Internal controls implementation guide for audit pros 2026

- Леонид Ложкарев

- Mar 13

- 10 min read

Internal controls are the backbone of strong governance, yet many organizations struggle to implement them effectively. Without a clear roadmap, audit and compliance professionals often face resistance from management, inadequate documentation, and controls that fail under pressure. This guide provides a practical, step-by-step framework to help you design, execute, and verify internal controls that actually work. You’ll learn how to avoid common pitfalls, engage stakeholders, and build a resilient control environment that protects your organization from financial and operational risks while meeting regulatory requirements.

Table of Contents

Key takeaways

Point | Details |

Structured approach | Implementing controls requires preparation, execution, and verification phases to ensure effectiveness. |

Team alignment | Success depends on clear roles, management support, and communication across all stakeholders. |

Continuous monitoring | Regular evaluation and refinement sustain control effectiveness and adapt to evolving risks. |

Common pitfalls | Avoid failures by addressing management buy-in, training gaps, and overly complex control designs. |

Technology leverage | Automation and monitoring tools improve efficiency, accuracy, and compliance tracking. |

Understanding the basics: What you need before implementing internal controls

Before you start implementing internal controls, you need a solid foundation. Internal controls are processes and procedures designed to provide reasonable assurance that your organization achieves its objectives in operational effectiveness, reliable financial reporting, and compliance with laws and regulations. They play a critical role in governance by mitigating risks and protecting assets.

Your implementation team should include key stakeholders from multiple departments. Assign a project lead, typically from internal audit or compliance, who coordinates activities and reports to senior management. Include control owners from finance, operations, IT, and other relevant areas who will execute and maintain controls daily. Risk managers provide expertise in identifying and prioritizing threats, while legal and compliance advisors ensure alignment with regulatory requirements.

You’ll need specific resources before launching your implementation. Documentation templates for policies, procedures, and control matrices streamline the process. Risk assessment tools help identify and prioritize control gaps. Internal control in banking frameworks provide industry-specific guidance, and foundational knowledge and team composition are vital for implementation success. Project management software tracks milestones, responsibilities, and deadlines.

Compliance standards and frameworks guide your control design. The COSO framework remains the gold standard, offering five integrated components: control environment, risk assessment, control activities, information and communication, and monitoring activities. For public companies, Sarbanes-Oxley Section 404 mandates specific internal control requirements over financial reporting. Industry-specific regulations like FDICIA for banks or HIPAA for healthcare organizations add additional layers.

Essential resources for implementation:

Risk assessment methodologies and tools

Control documentation templates and matrices

Training materials for control owners

Monitoring and reporting dashboards

Compliance framework guidelines (COSO, SOX)

Top management support makes or breaks your implementation. Without executive buy-in, you’ll struggle to secure resources, enforce accountability, and overcome resistance. Schedule early meetings with C-suite leaders to present your business case, emphasizing how controls reduce risk exposure, improve operational efficiency, and protect the organization’s reputation. Secure a formal mandate that empowers your team to access information, interview personnel, and implement changes across departments.

Pro Tip: Create a control implementation charter signed by senior management that defines scope, authority, resources, and success metrics. This document serves as your mandate when facing resistance or resource constraints.

Key roles and responsibilities:

Role | Primary Responsibilities |

Project Lead | Coordinates implementation, reports progress, resolves conflicts |

