Understand the audit risk model: Enhance controls and risk

- John C. Blackshire, Jr.

- Apr 27

- 10 min read

TL;DR:

Audit failures often result from weak or misunderstood risk models, not random errors.

The traditional audit risk model is being enhanced by data analytics and machine learning.

Effective risk assessment now requires combining professional judgment with continuous, data-driven tools.

Most audit failures are not random accidents. They are predictable outcomes tied directly to weak, incomplete, or misunderstood audit risk models. If your team has ever issued an opinion and later discovered a material misstatement slipped through, the root cause likely traces back to how risk was assessed, weighted, and managed from the start. The audit risk model (ARM) is one of the most foundational frameworks in auditing, yet it is frequently reduced to a formula on a planning worksheet rather than treated as a living guide for professional judgment. This article clarifies what the ARM actually does, how each component works in practice, where the model falls short, and how technology is reshaping what effective risk assessment looks like in 2026.

Table of Contents

Key Takeaways

Point | Details |

Audit risk model basics | The model helps auditors systematically assess the risk of undetected errors in financial reporting. |

Model limitations | Traditional models can miss complex or dynamic risks, so professionals should combine classic and modern tools. |

Tech-powered audits | Machine learning and analytics measurably improve audit risk prediction accuracy. |

Continuous learning | Ongoing education in risk modeling methods is critical for top-performing audit teams. |

What is the audit risk model?

The audit risk model gives auditors a structured way to think about the likelihood that an audit opinion will be wrong. In simple terms, it answers the question: what is the probability we miss something material? That probability is never zero, but the ARM helps you quantify and manage it.

The formula is straightforward:

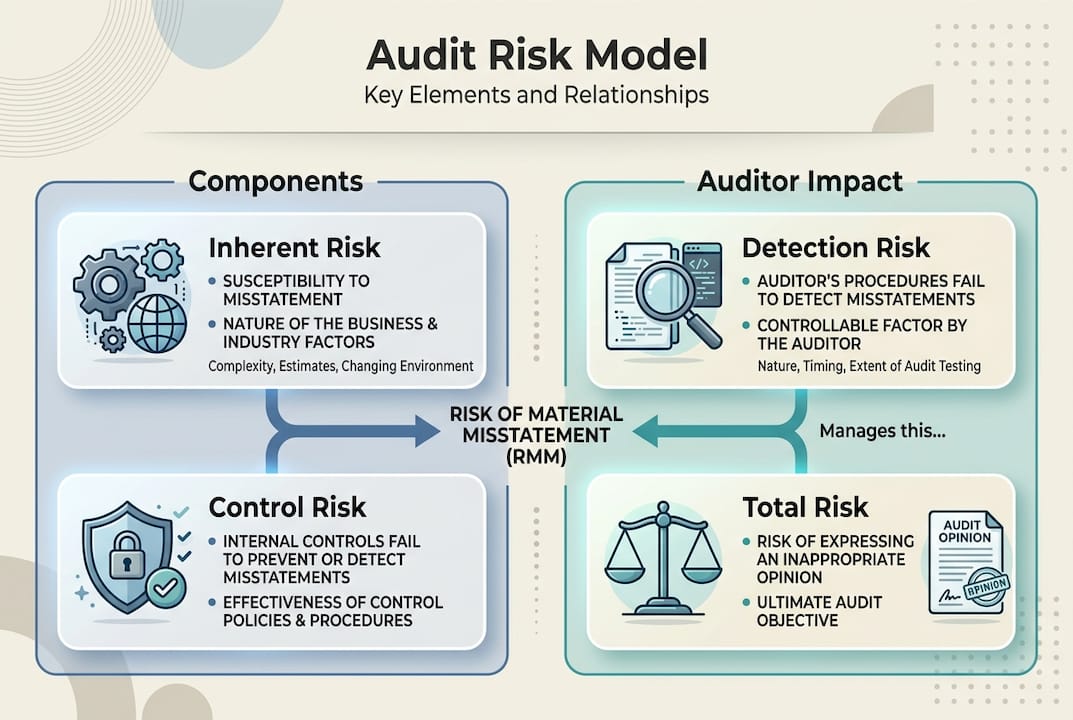

Audit Risk (AR) = Inherent Risk (IR) × Control Risk (CR) × Detection Risk (DR)

Each variable represents a different source of risk in the audit process. Understanding how they interact is essential for audit planning best practices that produce reliable results.

