SOX Compliance Explained: Impact on Auditing Roles

- Леонид Ложкарев

- Jan 28

- 8 min read

Updated: Jan 31

Public trust in financial reporting can shift overnight when compliance gaps emerge. For internal auditors and compliance officers across the United States and Canada, the impact of the Sarbanes-Oxley Act goes far beyond routine box-checking.

Mastering internal control frameworks and understanding SOX’s evolving requirements not only protects organizations from risk but also directly supports executive accountability and investor confidence. This resource gives you a focused look at what matters most for effective SOX compliance in today’s regulatory climate.

Table of Contents

Key Takeaways

Point | Details |

SOX Objectives | The Sarbanes-Oxley Act enhances corporate accountability and financial transparency by implementing strict controls and penalties for financial misconduct. |

Executive Accountability | CEOs and CFOs are personally responsible for the accuracy of financial statements, facing severe penalties for misrepresentation. |

Role of PCAOB | The Public Company Accounting Oversight Board establishes rigorous audit standards, reinforcing the need for thorough and independent financial examinations. |

Effective Compliance Strategies | Organizations should adopt a risk-based approach to compliance, leveraging technology to automate controls and improve efficiency in documentation and monitoring. |

What Is SOX Compliance and Why It Matters

The Sarbanes-Oxley Act (SOX) represents a critical legislative framework designed to transform corporate accountability and financial transparency in the United States. Passed in 2002 as a direct response to massive accounting scandals involving Enron and WorldCom, this federal law fundamentally reshaped how publicly traded companies manage their financial reporting and internal controls.

At its core, SOX mandates stringent standards for financial record keeping and establishes severe penalties for corporate and accounting fraud. Public companies must now implement comprehensive internal control systems that ensure accurate financial reporting and prevent potential manipulation. The law specifically targets corporate leadership, requiring CEOs and CFOs to personally certify the accuracy of financial statements and holding them legally responsible for any misrepresentations.

The legislation created the Public Company Accounting Oversight Board (PCAOB), an independent regulatory body charged with overseeing audit procedures and ensuring independent, rigorous financial examinations. This development was revolutionary, as it introduced unprecedented levels of external scrutiny into corporate financial practices. By establishing clear accountability mechanisms, SOX aims to restore investor confidence and create a more transparent corporate environment where financial integrity is paramount.

Pro tip: Develop a robust compliance documentation system that tracks all internal control processes and maintains clear audit trails to simplify SOX reporting and reduce potential regulatory risks.

Essential SOX Act Provisions for Auditors

The Sarbanes-Oxley Act imposes critical requirements on auditors that fundamentally transform their professional responsibilities and accountability. Public Company Accounting Oversight Board (PCAOB) standards now mandate rigorous protocols for financial reporting and independent audit procedures, creating a more transparent and trustworthy corporate financial environment.

Under SOX, auditors must adhere to several key provisions that directly impact their professional practice. Section 302 requires auditors to verify that financial reports are free from material misstatements and fairly represent the company’s financial condition. Section 404 specifically mandates comprehensive internal control assessments, compelling auditors to thoroughly evaluate and document a company’s financial reporting mechanisms. This means conducting detailed risk assessments, identifying potential control weaknesses, and providing substantive recommendations for improving financial governance.

The legislation also introduces significant personal and professional consequences for non-compliance. Auditors who fail to meet SOX requirements can face severe penalties, including potential criminal charges, professional decertification, and substantial financial penalties. These stringent requirements ensure that auditors maintain the highest standards of professional integrity, independence, and thoroughness in their financial reporting and audit procedures.

Pro tip: Maintain meticulous documentation of all audit procedures and internal control assessments to demonstrate compliance and protect your professional reputation.

