What Is Audit Sampling? 5 Key Techniques for 2026 Auditors

- Леонид Ложкарев

- Mar 1

- 11 min read

Audit sampling allows auditors to examine as little as 1% of transactions and still draw reliable conclusions about entire populations. This technique transforms auditing from an exhaustive review into an efficient, standards-based process that balances assurance with resource constraints. In 2026, mastering audit sampling techniques is essential for both internal and external auditors working to meet regulatory requirements while managing practical limitations.

Table of Contents

Key Takeaways

Point | Details |

Audit sampling examines subsets | Auditors draw conclusions about entire populations by testing representative samples rather than all items. |

Two primary methods exist | Statistical and non-statistical sampling each serve different audit contexts and risk profiles. |

Standards govern sampling | PCAOB AS 2315 and IAASB ISA 530 establish requirements for proper sample design, selection, and evaluation. |

Sample size balances risk and efficiency | Larger samples reduce sampling risk but increase costs; optimal sizing requires careful calculation. |

Extrapolation drives conclusions | Projecting sample findings to the full population determines whether material misstatements exist. |

Introduction to Audit Sampling

Audit sampling involves selecting and evaluating a representative subset from a full population to form conclusions about the entire group. Rather than examining every transaction or control, auditors test carefully chosen samples that provide sufficient evidence while maintaining cost effectiveness. This fundamental approach allows firms to conduct quality audits without unlimited resources.

The primary purpose of sampling is reducing auditor workload and client costs while preserving audit quality and compliance with professional standards. Audit sampling improves efficiency by enabling reliable conclusions from partial populations, making it indispensable in modern auditing practice.

Common scenarios for audit sampling techniques include:

Testing internal controls over large transaction volumes

Verifying account balances with numerous individual items

Evaluating compliance with policies across multiple departments

Substantive testing of revenue or expense populations

The critical requirement is that samples accurately represent the population. Biased or unrepresentative samples undermine audit conclusions and increase the risk of undetected material misstatements. Auditors must design sampling plans carefully to ensure samples reflect population characteristics and provide valid evidence for audit opinions.

