Audit evidence explained: Strengthening assurance and compliance

- John C. Blackshire, Jr.

- Mar 27

- 9 min read

Updated: Mar 31

Many auditors assume that audit evidence is simply a stack of signed documents sitting in a workpaper file. That assumption is costly. Audit evidence is the foundation on which every audit opinion rests, and sufficient and appropriate evidence means the difference between a defensible conclusion and a professional liability. Whether you work in internal audit, external assurance, or compliance oversight, understanding how evidence is defined, gathered, and evaluated is not optional. This article walks through the standards, procedures, and practical judgment calls that shape evidence quality in every engagement.

Table of Contents

Key Takeaways

Point | Details |

Definition matters | Audit evidence is the information supporting audit conclusions, grounded in professional standards. |

Quality and quantity | Effective evidence evaluation relies on balancing sufficiency (quantity) and appropriateness (quality), guided by risk and materiality. |

Procedure variety | Auditors use seven distinct procedures to gather evidence, each with strengths and limitations. |

Judgment is critical | There are no universal benchmarks; evidence needs are determined by professional judgment and audit context. |

Training advances skills | Continuous training helps audit professionals navigate complex evidence evaluation and compliance challenges. |

What is audit evidence? Definition and principles

Audit evidence is the information auditors use to arrive at conclusions that support their opinion or findings. That definition sounds simple, but the implications run deep. Every test you perform, every document you review, and every interview you conduct produces evidence that either supports or challenges your working hypothesis.

Major standards bodies align closely on this concept. The PCAOB, IAASB, and IIA all treat evidence as the raw material of audit judgment. The audit importance for compliance function depends entirely on the quality of that raw material. Without reliable evidence, an audit opinion is just an opinion.

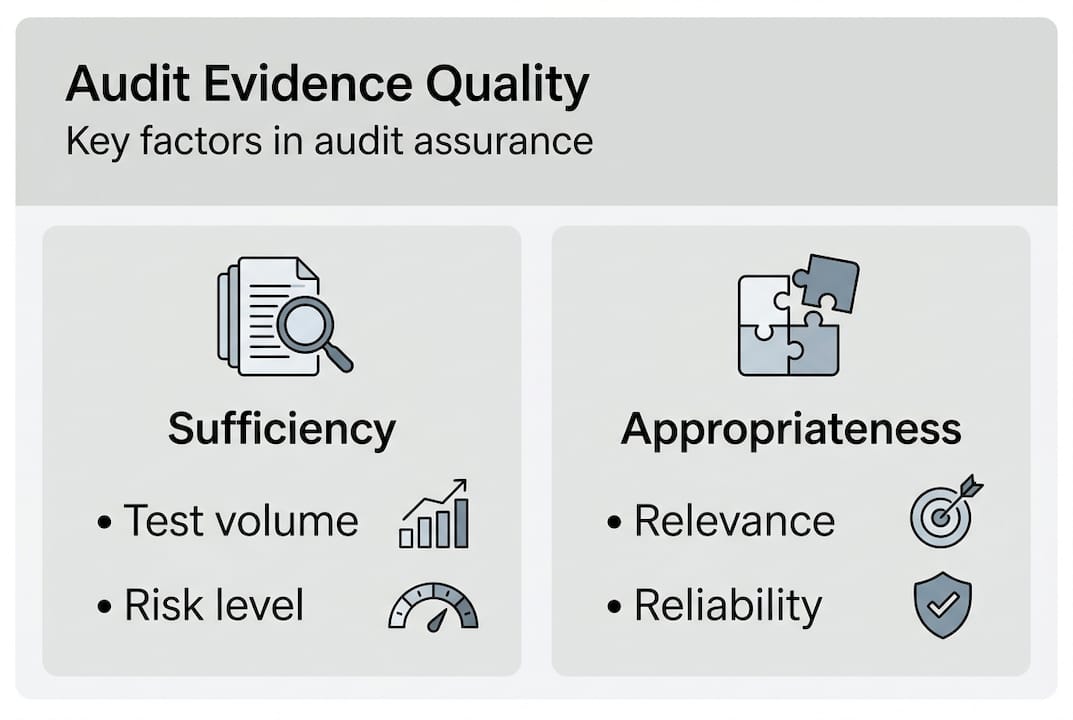

Two core principles govern all audit evidence:

Sufficiency refers to the quantity of evidence. More evidence is generally needed when the risk of material misstatement is higher.

Appropriateness refers to the quality of evidence, specifically whether it is relevant to the assertion being tested and reliable in its source.

Professional judgment determines how these two principles interact in any given engagement.

Documentation of evidence must support the conclusions reached, not just the procedures performed.