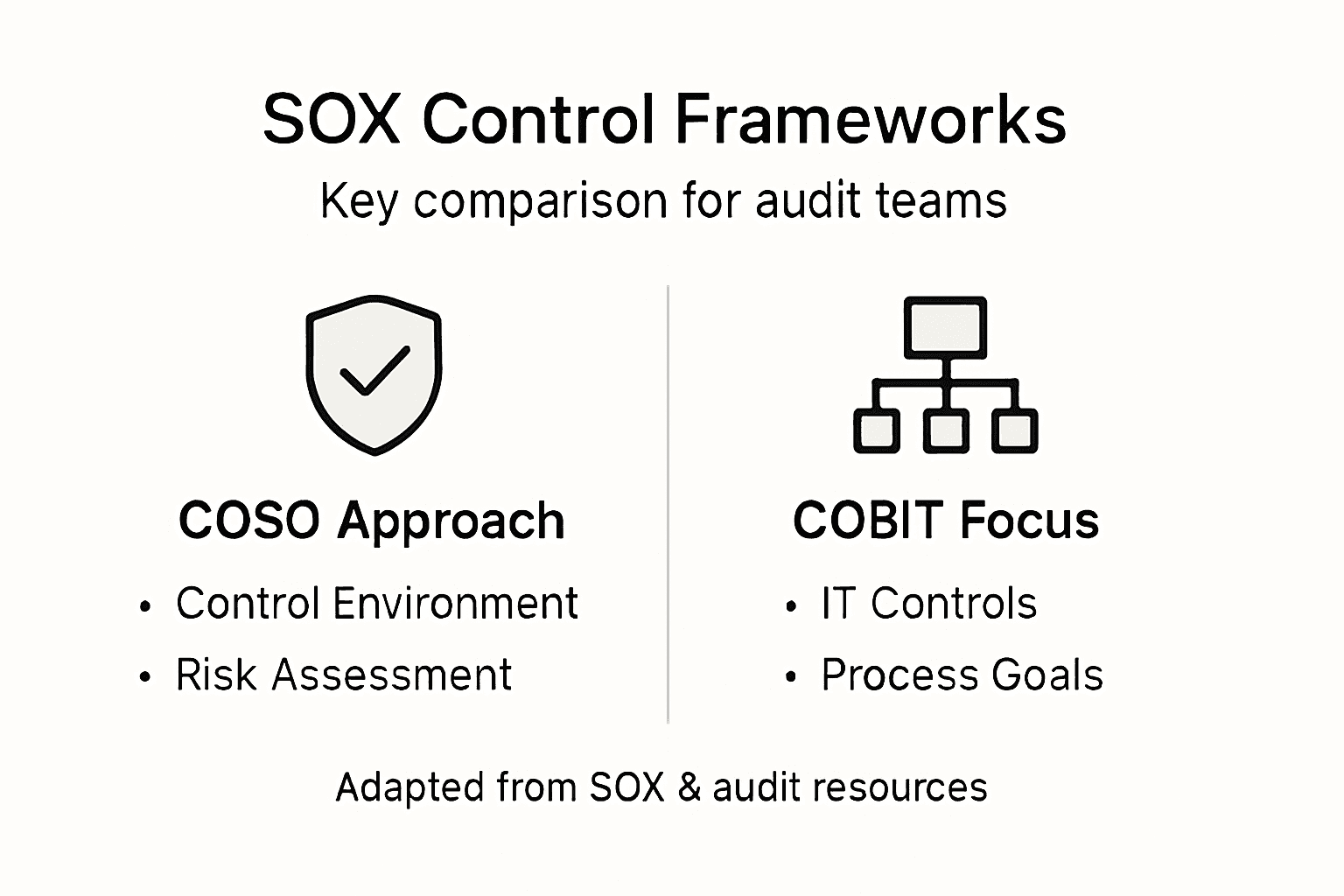

Internal Control Frameworks Used in SOX

Sarbanes-Oxley compliance relies critically on robust internal control frameworks that provide structured approaches to assessing and managing financial reporting risks. COSO and COBIT frameworks have emerged as the most widely adopted methodologies for organizations seeking to establish comprehensive internal control mechanisms.