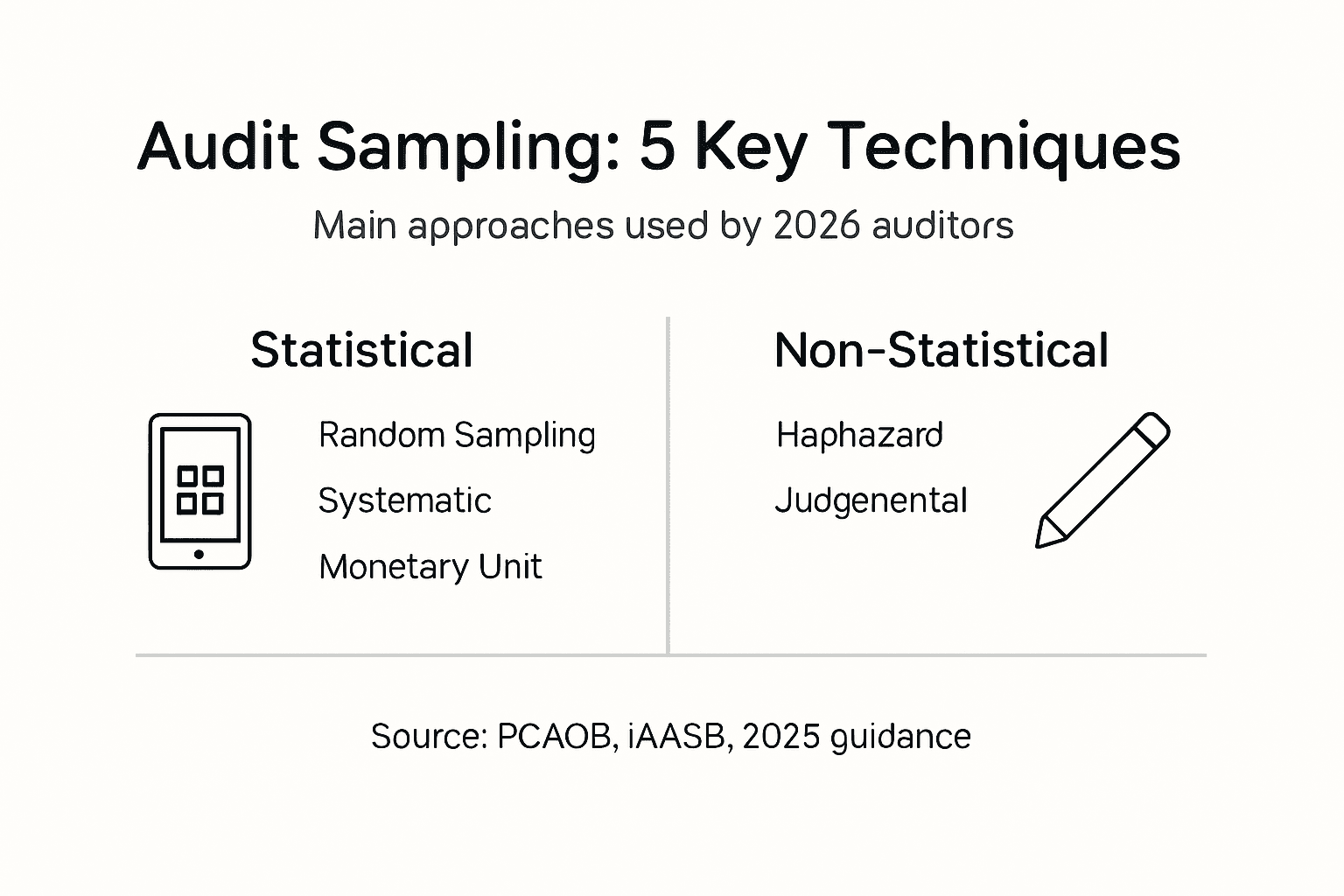

Types of Audit Sampling Techniques

Auditors choose between two fundamental approaches when designing sampling plans. Statistical sampling quantifies sampling risk, while non-statistical relies on auditor judgment without measuring risk precisely. Each method offers distinct advantages depending on audit objectives and circumstances.

Feature | Statistical Sampling | Non-Statistical Sampling |

Risk measurement | Quantifies sampling risk using probability theory | Cannot measure sampling risk numerically |

Sample selection | Random or systematic selection required | Judgment-based selection acceptable |

Best use cases | Large populations, high-risk areas, precise risk control | Smaller audits, low-risk areas, practical constraints |

Complexity | Higher complexity, requires statistical knowledge | Simpler, more intuitive for auditors |

Defensibility | Stronger statistical basis for conclusions | Relies on auditor expertise and documentation |

Statistical sampling uses probability theory to select items and allows auditors to calculate confidence levels and sampling risk. This approach provides mathematical support for audit conclusions and helps control sampling risk below specific thresholds, typically 5% or 10%. When audit standards require precise risk quantification, statistical methods become essential.

Non-statistical sampling relies on auditor judgment throughout the process. While this method cannot quantify sampling risk mathematically, experienced auditors can still achieve adequate assurance through careful planning and professional skepticism. The simplicity of non-statistical approaches makes them practical for smaller engagements or situations where statistical precision is unnecessary.

Key considerations when choosing between methods:

Population size and complexity

Audit risk tolerance levels

Available resources and timeline

Regulatory requirements and client expectations

Auditor expertise in statistical techniques

Pro Tip: Use statistical and non-statistical sampling when you need to control sampling risk below 5% for high-stakes audits of public companies or regulated entities.

Standards Governing Audit Sampling

Professional standards establish requirements that ensure audit sampling procedures produce reliable evidence. PCAOB AS 2315 and IAASB ISA 530 set professional requirements for audit sampling design, execution, and evaluation. Understanding these frameworks is mandatory for auditors working in 2026.