Control Owners | Execute daily controls, document activities, report issues |

Risk Managers | Identify threats, prioritize controls, assess residual risk |

Management | Provide resources, enforce accountability, remove barriers |

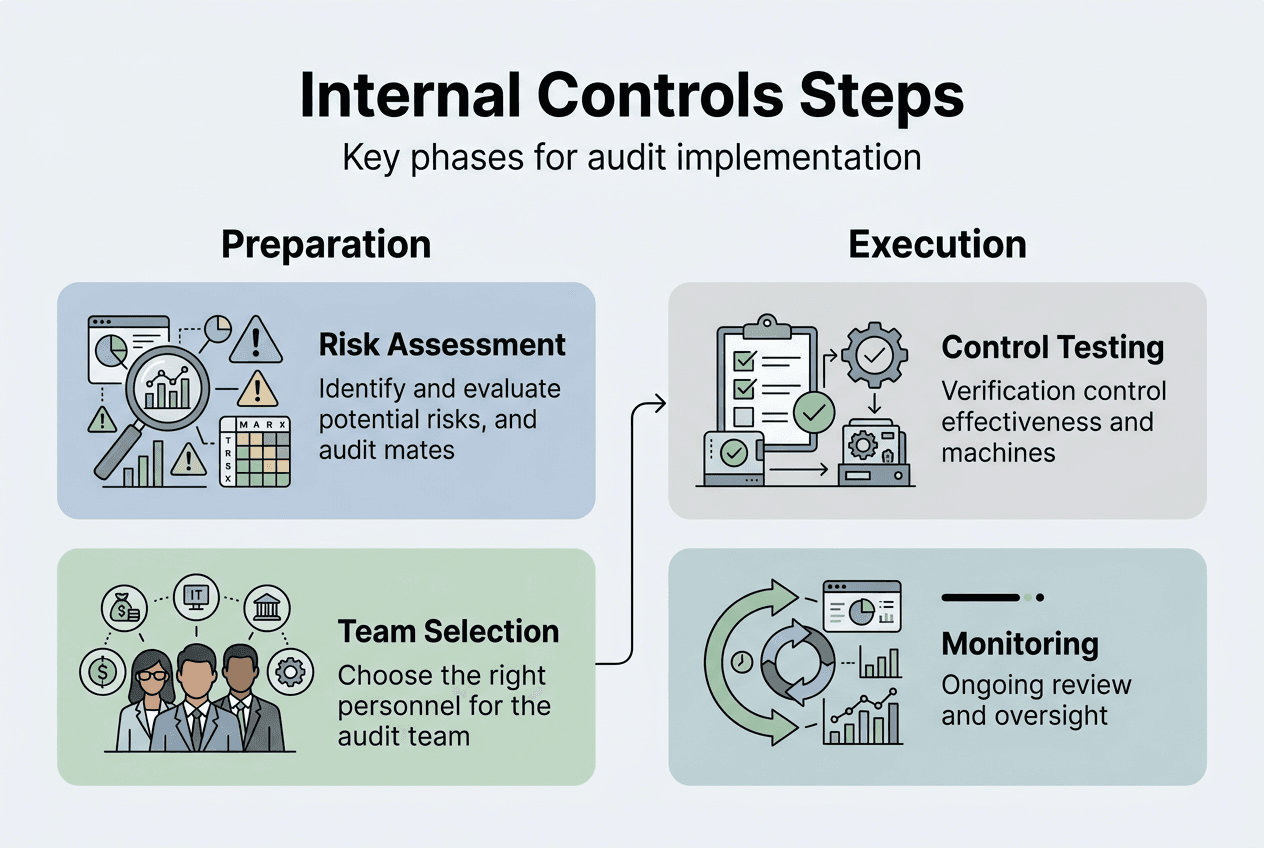

Step-by-step process for executing internal controls implementation

Start with a comprehensive risk assessment that identifies and prioritizes threats to your organization’s objectives. Interview department heads, review historical incidents, analyze industry trends, and examine regulatory changes. Document each risk’s likelihood and potential impact, then map existing controls to see where gaps exist. This assessment becomes your roadmap for designing targeted controls that address your highest priorities.

Design controls that are proportionate to the risks they address. For high-impact financial reporting risks, implement segregation of duties, dual authorization, and reconciliation procedures. For operational risks, consider automated system controls, physical safeguards, and supervisory reviews. Document each control’s objective, frequency, responsible party, and evidence of execution. A clear, structured rollout process improves control adoption and effectiveness.

Implementation sequence:

Conduct comprehensive risk assessment across all business processes

Design controls mapped to identified risks and control objectives

Document control procedures, responsibilities, and evidence requirements

Develop training programs for control owners and process participants

Execute pilot testing in selected departments before full rollout

Launch organization-wide implementation with phased approach

Establish monitoring mechanisms and reporting protocols

Review and refine controls based on initial performance data

Communication and training are critical during execution. Control owners need to understand not just what to do, but why controls matter and how they fit into the broader risk management strategy. Develop role-specific training modules that include real-world scenarios, common mistakes, and best practices. Use multiple formats: live workshops for complex topics, video tutorials for routine procedures, and quick reference guides for daily tasks.

Technology accelerates implementation and improves control reliability. Governance, risk, and compliance (GRC) platforms centralize control documentation, automate workflow approvals, and generate compliance reports. Robotic process automation handles repetitive control activities like data validation and reconciliation. Analytics tools identify anomalies and trends that indicate control weaknesses. Choose technology that integrates with your existing systems and scales as your control environment matures.

Coordinate your implementation with existing audit schedules to leverage resources efficiently. If internal audit plans to review accounts payable next quarter, prioritize implementing controls in that area first. This approach provides immediate validation of your control design and identifies issues while the implementation team is still engaged. It also demonstrates value to management by showing tangible improvements in audit findings.