The Committee of Sponsoring Organizations (COSO) framework stands out as the primary model for internal control assessment under SOX. This framework provides a comprehensive approach that evaluates control effectiveness across five critical components: control environment, risk assessment, control activities, information and communication, and monitoring activities. Organizations use COSO to systematically identify potential financial reporting risks, design appropriate control mechanisms, and continuously evaluate the effectiveness of their internal control systems.

Another significant framework is COBIT (Control Objectives for Information and Related Technologies), which focuses specifically on information technology governance and control. Under SOX Section 404, COBIT helps organizations develop robust IT control strategies that ensure the reliability, accuracy, and integrity of financial reporting systems. This framework is particularly valuable for addressing the complex technological risks associated with modern financial reporting, providing detailed guidelines for managing IT-related control objectives and minimizing potential vulnerabilities.

Pro tip: Implement a comprehensive internal control framework that integrates both COSO and COBIT principles to create a more holistic approach to SOX compliance and risk management.

Here’s a comparison of two key internal control frameworks used for SOX compliance:

Framework | Main Focus | Strengths | Typical Use Cases |

COSO | Enterprise-wide controls | Broad risk assessment, internal environment | Financial reporting and corporate governance |

COBIT | IT governance and controls | Detailed IT process guidance, tech risk focus | Managing IT-related financial risks |

Core SOX Compliance Requirements and Processes

The Sarbanes-Oxley Act establishes comprehensive compliance requirements that fundamentally reshape how public companies manage financial reporting and internal controls. SOX compliance involves complex assessment processes that demand rigorous documentation, testing, and ongoing evaluation of financial control mechanisms.

Section 302 of SOX introduces critical management certification requirements, compelling CEOs and CFOs to personally attest to the accuracy and completeness of financial statements. This provision mandates that senior executives take direct responsibility for the integrity of financial reporting, with potential criminal penalties for intentional misrepresentations. Additionally, Section 404 requires companies to produce an annual internal control report that comprehensively documents the effectiveness of financial reporting controls, including a detailed assessment of potential risks and the specific mechanisms designed to mitigate those risks.

The compliance process typically involves multiple interconnected steps, including risk identification, control design, documentation, testing, and continuous monitoring. Organizations must develop systematic approaches to evaluate their internal control environments, identifying potential vulnerabilities in financial reporting systems and implementing robust control activities. This requires a holistic approach that encompasses not just financial processes, but also technological systems, operational procedures, and organizational governance structures.

Pro tip: Develop a comprehensive compliance documentation system that tracks control assessments, maintains clear audit trails, and enables rapid response to potential reporting risks.

Key Roles, Responsibilities, and Liabilities

The Sarbanes-Oxley Act fundamentally transforms corporate governance by establishing clear and stringent roles and responsibilities for key organizational stakeholders. SOX imposes significant legal responsibilities on executives, creating a landscape of personal accountability that extends far beyond traditional corporate reporting practices.

Executive leadership, particularly CEOs and CFOs, bears the most substantial burden under SOX regulations. These top-tier executives are now personally responsible for certifying the accuracy and completeness of financial statements, with potential criminal penalties for intentional misrepresentations. This means that company leaders can face direct legal consequences, including substantial fines and potential imprisonment, for knowingly submitting false or misleading financial reports. The legislation effectively eliminates the traditional corporate shield, making individual executives directly answerable for their organization’s financial integrity.

Auditors and financial professionals also face heightened responsibilities under SOX. The Public Company Accounting Oversight Board (PCAOB) was established specifically to create rigorous standards for external auditors, ensuring their independence and professional conduct. Auditors must now maintain an unprecedented level of professional scrutiny, conducting comprehensive assessments of internal control mechanisms and providing unbiased evaluations of financial reporting processes. Their role has transformed from a primarily advisory function to a critical gatekeeping mechanism designed to protect investor interests and maintain market transparency.