PCAOB AS 2315 applies to audits of U.S. public companies registered with the SEC. This standard requires auditors to plan sampling procedures, select appropriate sample sizes, perform testing, and evaluate results in ways that provide sufficient appropriate evidence. The PCAOB emphasizes documentation of the sampling methodology, rationale for sample size, and evaluation of findings.

IAASB ISA 530 provides international guidance applicable in jurisdictions following International Standards on Auditing. While similar to PCAOB standards, ISA 530 applies more broadly to private and public entity audits worldwide. Both frameworks require auditors to consider sampling risk, design representative samples, and project sample results to populations.

The AICPA also issues guidance influencing audits of non-public U.S. entities. These guidelines align with international standards while addressing practical considerations for smaller firms and private company audits.

Key compliance requirements include:

Adequate planning before sample selection begins

Scientifically sound selection methods

Sufficient sample sizes based on risk assessment

Proper evaluation and extrapolation of results

Comprehensive documentation of all sampling decisions

Complying with these standards ensures audit conclusions meet reliability and materiality thresholds expected by regulators, clients, and financial statement users. Regulatory reviewers routinely examine sampling documentation during quality inspections, making proper adherence to audit sampling regulatory standards essential for avoiding deficiencies.

Determining Sample Size in Audits

Calculating appropriate sample sizes requires balancing audit risk with resource constraints. Sample size depends on factors like tolerable error, expected error, population size, and risk of incorrect acceptance. Systematic approaches help auditors make defensible decisions.

Follow these steps for audit sample size determination:

Define the audit objective and identify the population clearly

Assess inherent risk, control risk, and acceptable detection risk

Establish tolerable error and expected error rates

Select confidence level based on audit risk assessment

Apply statistical formulas or reference standardized tables

Adjust sample size for special considerations or constraints

Audit risk components directly influence sample size requirements. Higher inherent or control risk requires lower detection risk, which necessitates larger samples. Conversely, strong controls and low inherent risk allow smaller samples while maintaining adequate assurance.

Tolerable error represents the maximum error auditors can accept without adjusting their opinion. Smaller tolerable error thresholds require larger samples to detect deviations. Expected error reflects the auditor’s best estimate of errors in the population based on prior audits or preliminary testing.

Population Size | Low Risk | Medium Risk | High Risk |

Under 1,000 | 25-40 | 40-60 | 60-100 |

1,000-10,000 | 30-50 | 50-80 | 80-150 |

Over 10,000 | 40-60 | 60-100 | 100-200+ |

Sample sizes that are too small increase sampling risk and the chance of incorrect conclusions. Excessively large samples waste resources without proportional increases in audit quality. Finding the optimal balance requires judgment informed by professional standards and statistical principles.

Pro Tip: Regularly revisit sample size assumptions as you gather preliminary evidence and adjust your sampling plan if initial findings reveal higher-than-expected error rates or control weaknesses.

Understanding Sampling Risk and Its Relationship to Audit Risk

Sampling risk represents the possibility that sample results differ materially from the actual population characteristics. Sampling risk is the risk that sample results differ from the whole population, affecting audit conclusions. This risk cannot be eliminated but must be managed to acceptable levels.

Sampling risk comprises two types. The risk of incorrect acceptance occurs when auditors conclude controls are effective or balances are fairly stated when they are not. The risk of incorrect rejection leads auditors to conclude controls are ineffective or balances are misstated when they actually are acceptable. Both create problems, though incorrect acceptance poses greater audit risk.

This risk component fits within the broader audit risk model alongside inherent risk and control risk. Total audit risk equals the product of these three factors. Auditors manipulate sampling risk through sample size and selection methods to keep overall audit risk at acceptably low levels.

Strategies for managing sampling risk include:

Increasing sample sizes to reduce variability

Using random or systematic selection to ensure representativeness

Employing statistical methods to quantify and control risk

Stratifying populations to focus on high-risk items

Performing additional procedures when results are inconclusive

Sampling risk is manageable and should be controlled through proper planning and execution, not eliminated entirely, which would require testing 100% of the population.