Pro Tip: Create a control implementation dashboard that tracks completion status, identifies bottlenecks, and highlights risks requiring management attention. Update it weekly and share with stakeholders to maintain momentum and accountability.

Control documentation essentials:

Document Type | Key Contents |

Control Matrix | Risk, control objective, procedure, owner, frequency, evidence |

Process Narrative | Step-by-step workflow showing control points and decision criteria |

Training Materials | Role responsibilities, execution steps, common errors, escalation paths |

Evidence Repository | Standardized templates and storage location for control execution proof |

Continuous process review starts during implementation, not after. Schedule weekly team meetings to discuss challenges, share solutions, and adjust timelines. Collect feedback from control owners about practical difficulties executing procedures. Some controls that look good on paper prove unworkable in practice, requiring redesign before they become embedded in operations. Stay flexible and responsive during this critical phase.

Common challenges and troubleshooting during implementation

Lack of management buy-in derails more implementations than any technical issue. Middle managers resist controls they perceive as bureaucratic obstacles that slow down their teams. They question the value when controls reveal deficiencies in their departments. Combat this by involving managers early in control design, demonstrating how controls protect them from personal liability, and celebrating quick wins that show tangible benefits.

Poor communication creates confusion and resistance throughout the organization. Employees don’t understand why new procedures are necessary or how to execute them correctly. They revert to old habits because new controls seem arbitrary. Establish multiple communication channels: town halls for big-picture context, department meetings for specific impacts, and one-on-one coaching for complex roles. Repeat key messages consistently and address concerns promptly.

Typical implementation pitfalls:

Insufficient training leading to inconsistent control execution

Overly complex controls that employees circumvent or ignore

Inadequate documentation making controls impossible to verify

Missing segregation of duties creating fraud opportunities

Failure to monitor controls after initial implementation

Underestimating resource requirements for sustainable operation

Overcomplicating controls is a common mistake among well-intentioned professionals. You design elaborate procedures with multiple approval layers and extensive documentation requirements. The result? Controls become so burdensome that employees find workarounds or simply don’t comply. Keep controls as simple as possible while still achieving the control objective. A streamlined three-way match process that people actually perform beats a comprehensive ten-step procedure that exists only on paper.

Underestimating risk areas leaves critical gaps in your control environment. You focus resources on obvious financial reporting risks while overlooking operational and compliance exposures. Conduct thorough risk assessments across all business processes, not just accounting functions. Consider cybersecurity, vendor management, regulatory compliance, and reputational risks. Internal controls often fail due to common implementation errors and oversight risks.

Resistance from long-tenured employees poses unique challenges. They’ve done things a certain way for years and see no reason to change. They may have informal workarounds that bypass proposed controls. Address this by acknowledging their expertise, explaining how controls protect them and the organization, and involving them in refining procedures to incorporate their knowledge while maintaining control objectives.

“The most effective controls are those that employees understand and embrace as part of their daily responsibilities, not burdensome add-ons imposed from above. Successful implementation requires earning trust and demonstrating value at every level of the organization.”

Handling control deficiencies discovered during audits requires swift, systematic response. When auditors identify a control weakness, document the root cause immediately. Was the control poorly designed, inadequately communicated, or simply not executed? Develop a corrective action plan that addresses the underlying issue, not just the symptom. Assign responsibility for remediation, set deadlines, and track completion through your GRC platform.

Maintaining control integrity over time demands ongoing attention. Controls drift as personnel change, processes evolve, and new risks emerge. Establish a formal review cycle where control owners certify quarterly that procedures remain current and effective. Update documentation promptly when processes change. Conduct periodic walkthroughs to verify controls operate as documented. This discipline prevents the gradual erosion that undermines even well-designed control environments.

Verifying effectiveness: Monitoring and continuous improvement of internal controls

Monitoring begins the moment controls go live. Implement multiple layers of oversight to catch issues early. Control owners perform self-assessments, documenting their execution and identifying any deviations. Supervisors conduct periodic reviews, testing a sample of transactions to verify controls operated as designed. Internal audit provides independent assurance through scheduled and surprise audits.

Key performance indicators transform subjective assessments into objective metrics. Track control execution rates to identify procedures that employees struggle to complete consistently. Measure the timeliness of control activities, flagging delays that might indicate resource constraints or process inefficiencies. Monitor exception rates to spot trends suggesting emerging risks or control weaknesses. Calculate the cost of control activities to ensure resources are allocated efficiently.