Pro tip: Develop a comprehensive personal compliance documentation system that tracks your professional decisions, maintains clear evidence of due diligence, and protects you from potential legal vulnerabilities.

Common Mistakes and Risk Management Strategies

Organizations frequently encounter significant challenges when implementing Sarbanes-Oxley compliance programs, often resulting from misunderstandings about the scope and depth of required controls. SOX compliance strategies require targeted risk management that goes beyond traditional accounting practices.

One of the most prevalent mistakes is over-documentation and manual control implementation. Many organizations create unnecessarily complex compliance processes that consume substantial resources without providing meaningful risk mitigation. Companies often generate extensive documentation for controls that have minimal impact on financial reporting, leading to inefficient compliance efforts. The most effective approach involves adopting a risk-based methodology that prioritizes controls directly linked to significant financial statement risks, focusing on key accounts and critical control points that genuinely impact financial integrity.

Technology plays a crucial role in modern SOX compliance risk management. Automated control testing, continuous monitoring systems, and integrated risk assessment tools can dramatically reduce human error and provide more comprehensive oversight. Organizations should invest in technological solutions that enable real-time risk identification, streamline documentation processes, and create transparent audit trails. This approach not only enhances compliance effectiveness but also reduces the manual labor traditionally associated with SOX reporting requirements.

Below is a summary of common SOX compliance missteps and effective risk management strategies:

Common Mistake | Risk Created | Recommended Strategy |

Over-documentation | Wasted resources, inefficiency | Risk-based control prioritization |

Reliance on manual controls | Increased human error | Automate testing and monitoring |

Neglecting IT risks | Data breaches, inaccurate records | Integrate IT control frameworks |

Poor audit trail tracking | Regulatory exposure | Implement centralized documentation tools |

Pro tip: Implement a dynamic, technology-driven risk management approach that continuously assesses control effectiveness and adapts to emerging financial reporting challenges.

Master SOX Compliance and Elevate Your Auditing Expertise

Navigating the demanding landscape of SOX compliance requires a deep understanding of internal controls, audit responsibilities, and risk management strategies outlined in the Sarbanes-Oxley Act. This article highlights critical pain points such as rigorous documentation, personal accountability for executives and auditors, and the complexities of frameworks like COSO and COBIT. If you want to confidently meet these challenges and avoid common compliance pitfalls, specialized training is essential.

Boost your professional credentials with tailored CPE courses and webinars designed specifically for audit and compliance professionals. Whether you are a chief audit executive, internal auditor, or risk manager, Compliance Seminars offers expert-led instruction on SOX requirements and audit best practices. Explore practical strategies and step-by-step guidance to help you implement effective internal control frameworks and maintain a clear audit trail. Start advancing your skills today with live or online courses from industry experts with Big 4 experience at Compliance Seminars. Take action now so you can reduce your risks and confidently certify your company’s financial integrity.

Frequently Asked Questions

What is SOX compliance?

SOX compliance refers to adherence to the Sarbanes-Oxley Act, which mandates strict standards for financial record keeping and reporting processes for publicly traded companies. It aims to enhance corporate accountability and prevent financial fraud.

What are the key provisions of the Sarbanes-Oxley Act that affect auditors?

Key provisions include Section 302, which mandates the verification of financial reports for material misstatements, and Section 404, which requires comprehensive internal control assessments. These provisions emphasize the importance of independent audit procedures and accountability.

How has SOX impacted the role of auditors?

SOX has transformed auditors’ roles by imposing rigorous standards for financial reporting. Auditors must now conduct thorough assessments of internal controls and maintain a higher level of professional integrity, ensuring the accuracy of financial statements under strict compliance guidelines.

What internal control frameworks are commonly used for SOX compliance?

The COSO (Committee of Sponsoring Organizations) framework and COBIT (Control Objectives for Information and Related Technologies) are commonly used for establishing internal control systems. COSO focuses on enterprise-wide controls, while COBIT emphasizes IT governance and controls.

Recommended

Comments