Understanding this relationship helps you balance efficiency with assurance. While larger samples reduce sampling risk, they increase audit costs and timeline. The goal is achieving sufficient assurance at reasonable cost, not perfection. Professional judgment guided by standards determines the appropriate risk level for each engagement.

Common Misconceptions About Audit Sampling

Several widespread myths about audit sampling can mislead auditors and compromise audit quality. Increasing sample size beyond optimal points yields diminishing returns for audit quality. Recognizing these misconceptions helps auditors make better decisions.

Myth: Larger samples always improve audit conclusions. Reality: After reaching an optimal size based on statistical calculations, additional items provide minimal incremental assurance. The relationship between sample size and confidence is not linear. Doubling your sample size does not double your confidence level.

Myth: Audit sampling must be statistical to be valid. Reality: Non-statistical sampling based on sound professional judgment can provide sufficient appropriate evidence. Many successful audits use judgment-based selection, particularly for smaller populations or lower-risk areas. The key is proper documentation and logical rationale.

Myth: Ignoring population extrapolation is acceptable if sample errors are small. Reality: Failing to project sample findings to the entire population violates professional standards and can lead to material misstatements going undetected. Even small sample error rates may indicate material population errors.

Misinterpreting sampling results creates significant audit risk. Auditors sometimes treat sample results as definitive rather than estimates subject to sampling risk. Others fail to consider qualitative aspects of errors, focusing solely on quantitative projections. Both approaches can lead to flawed conclusions.

Additional misconceptions:

Believing random selection is the only acceptable method

Assuming sampling works equally well for all audit objectives

Thinking smaller populations always require testing a higher percentage

Overlooking the need to test all high-value or unusual items separately

Pro Tip: Always consider cost-benefit tradeoffs when designing sampling plans and rely on professional standards over intuition when making sample size and selection decisions.

Evaluating and Extrapolating Audit Sample Results

Proper evaluation of sample findings determines whether audit objectives are met. Extrapolating errors found in samples to the total population is essential to determine material misstatements. This process transforms sample data into population-level conclusions.

After completing sample testing, auditors must systematically analyze results:

Record all identified deviations or monetary errors

Classify errors by type, cause, and significance

Calculate sample error rates or amounts

Project sample findings to the entire population

Compare projected errors to materiality thresholds

Form conclusions about population characteristics

Document the evaluation process and rationale

Projecting sample errors requires different approaches depending on sampling method. For statistical samples, auditors use formulas that incorporate sampling risk to calculate upper and lower error bounds. For non-statistical samples, auditors apply professional judgment to estimate likely population errors, often using simple ratio extrapolation.

Key considerations during evaluation:

Whether errors are isolated incidents or systematic problems

The nature and cause of identified deviations

Whether errors are factual, judgmental, or projected

How close projected errors come to materiality limits

Whether additional testing is needed for inconclusive results

Materiality thresholds determine whether identified errors require audit opinion modifications or client adjustments. If projected population error exceeds tolerable error, auditors must either request client corrections or modify their audit opinion. When projected error approaches but does not exceed tolerable error, auditors consider performing additional procedures to reduce uncertainty.

Ignoring proper extrapolation risks underestimating audit risk and issuing inappropriate opinions. Even small sample errors can indicate material population problems. Thorough evaluation ensures audit conclusions rest on solid evidence and comply with professional requirements.

Practical Application and Industry-Specific Considerations

Applying sampling techniques effectively requires adapting general principles to specific audit contexts. Tailoring audit sampling methodology to specific audit objectives and industry regulations improves compliance and efficiency. Real-world implementation involves balancing theory with practical constraints.

In large financial institution audits, statistical sampling helps manage vast transaction volumes while controlling sampling risk precisely. Banks processing millions of transactions monthly cannot test everything, so stratified random sampling focuses effort on high-value items while maintaining statistical validity across the population.