The PCAOB captures this balance precisely:

“Audit evidence must be sufficient (quantity affected by risk of material misstatement and quality) and appropriate (relevant and reliable).” — PCAOB AS1105

Understanding ethics in audit evidence is equally important here. Professional skepticism, which means questioning assumptions and corroborating claims, is not a personality trait. It is a standards-based requirement that shapes how you evaluate every piece of evidence you collect.

Types of audit evidence and typical sources

With the principles defined, the next step is understanding where audit evidence comes from and how it is collected. Evidence takes many forms, and not all forms carry equal weight.

The seven main audit procedures for gathering evidence are:

Inspection of records or physical assets

Observation of processes or controls in action

Inquiry through interviews with management or staff

Confirmation from independent third parties

Recalculation to verify mathematical accuracy

Reperformance of a control or process independently

Analytical procedures using comparisons and ratios

Each procedure produces a different type of evidence. Understanding types of audit evidence and their relative strengths helps you build a more defensible workpaper file. The internal audit evidence procedures you select should match the risk profile of the area under review.

Here is a quick comparison of common evidence sources and their reliability:

Evidence source | Type | Relative reliability |

Bank confirmation from third party | External | High |

Auditor-prepared recalculation | Internal | High |

Management-prepared schedules | Internal | Moderate |

Oral inquiry responses | Oral | Low to moderate |

Physical inspection of assets | Physical | High |

Electronic records with controls | Electronic | Moderate to high |

External evidence, such as a bank confirmation sent directly to the auditor, is generally more reliable than internal documents prepared by management. That does not mean internal evidence is useless. It means you need more of it, or you need to corroborate it with something stronger.

Audit procedures: How auditors collect evidence

Now that we know the evidence types, let us explore the specific procedures auditors use to gather them. Each procedure has a distinct purpose, and each has real limitations you need to account for.

The seven audit procedures work like tools in a toolkit. You would not use a hammer for every job, and you should not rely on inquiry alone for every audit area.

Inspection involves examining documents, contracts, or physical items. It is strong for existence and completeness assertions but tells you little about valuation.

Observation lets you watch a process happen in real time, like a physical inventory count. The limitation is that behavior may change when people know they are being watched.

Inquiry is fast and flexible but ranks lowest in reliability on its own. Always corroborate what management tells you.

Confirmation is one of the strongest procedures for cash and receivables. Direct responses from banks or customers carry significant weight.

Recalculation is straightforward: you recompute a figure to verify accuracy. It works well for depreciation schedules, interest calculations, and payroll.

Reperformance goes further by independently executing a control or process. If the client says a three-way match is performed on every invoice, you perform it yourself on a sample.

Analytical procedures use ratios, trends, and comparisons to identify unusual patterns. They are powerful for planning and final review stages.

Pro Tip: Never rely on a single procedure for a high-risk assertion. Layer two or three procedures to build a stronger, more defensible evidence base. Inquiry plus confirmation plus recalculation is far more persuasive than any one method alone.

The audit procedures for evidence you select directly affect whether your evidence meets the sufficiency and appropriateness bar. Choose procedures that match the assertion, the risk level, and the available sources.

Sufficiency and appropriateness: Determining quality and quantity

Having covered procedures, let us examine how auditors decide whether evidence is adequate. This is where professional judgment becomes the most critical skill in your toolkit.

Sufficiency has no fixed number. There is no rule that says “test 25 transactions and you are done.” The PCAOB AS1105 standard is clear that quantity is driven by risk of material misstatement and the quality of evidence already obtained. Higher risk means more evidence. Lower-quality evidence means more of it.

Research from the University of Arizona confirms that auditors use multiple bases for materiality and sufficiency judgments, going well beyond simple rules of thumb like the 5% of pre-tax income benchmark. Professional judgment is genuinely complex.

Here is how risk and materiality interact with evidence requirements:

Risk level | Materiality | Evidence quantity needed | Evidence quality required |

High | High | Large samples, multiple procedures | External or auditor-generated |

High | Low | Moderate samples | Corroborated internal sources |

Low | High | Targeted testing | Reliable internal or external |

Low | Low | Minimal testing | Internal with basic corroboration |

Appropriateness breaks into two parts. Relevance asks whether the evidence actually relates to the assertion you are testing. Reliability asks whether the source is trustworthy. A document created by management and never independently verified scores low on reliability, even if it is technically relevant.

Pro Tip: When you are unsure whether you have enough evidence, ask yourself this: “If a reviewer with no prior knowledge of this engagement read my workpapers, would they reach the same conclusion I did?” If the answer is no, you need more evidence.

The risk and materiality in audit relationship is one of the most tested concepts in professional exams and one of the most misapplied in practice. Understanding risk assessment impact on evidence decisions is a skill that separates competent auditors from exceptional ones.

