore our 2026 CPE event calendar to find upcoming training opportunities that align with your professional development goals and help you stay ahead of evolving governmental auditing standards.

What is the difference between governmental auditing and financial auditing?

Governmental auditing encompasses financial, compliance, and performance audits specifically designed for public sector accountability. It extends beyond verifying financial statement accuracy to evaluate whether government entities use resources economically, efficiently, and effectively. This broader scope reflects the public interest dimension absent in private sector work.

Financial auditing focuses primarily on whether financial statements present fairly in accordance with applicable accounting standards. While financial audits form part of governmental auditing, they represent only one component. Governmental audits additionally examine compliance with laws and regulations, assess internal controls over operations, and evaluate program outcomes.

Governmental audits follow GAGAS standards with additional public interest emphasis, requiring stricter independence standards and more comprehensive reporting than generally accepted auditing standards. These enhanced requirements recognize that governmental audits serve diverse stakeholders including taxpayers, legislators, oversight bodies, and the public, not just management and investors.

Who must comply with Single Audit requirements in 2026?

Entities expending $1 million or more in federal funds during a fiscal year must undergo a Single Audit. This threshold applies to fiscal years starting on or after October 1, 2024, representing an increase from the previous $750,000 threshold. Organizations below this threshold remain exempt from Single Audit requirements but must still comply with specific terms and conditions of their federal awards.

Covered entities include nonprofits, universities, state agencies, local governments, and tribal organizations receiving federal assistance. Noncompliance triggers serious consequences including potential loss of current and future funding, increased federal oversight, and required repayment of questioned costs. Repeat findings can result in debarment from federal programs.

What continuing education requirements must governmental auditors meet?

Auditors must complete 80 hours of CPE every two years to comply with GAGAS standards. Of these 80 hours, at least 24 must directly relate to the government environment, government auditing, or the specific audit being performed. The remaining hours should enhance professional proficiency relevant to audit responsibilities.

CPE ensures auditors remain current on evolving standards, emerging risks, and new auditing techniques. Topics should include updates to GAGAS, changes in accounting standards, developments in information technology, and emerging fraud schemes. Understanding CPE credits importance for auditors helps you structure learning strategically.

Failure to meet CPE requirements jeopardizes audit credibility and professional standing. Auditors who fall short cannot claim GAGAS compliance for their work, potentially invalidating audit reports and exposing both auditors and their organizations to legal and professional consequences. Documentation of CPE completion is essential for peer reviews and quality control inspections.

Recommended

Comments