Smaller organizations with limited transaction volumes often benefit from non-statistical approaches. A regional manufacturer with 5,000 annual purchase orders might use judgment-based selection, focusing on unusual items, large amounts, and random selections across the year. This practical method provides adequate evidence without statistical complexity.

Industry-specific factors influence sampling decisions:

Healthcare audits must address regulatory compliance sampling for billing and patient records

Government audits often follow specific sampling requirements in federal audit guides

Banking audits incorporate risk-based sampling aligned with regulatory capital requirements

Insurance audits stratify by policy type, premium size, and claim complexity

Integrating master risk assessment for auditors with sampling plans improves effectiveness. Higher-risk areas identified during planning receive larger samples or more rigorous testing. Lower-risk areas allow smaller samples, optimizing audit resources.

Practical tips for implementation:

Start sample design during audit planning, not during fieldwork

Document sampling rationale contemporaneously with decisions

Consider automation tools for large population sampling

Maintain flexibility to adjust plans based on preliminary findings

Consult with experienced auditors or specialists for complex scenarios

Successful audits balance theoretical rigor with practical realities. Resource constraints, client cooperation, and timeline pressures all affect sampling decisions. The goal is achieving sufficient appropriate evidence within real-world limitations, not perfect statistical purity.

Advance Your Audit Sampling Expertise with Professional CPE Training in 2026

Mastering audit sampling requires ongoing education as standards evolve and techniques advance. Our 2026 CPE Event Calendar offers comprehensive training designed specifically for auditors seeking practical skills and certification credits. Learn directly from industry experts with Big 4 backgrounds who translate complex sampling concepts into actionable strategies.

Stay current with PCAOB AS 2315, IAASB ISA 530, and emerging best practices through our specialized courses. Our internal auditor CPE webinars provide flexible learning options, while our audit sampling techniques in-person training delivers hands-on experience with real-world applications. Whether you are preparing for CIA, CPA, or CISA certifications, our NASBA-approved programs help you build confidence and competence in audit sampling methodology.

Frequently Asked Questions About Audit Sampling

How does audit sampling differ from testing 100% of the population?

Audit sampling examines only a subset of items, using statistical or judgment-based methods to draw conclusions about the entire population. Testing 100% provides complete certainty but is rarely cost effective or necessary. Sampling balances reasonable assurance with practical resource constraints, allowing auditors to form reliable conclusions while managing time and budget limitations.

Can sampling risk be completely eliminated in an audit?

No, sampling risk exists whenever auditors test less than 100% of a population. However, auditors control sampling risk to acceptably low levels through proper sample size calculations, random selection methods, and statistical techniques. Professional standards require managing, not eliminating, sampling risk as part of the overall audit risk model.

How do auditors choose between statistical and non-statistical sampling in practice?

The choice depends on audit risk, population characteristics, regulatory requirements, and available resources. Statistical methods suit large populations, high-risk areas, or situations requiring precise risk quantification. Non-statistical approaches work well for smaller audits, lower-risk areas, or when statistical expertise is limited. Both methods can provide sufficient appropriate evidence when properly designed and executed.

Do professional standards require documenting all sampling procedures?

Yes, PCAOB AS 2315, IAASB ISA 530, and AICPA guidance require comprehensive documentation of sampling methodology, including rationale for sample size, selection method, items tested, errors found, and conclusions reached. Proper documentation allows supervisors and regulators to understand and evaluate the auditor’s judgment and ensures sampling procedures can withstand scrutiny during quality reviews.

Can audit sampling be used for both control testing and substantive procedures?

Absolutely. Auditors apply sampling to test internal controls’ operating effectiveness and to perform substantive tests of account balances and transactions. The principles remain consistent, though specific considerations differ. Control testing typically uses attribute sampling to estimate deviation rates, while substantive testing often employs variables sampling to estimate monetary amounts. Both applications follow the same fundamental standards for design, selection, and evaluation.

Recommended