Here is a quick breakdown of the three core components:

Inherent Risk (IR): The susceptibility of an account or assertion to material misstatement before considering internal controls.

Control Risk (CR): As noted in audit standards, Control Risk is the risk that internal controls fail to prevent or detect material misstatements.

Detection Risk (DR): The risk that the auditor’s own procedures will not catch a material misstatement that exists.

Component | Controlled by | Key question |

Inherent Risk | Client environment | How prone is this area to error by nature? |

Control Risk | Client’s internal controls | How strong are the controls protecting this area? |

Detection Risk | Auditor’s procedures | How thorough are our audit tests? |

“The audit risk model provides a conceptual framework for determining the nature, timing, and extent of audit procedures. It is not a mechanical calculation but a tool for structured professional judgment.”

The ARM is most powerful when used as a decision-making guide rather than a compliance checkbox. When auditors treat it that way, it shapes how much evidence they gather, which accounts they prioritize, and how they respond to red flags as the engagement progresses.

Components of the audit risk model explained

Knowing the model’s formula, let’s break down each component and see how they work together in practice.

Inherent Risk reflects the natural complexity and risk embedded in a financial area before any controls are applied. High inherent risk typically appears in areas involving significant estimates, complex transactions, or unusual activity. Think of a manufacturing company’s inventory valuation: there are physical counts, cost allocations, and obsolescence judgments all happening simultaneously. That complexity creates natural exposure to error.

Control Risk is arguably the most consequential component because it reflects the strength of the client’s own defenses. Control Risk (CR) is the risk that internal controls fail to prevent or detect material misstatements. If those controls are strong and well-tested, auditors can reduce the level of substantive testing. If controls are weak or untested, detection risk must be lowered to compensate, meaning more audit work is required.

Detection Risk is the one variable the auditor can directly influence. If inherent and control risks are both high, you respond by designing more rigorous, targeted procedures and expanding sample sizes to bring detection risk down to an acceptable level.

Risk component | Definition | Practical example | How auditor manages it |

Inherent Risk | Natural risk before controls | Revenue recognition for long-term contracts | Allocate more senior resources |

Control Risk | Risk controls won’t catch errors | Segregation of duties gaps in a small entity | Increase substantive testing |

Detection Risk | Risk auditor procedures miss errors | Sampling that excludes key transactions | Expand procedures and sample sizes |

Here is a step-by-step framework for evaluating each risk in a real engagement:

Assess the client’s industry, complexity, and history of misstatements to set Inherent Risk.

Walk through the client’s control environment to evaluate the design effectiveness of key controls.

Test controls for operating effectiveness where you plan to rely on them.

Set Detection Risk based on what Inherent Risk and Control Risk require.

Design substantive procedures accordingly, more when Detection Risk must be low.

Pro Tip: A common mistake is treating Control Risk as automatically low just because management asserts their controls are strong. Always test operating effectiveness before relying on any control. Documentation alone is not evidence of a functioning control. This is especially relevant when reviewing compliance audit best practices for high-risk engagements.

Limitations of the traditional audit risk model

While this model is foundational, professionals must recognize its constraints. Let’s examine where ARM may fall short.

The traditional ARM was designed in an era when audit evidence came from paper records and controlled environments. Today’s audit landscape looks very different. Organizations operate across geographies, systems, and business models that introduce risks the original formula was never built to handle.

The most commonly cited limitations include:

Oversimplification: The ARM treats risk as three discrete variables, but in reality, risks are interconnected. A control failure in one area can amplify inherent risk in another area in ways the formula does not capture.

