How data analytics transforms auditing: guide for auditors

- John C. Blackshire, Jr.

- 2 hours ago

- 8 min read

Audit professionals have long relied on statistical sampling to draw conclusions about entire populations of transactions. That approach worked well enough when data volumes were manageable and fraud schemes were relatively straightforward. Today, the landscape looks very different. Machine learning models like Random Forest now achieve an F1 score of 0.90 in fraud detection tasks, a result that traditional sampling simply cannot match. This guide walks you through why analytics matters, how to apply it, where the risks hide, and what practical steps will help your team get real results.

Table of Contents

Key Takeaways

Point | Details |

Boosted fraud detection | Data analytics significantly increases the effectiveness and accuracy of identifying fraud in audits. |

Efficiency and coverage | Analytics enables auditors to analyze complete data sets quickly, improving both coverage and speed. |

Skill development needed | Auditors must enhance analytics and technical skills to maximize the benefits of new tools. |

Balance risk and judgment | Relying solely on analytics tools can be risky—professional judgment remains critical for reliable outcomes. |

Continuous improvement | Ongoing education and best practice implementation are key to leveraging analytics successfully in auditing. |

Why data analytics matters for today’s auditor

Traditional auditing selects a sample, tests it, and extrapolates findings to the broader population. That model carries inherent risk: the transactions you do not test are exactly where a sophisticated fraud scheme may live. Data analytics changes the equation by enabling auditors to examine every single transaction in a data set, not just a representative slice.

Big data tools and continuous monitoring platforms now make it possible to flag anomalies in real time rather than weeks after the fact. Think of it as moving from a periodic health checkup to a continuous vital-signs monitor. The difference in early detection is significant.

Machine learning, including Random Forest models, dramatically improves risk and fraud detection compared to traditional audit approaches. That is not a vendor claim; it is an empirical finding from peer-reviewed research.

“Analytics-driven auditing shifts the auditor’s role from reactive reviewer to proactive risk identifier, fundamentally changing what audit quality looks like.”

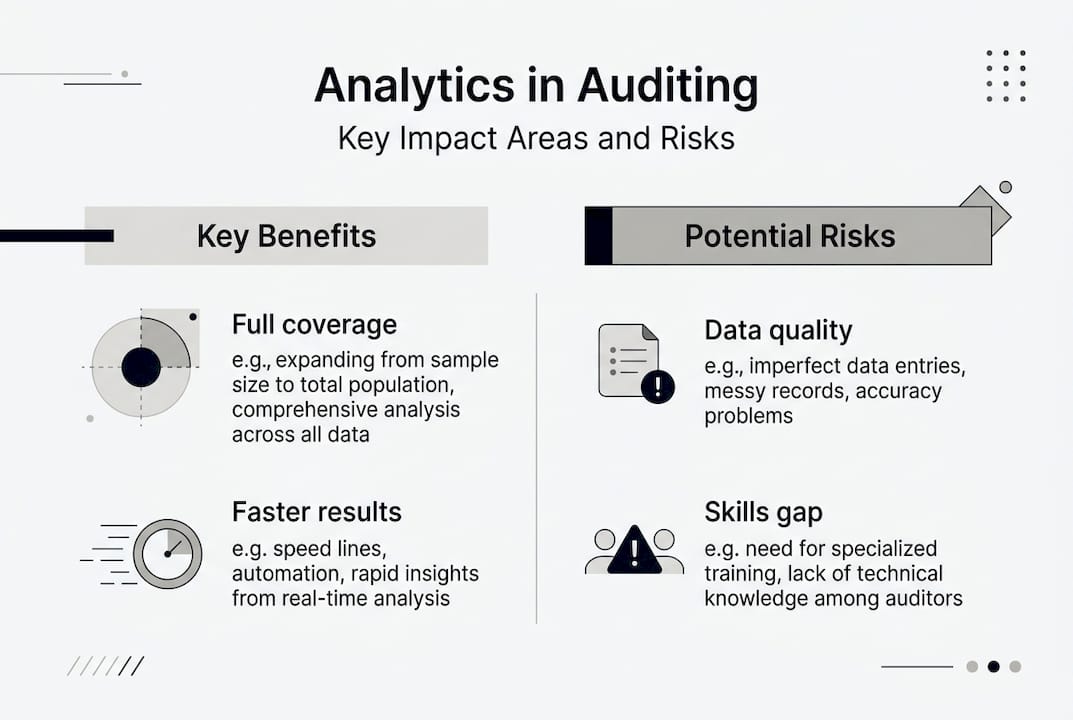

Key benefits you can expect when analytics is embedded in your audit process:

Full-population testing instead of sample-based inference

Real-time anomaly detection that surfaces issues before they escalate

Improved risk scoring that prioritizes high-risk areas for deeper review

Better audit coverage across complex, high-volume transaction environments

Stronger evidence to support auditor judgment and documentation

For a structured look at how this connects to your fraud detection process and your broader risk assessment for auditors, those resources offer practical frameworks you can apply immediately.

How data analytics enhances audit processes

Knowing that analytics adds value is one thing. Understanding exactly how it improves your day-to-day audit work is another. Data analytics allows deeper, broader evidence gathering that improves auditor judgment and efficiency across the entire engagement lifecycle.

Here is a direct comparison of where the two approaches diverge:

Dimension | Traditional sampling | Analytics-driven testing |

Population coverage | 5-15% of transactions | 100% of transactions |

Fraud detection timing | Post-period review | Near real-time flagging |

Anomaly identification | Manual pattern review | Automated model scoring |

Auditor time allocation | Data gathering heavy | Analysis and judgment heavy |

Evidence quality | Inferred from sample | Direct from full population |

A practical example: one internal audit team reviewing vendor payments manually sampled 200 invoices from a population of 40,000. They found nothing unusual. When they ran the same population through an analytics tool, the model flagged 47 duplicate payment patterns and three vendors with addresses matching employee records. The manual sample had missed all of it.

Pro Tip: Before deploying any analytics tool, map your data sources and confirm field definitions are consistent across systems. Inconsistent data structures are the single most common reason analytics projects stall before they produce findings.

Five steps for integrating analytics into your audit cycle:

Define the audit objective and identify which data sets are relevant

Assess data quality and resolve inconsistencies before analysis begins

Select and configure the appropriate analytic technique for the risk area

Review model outputs with professional judgment, not as final conclusions

Document the analytic methodology, parameters, and findings in your workpapers

For teams exploring advanced AI tools in auditing or evaluating AI implementation strategies, the sequencing of these steps matters as much as the tools themselves.

Challenges and risks: what auditors must manage

The advantages are real, but so are the pitfalls. Adopting analytics without a clear-eyed view of its limitations is how audit teams end up with false confidence in flawed findings.

Critiques of analytics adoption consistently point to three core concerns: data quality issues that undermine model outputs, skills shortages within audit teams, and the risk of over-reliance on analytic tools at the expense of professional judgment.

The skills gap is particularly acute. Many audit teams have strong technical auditors who lack data fluency, and strong data analysts who lack audit domain knowledge. Bridging that gap requires deliberate investment, not just access to software.

“A model is only as reliable as the data it processes and the judgment applied to its outputs. Neither element is optional.”

Common risks to monitor and manage:

Data integrity failures: source system errors that corrupt analytic results

Model bias: algorithms trained on historical data that reflect past blind spots

Scope creep: analytics expanding beyond the defined audit objective

Documentation gaps: insufficient workpaper support for analytic conclusions

Governance absence: no defined ownership for analytics tools and outputs

Pro Tip: Establish a peer review step specifically for analytic outputs. Have a second auditor independently assess whether the model flags align with the audit objective and whether the conclusions are supported by the underlying data.

Building a sound AI strategy for audit teams is foundational before deploying any tool at scale. Equally important is understanding compliance auditing risk in the context of analytics adoption, and maintaining the ethics in auditing that the profession demands.

Real-world applications: case studies and success stories

Empirical results from audit analytics deployments are increasingly well-documented. ML algorithms like Random Forest achieve an F1 score of 0.90 in fraud detection tasks, a benchmark that reflects both precision and recall in identifying fraudulent transactions.

Consider a financial services internal audit team that applied analytics to their accounts payable cycle. Manual review of a 10% sample had produced a clean opinion for three consecutive years. When analytics was applied to the full population, the team identified a pattern of split invoices designed to stay below approval thresholds. The scheme had been running for 22 months.