Control effectiveness metrics:

Percentage of controls executed on time and completely

Number and severity of control deficiencies identified

Time required to remediate identified weaknesses

Cost per control activity relative to risk mitigated

Employee compliance rates with control procedures

Audit findings related to control design and operation

Manual monitoring relies on human judgment and periodic testing. Control owners maintain logs documenting their activities. Supervisors review these logs and test samples of transactions. Internal audit conducts detailed walkthroughs and substantive testing. This approach works for smaller organizations or controls that require professional judgment. However, manual monitoring is resource-intensive, provides limited coverage, and introduces human error.

Automated monitoring leverages technology to provide continuous, comprehensive oversight. System-generated reports flag transactions that violate control parameters. Analytics tools identify patterns indicating potential control failures. Exception dashboards alert management to issues requiring immediate attention. Automated monitoring scales efficiently, covers 100% of transactions, and eliminates human bias. The tradeoff is upfront investment in technology and ongoing maintenance.

Manual vs automated control monitoring:

Approach | Advantages | Limitations |

Manual | Exercises professional judgment, flexible to unique situations | Resource-intensive, limited sample coverage, human error risk |

Automated | Continuous coverage, scalable, eliminates bias | Requires technology investment, less flexible for judgment calls |

Feedback loops drive continuous improvement. Collect input from control owners about practical challenges executing procedures. Analyze audit findings to identify systemic issues requiring control redesign. Review incidents and near-misses to determine whether existing controls failed or gaps exist. Hold quarterly control committee meetings where stakeholders discuss performance metrics, emerging risks, and improvement opportunities.

Documenting changes maintains control integrity and audit trails. When you modify a control procedure, update the control matrix, process narratives, and training materials simultaneously. Communicate changes to affected personnel before implementation. Archive previous versions to maintain a historical record. This discipline ensures everyone works from current documentation and provides auditors with clear evidence of your control evolution.

Updating control frameworks regularly keeps pace with organizational and environmental changes. Review your control environment annually or when significant changes occur: new business lines, major system implementations, regulatory updates, or leadership transitions. Reassess risks to identify emerging threats requiring new controls. Eliminate controls that no longer address relevant risks. Continuous evaluation and refinement sustain internal controls’ effectiveness and compliance.

Pro Tip: Establish a control change management process that requires formal approval before modifying any control. This prevents well-intentioned but poorly considered changes that introduce new risks or create gaps in your control environment.

Enhance your skills with expert internal audit and compliance training

Mastering internal controls implementation requires staying current with evolving standards, frameworks, and best practices. Professional development through specialized training programs sharpens your technical skills and expands your strategic perspective. Whether you’re designing controls for the first time or refining an established program, targeted education accelerates your expertise and enhances your value to your organization.

Compliance Seminars offers comprehensive continuing professional education designed specifically for audit and compliance professionals. Access 2026 CPE event calendar featuring in-person seminars across multiple cities, or join flexible internal auditor CPE webinars that fit your schedule. For professionals building foundational knowledge, Internal Auditing 101 training basics provides practical frameworks you can apply immediately. Earn NASBA-recognized CPE credits while learning from industry experts with Big 4 backgrounds who deliver standards-based instruction grounded in real-world application.

FAQ

What is the first step in implementing internal controls?

The first step is conducting a comprehensive risk assessment to identify areas requiring control. This assessment evaluates threats to your organization’s objectives, prioritizes risks by likelihood and impact, and maps existing controls to reveal gaps. Starting with risk assessment ensures you design targeted controls that address your most critical exposures rather than implementing generic procedures that may not fit your specific needs.

How often should internal controls be evaluated after implementation?

Controls should be evaluated at least annually through formal reviews, with continuous monitoring occurring throughout the year. More frequent evaluation is necessary when significant changes occur: new regulations, major system implementations, organizational restructuring, or emerging risks. Quarterly management certifications and ongoing performance metrics provide interim checkpoints between annual comprehensive reviews.

What are the key reasons internal controls fail?

Control failures typically stem from inadequate management support, poor communication, and insufficient training for control owners. Overly complex procedures that employees circumvent or ignore also contribute to failure. Other common causes include underestimating resource requirements, failing to monitor controls after implementation, and not updating controls as processes evolve. Awareness of these pitfalls helps you design resilient controls and address issues proactively.

Can technology improve internal controls implementation?

Yes, technology significantly enhances implementation efficiency and control effectiveness. GRC platforms centralize documentation, automate workflows, and generate compliance reports. Robotic process automation executes repetitive control activities with greater accuracy than manual procedures. Analytics tools identify anomalies and trends indicating potential weaknesses. Automated monitoring provides continuous oversight across 100% of transactions, catching issues that sampling-based manual reviews might miss.

Recommended

Comments