Challenges: Edge cases, reliability issues, and best practices

Even with strong procedures, real-world audits face challenging edge cases and evidence reliability concerns. Here is how to manage them.

Common reliability risks include:

Management bias: Schedules prepared by management may reflect favorable assumptions. Always ask what incentives exist to present information a certain way.

Electronic records integrity: Digital files can be altered without obvious physical signs. Verify that IT controls protect the integrity of electronic evidence.

Conflicting sources: When two pieces of evidence point in opposite directions, you cannot simply pick the one that supports your conclusion.

Oral evidence gaps: Interview responses are not self-corroborating. Document them carefully and seek written or physical support wherever possible.

The INTOSAI Journal notes that evidence inconsistencies between sources require investigation, and doubts about reliability, including management bias and electronic records, demand integrity checks before conclusions can be drawn.

“Professional skepticism is not cynicism. It is a disciplined, questioning mindset that requires auditors to critically assess evidence rather than accept it at face value.”

When you encounter conflicting evidence, document the conflict, investigate the cause, and obtain additional corroborating evidence before concluding. Understanding audit dysfunction and evidence failures shows how often problems trace back to insufficient skepticism at the evidence-gathering stage.

Best practices for managing evidence challenges:

Maintain a clear chain of custody for all physical and electronic evidence.

Document your reasoning when you override or discount a piece of evidence.

Use a structured workpaper review process to catch gaps before the engagement closes.

Apply analytical procedures as a final cross-check, even when substantive testing looks clean.

Internal vs external audits: Scope and evidence differences

Before wrapping up, it is vital to distinguish how evidence expectations change between internal and external audits. The standards are consistent, but the application differs significantly.

External audits, governed by PCAOB or IAASB standards, focus on providing assurance to shareholders and regulators. The evidence bar is high because the opinion is public and carries legal weight. Internal audits, guided by IIA standards, often serve a consulting or improvement function. The audience is management and the board, not the public.

Key differences in scope and evidence:

External audits require evidence sufficient to support an opinion on financial statements. Independence and objectivity are non-negotiable.

Internal audits may focus on operational efficiency, control design, or compliance. Evidence requirements are shaped by the engagement objective.

Assurance engagements in internal audit still require sufficient and appropriate evidence, but the threshold is calibrated to the internal audience.

Consulting engagements may rely more heavily on inquiry and observation, with less emphasis on external confirmation.

The PCAOB AS1105 framework applies to external audits, but its principles of sufficiency and appropriateness are equally useful as a benchmark for internal audit work.

Factor | External audit | Internal audit |

Primary audience | Shareholders, regulators | Management, board |

Governing standard | PCAOB, IAASB | IIA Standards |

Evidence threshold | High, public opinion | Calibrated to objective |

Independence requirement | Strict | Organizational independence |

Engagement type | Assurance | Assurance and consulting |

Review the internal audit success principles and the external audit process to see how evidence strategies differ in practice across both functions.

Expand your audit expertise with professional training

Mastering audit evidence is not a one-time achievement. Standards evolve, risk environments shift, and professional judgment sharpens with structured learning and peer engagement. If you are ready to move from understanding the concepts to applying them with confidence, targeted CPE training is the most direct path.

At compliance-seminars.com, we offer internal auditor CPE events designed specifically for professionals who need practical, standards-based instruction. Our audit assurance training programs cover PCAOB, IIA, and IAASB standards with real-world application built in. You can also join us at in-person audit training events held across multiple U.S. cities, led by instructors with Big 4 backgrounds. Whether you need CPE credits or deeper technical skills, we have a format that fits your schedule and career goals.

Frequently asked questions

How do auditors decide how much evidence is enough?

Auditors apply professional judgment based on risk, materiality, and the quality of evidence already gathered. Research confirms that sufficiency judgments go well beyond simple rules of thumb and involve multiple professional considerations.

What makes audit evidence appropriate?

Evidence is appropriate when it is both relevant to the assertion being tested and reliable in its source. The PCAOB AS1105 standard defines appropriateness as the combination of relevance and reliability.

What are the most commonly used procedures for collecting audit evidence?

Audit evidence is typically collected through seven main procedures: inspection, observation, inquiry, confirmation, recalculation, reperformance, and analytical procedures. Each procedure serves a different assertion and carries a different reliability level.

How do auditors handle conflicting or unreliable evidence?

Auditors investigate the source of the inconsistency, apply professional skepticism, and seek additional corroborating evidence. The INTOSAI guidance on financial audits emphasizes that doubts about reliability must be resolved before conclusions are drawn.

Are evidence standards different for internal and external audits?

The core standards are consistent, but application differs by objective. External audits target public assurance, while internal audits often focus on consulting and improvement, as outlined in the PCAOB AS1105 framework.

Recommended

Comments