Static nature: Traditional ARM is applied at a point in time, usually during planning. But risk evolves throughout an engagement. An economic shock, a leadership change, or a cybersecurity incident midway through an audit can shift the risk profile entirely.

Subjectivity bias: Each of the three components is ultimately based on the auditor’s judgment. Two equally qualified auditors can assess the same control environment and arrive at different Control Risk assessments, which creates inconsistency.

Qualitative risk gaps: The ARM focuses primarily on quantitative financial statement risk. It is less equipped to capture reputational risks, behavioral risks, or systemic risks tied to culture or leadership tone.

Traditional ARM is criticized as oversimplifying qualitative risks and being static and judgment-biased. Researchers point to predictive analytics and machine learning as paths toward a more dynamic and data-driven assessment approach.

Complex industries illustrate these gaps vividly. In financial services, for example, the speed of transactions and the volume of automated processes can make manual control testing feel like reviewing last month’s weather forecast. In rapidly scaling technology companies, control environments built for a 50-person startup often cannot keep pace with a 500-person organization. The ARM, applied traditionally, may not surface those growing pains until it is too late.

Pro Tip: Do not rely entirely on your own professional judgment when assessing risk in unfamiliar industries. Build a structured checklist anchored to documented industry risks and complement it with data analytics before finalizing your risk assessments. Reviewing audit management strategies can help you identify systematic approaches to risk documentation.

Advances in audit risk modeling: Data and technology

Recognizing these limitations has pushed many audit teams to adopt technology-driven improvements. Here is how data and innovation are reshaping audit risk.

Machine learning models are not replacing the audit risk model. They are making it more accurate and more responsive to real-world conditions. The most significant development is the shift from static judgment to dynamic, evidence-driven risk scoring.

Random Forest machine learning models have demonstrated F1 scores of 0.90 and AUC of 0.91 when predicting high audit risk, significantly outperforming traditional methods that rely on heuristics and manual assessment. That means these models correctly identify high-risk areas with far greater precision and far fewer false negatives.

Approach | Risk accuracy | Adaptability | Subjectivity |

Traditional ARM | Moderate | Low (static) | High |

Predictive analytics | High | Medium | Medium |

Machine learning (Random Forest) | Very High (AUC 0.91) | High (dynamic) | Low |

Here is what predictive analytics and machine learning bring to the audit risk assessment process:

Continuous monitoring: Rather than assessing risk at a single point in time, data-driven models can flag anomalies in real time as transactions occur.

Pattern recognition: ML models identify subtle relationships between financial variables that human reviewers might miss, especially in large data sets.

Objectivity: Algorithms do not have the same judgment biases that individual auditors carry. While they require careful design and validation, they introduce a form of consistency that professional judgment alone cannot guarantee.

Scalability: Analytics can cover 100% of a population rather than a sample, which directly reduces Detection Risk in a way traditional testing cannot match.

Organizations implementing risk assessment for auditors frameworks are increasingly incorporating analytics tools to replace or supplement judgment-based risk scoring. The role of risk assessment in audit quality is expanding, not shrinking, as these tools become more accessible. For additional context on how broader risk mitigation strategies are evolving, operational risk reduction strategies offer a useful external perspective.

Best practices for applying the audit risk model

With new technologies and critiques in mind, here is how to put theory into action for stronger audits.

Applying the ARM well requires more than knowing the formula. It requires a systematic approach that integrates professional judgment, documented evidence, and, increasingly, analytical tools. Here are the core steps for a successful ARM implementation in any engagement:

Start with entity-level risk. Before assessing individual accounts, understand the overall risk environment. Management’s philosophy, governance structure, and industry dynamics all set the baseline for Inherent Risk.

Document your control environment assessment rigorously. Every conclusion about Control Risk should be supported by evidence, walkthroughs, prior audit results, or analytical indicators, not assumptions.