Key performance benchmarks from analytics-driven audit engagements:

Metric | Traditional approach | Analytics-driven approach |

Fraud detection rate | 60-70% | 85-92% |

Time to identify anomalies | 4-6 weeks | 24-72 hours |

Population coverage | 10-15% | 100% |

False positive rate | High (manual fatigue) | Reduced with model tuning |

Steps for replicating these results in your own engagements:

Identify a high-volume, high-risk transaction cycle as your pilot area

Extract and clean the full population data with IT support

Apply a supervised or unsupervised model appropriate to the risk hypothesis

Validate model outputs against known historical findings to calibrate accuracy

Present findings with full methodology documentation to audit leadership

For deeper context on applying these techniques, the fraud detection with ML resource and the risk assessment in practice guide both offer structured frameworks. The underlying ML in audit research provides the empirical foundation for these benchmarks.

Best practices for integrating data analytics into your audit workflow

Successful analytics integration is not about buying the most sophisticated tool. It is about building the right habits, governance structures, and skills within your team. Developing analytics skills and integrating expert judgment are critical for reaping the benefits of new tools.

Core best practices that consistently separate high-performing analytics programs from underperforming ones:

Pair every analytic output with a documented auditor interpretation

Establish data governance protocols before the first engagement goes live

Build analytics into the risk assessment phase, not just fieldwork

Rotate analytics responsibilities across team members to build broad capability

Review and update analytic models annually to reflect evolving risk patterns

For upskilling your team, a structured approach works better than ad hoc training. Here is a practical sequence:

Assess current team competencies in data analysis and audit-specific tools

Identify the gap between current skills and the analytics techniques your engagements require

Prioritize training in tools your organization already has access to before adding new platforms

Create internal knowledge-sharing sessions where team members present analytic findings and methods

Measure improvement through engagement-level metrics: detection rates, time savings, and documentation quality

When evaluating analytics solutions, look for tools that integrate with your existing audit management software, support your data formats, and produce outputs that are defensible in a regulatory review. The AI tool adoption for auditors resource covers selection criteria in detail, and avoiding analytics pitfalls addresses the sequencing mistakes that derail otherwise sound programs.

The goal is not to automate auditing. The goal is to give auditors better information so their judgment is applied where it matters most.

Advance your auditing skills with expert-led training

Data analytics is reshaping what auditors are expected to know and do. Staying current requires more than reading about it; it requires structured, practical training that connects technique to real audit scenarios.

At compliance-seminars.com, we offer CPE webinars for auditors that cover data analytics, AI tools, fraud detection, and risk assessment in formats designed for working professionals. Whether you prefer live instruction or self-paced learning, our audit CPE event calendar includes options across multiple U.S. cities and online. If you are building foundational skills, the auditing basics course provides a structured starting point recognized for CPE credit under NASBA standards. Your team’s analytics capability is a competitive and regulatory asset worth investing in.

Frequently asked questions

How does data analytics improve fraud detection in audits?

Data analytics enables auditors to test entire transaction populations rather than samples, surfacing anomalies and patterns that manual review misses. ML algorithms like Random Forest have achieved an F1 score of 0.90 in audit fraud detection tasks, reflecting strong precision and recall.

What are the biggest challenges in adopting data analytics for auditing?

The most significant barriers are skills shortages within audit teams, unreliable source data, and the risk of treating model outputs as conclusions rather than starting points. Skill gaps, data reliability, and model dependence are the most frequently cited concerns in audit analytics research.

Can data analytics fully replace auditor judgment?

No. Analytics augments professional judgment by providing better information, but the interpretation, documentation, and conclusions remain the auditor’s responsibility. Human oversight paired with analytic tools produces the most reliable audit outcomes.

Which audit areas benefit most from analytics?

Fraud detection, risk assessment, and anomaly identification in high-volume transaction cycles see the greatest measurable improvements. Analytics-driven auditing substantially improves detection rates and coverage in these focus areas.

What skills do auditors need to leverage analytics effectively?

Auditors need proficiency in data analysis techniques, familiarity with audit-specific analytic tools, and the critical thinking to distinguish a model flag from a confirmed finding. Skills development is essential for translating analytic outputs into defensible audit conclusions.

Recommended

Comments