Set an explicit Detection Risk target. Rather than defaulting to “moderate,” calculate what Detection Risk must be given your Inherent and Control Risk assessments, then design procedures that actually meet that threshold.

Use analytics to pressure-test your judgments. Run data analytics early in the planning phase to identify anomalies or outliers that could signal elevated risk areas your traditional assessment might have underweighted.

Revisit risk assessments throughout the engagement. Risk is not frozen after the planning memo is signed. Build in a formal midpoint reassessment, especially for long or complex engagements.

Link procedures directly to specific risk conclusions. Every audit procedure should trace back to a specific risk. If you cannot articulate why a procedure addresses a specific risk, reconsider its value.

Common pitfalls to avoid:

Treating Control Risk as low without performing any tests of controls

Failing to update risk assessments when new information emerges during fieldwork

Over-relying on prior year conclusions without evaluating whether conditions have changed

Designing detection procedures based on habit rather than current risk conclusions

Ignoring qualitative risk signals like management override, high turnover, or cultural pressure

As highlighted in guidance on Control Risk, controls that are not properly tested cannot reduce the auditor’s assessment of risk, regardless of how well-documented they appear in policy manuals.

Pro Tip: Build a risk matrix that maps each ARM component to specific financial statement areas, then use that matrix to drive resource allocation. Higher-risk areas get more senior staff, larger samples, and more directional testing. This single discipline can significantly lift audit quality across an engagement. Referencing current risk management strategies can give you a broader framework for integrating ARM into your organization’s overall risk governance.

Our take: The evolving future of the audit risk model

We want to be direct about something: the audit risk model is not going away. It is too useful as a conceptual scaffold for how auditors think about uncertainty and evidence. But the version of ARM that lives solely in a planner’s judgment, applied once at the start of an engagement, is no longer sufficient on its own.

The profession is moving toward a model where the ARM formula serves as the strategic framework and data-driven tools fill in the accuracy gaps. Machine learning does not replace the auditor’s understanding of the business, but it does make that understanding sharper and more defensible. Auditors who learn to work with analytics tools, not just alongside them, will produce better risk assessments and more credible opinions.

Our honest prediction is that within the next few years, continuous auditing and predictive risk scoring will become the baseline expectation for high-quality engagements, not an advanced differentiator. That means now is the time to build those skills. Staying informed on 2026 compliance risk practices is a practical starting point for understanding where the profession is headed and what your team needs to prepare.

The professionals who will lead in this environment are those who understand both the classic principles and the modern tools well enough to know when each applies.

Advance your audit skillset with specialized training

Mastering the audit risk model is not a one-time exercise. Risk environments evolve, standards update, and new tools emerge constantly. Staying current requires deliberate, ongoing investment in your professional knowledge.

At compliance-seminars.com, we offer targeted CPE training designed specifically for audit and compliance professionals who need practical, standards-based instruction they can apply immediately. Whether you prefer live instruction or on-demand formats, our 2026 CPE event calendar features sessions across multiple U.S. cities covering audit risk, internal controls, and emerging compliance topics. For a focused deep dive into control frameworks and risk assessment methodologies, explore our internal control CPE training offerings built around COSO, SOX, and modern auditing standards.

Frequently asked questions

What is control risk in the audit risk model?

Control risk is the chance that a company’s internal controls won’t prevent or detect errors or fraud during an audit, meaning material misstatements could exist without the client’s systems catching them.

How is the audit risk model formula calculated?

The audit risk model is calculated as Audit Risk = Inherent Risk × Control Risk × Detection Risk, where each component reflects a different source of uncertainty in the audit process.

Why is the traditional audit risk model criticized?

Critics say it overlooks qualitative risks and relies too heavily on static or subjective judgment, making it less effective in complex, fast-moving business environments.

How is technology making audit risk assessment better?

Machine learning models such as Random Forest are helping auditors predict high-risk areas with substantially greater precision, achieving AUC scores of 0.91 compared to the more variable results of traditional manual assessment methods.

Recommended

Comments