External Audit Process: Ensuring Financial Trust

- Леонид Ложкарев

- Feb 26

- 12 min read

Every audit leader knows the pressure to deliver financial statements that inspire real trust among stakeholders. In the United States financial services sector, the external audit process stands as the backbone for regulatory compliance and third-party independence. Grasping the structured phases and legal requirements is crucial for chief audit executives and external auditors to enhance audit quality, maintain objectivity, and satisfy rigorous standards that shape investor and regulator confidence.

Table of Contents

Key Takeaways

Point | Details |

External Audit Purpose | External audits provide independent verification of financial statements, ensuring stakeholders can trust the organization’s financial position. |

Independence of Auditors | Auditors must maintain complete independence to deliver objective evaluations, free from any management influence or conflicts of interest. |

Audit Cycle Phases | The audit cycle includes planning, risk assessment, fieldwork, reporting, and follow-up, each critical for thorough examination and compliance. |

Regulatory Compliance | Adhering to statutory requirements and accounting standards is essential for maintaining auditor credibility and ensuring public trust in financial reporting. |

External Audit Process Defined and Explained

An external audit is an independent examination of a company’s financial statements by auditors who have no involvement in day-to-day operations. These auditors assess whether financial records are accurate, complete, and presented fairly according to applicable accounting standards.

The core purpose is straightforward: provide stakeholders with confidence that financial statements reflect the true financial position of the organization. This confidence matters enormously for investors, regulators, lenders, and the public who rely on these statements to make decisions.

What Makes External Audits Different

External audits differ fundamentally from internal audits. Internal audits focus on improving processes and controls within your organization. External audits provide an objective, third-party opinion on financial accuracy and compliance.

Key distinctions include:

Independence: External auditors have no financial interest in your company’s operations or outcomes

Scope: They examine entire financial statements, not just operational improvements

Stakeholder focus: Results inform investors, regulators, and creditors, not just management

Regulatory requirement: Many organizations must conduct external audits by law

This independence is critical. Your auditors must remain unbiased throughout the engagement, which means they cannot serve in management roles or have personal relationships that could compromise their objectivity.

Here’s how external audits and internal audits compare in purpose and stakeholder impact:

Aspect | External Audit | Internal Audit |

Primary Objective | Financial statement accuracy | Process improvement and risk management |

Stakeholder Impact | Investors, regulators, public | Management and board |

Regulatory Requirement | Often legally required | Typically voluntary |

Independence | Complete third-party independence | May be part of the organization |

The Core Examination Process

External audit examinations involve testing transactions, verifying asset existence, and confirming liabilities. Auditors don’t examine every single transaction—they use sampling techniques to assess the overall accuracy of your financial statements.

The process includes:

Review accounting policies for consistency with standards

Test controls over financial transaction processing

Verify significant account balances through independent confirmation

Assess management’s estimates and judgments

Evaluate the overall presentation of financial statements

Why This Matters for Your Organization

External audits provide the independent verification that stakeholders need to trust your financial reporting and decision-making.

For financial services firms specifically, external audits demonstrate compliance with regulatory requirements and build stakeholder confidence. They identify weaknesses in controls, uncover potential fraud, and ensure your accounting practices align with regulatory standards.

Your auditors will ultimately issue an opinion stating whether your financial statements are fairly presented. This opinion carries significant weight with regulators, lenders, and investors in your sector.

Pro tip: Prepare comprehensive audit documentation before your fieldwork begins—organized transaction files, account reconciliations, and supporting schedules reduce audit time and costs while demonstrating your control environment strength.

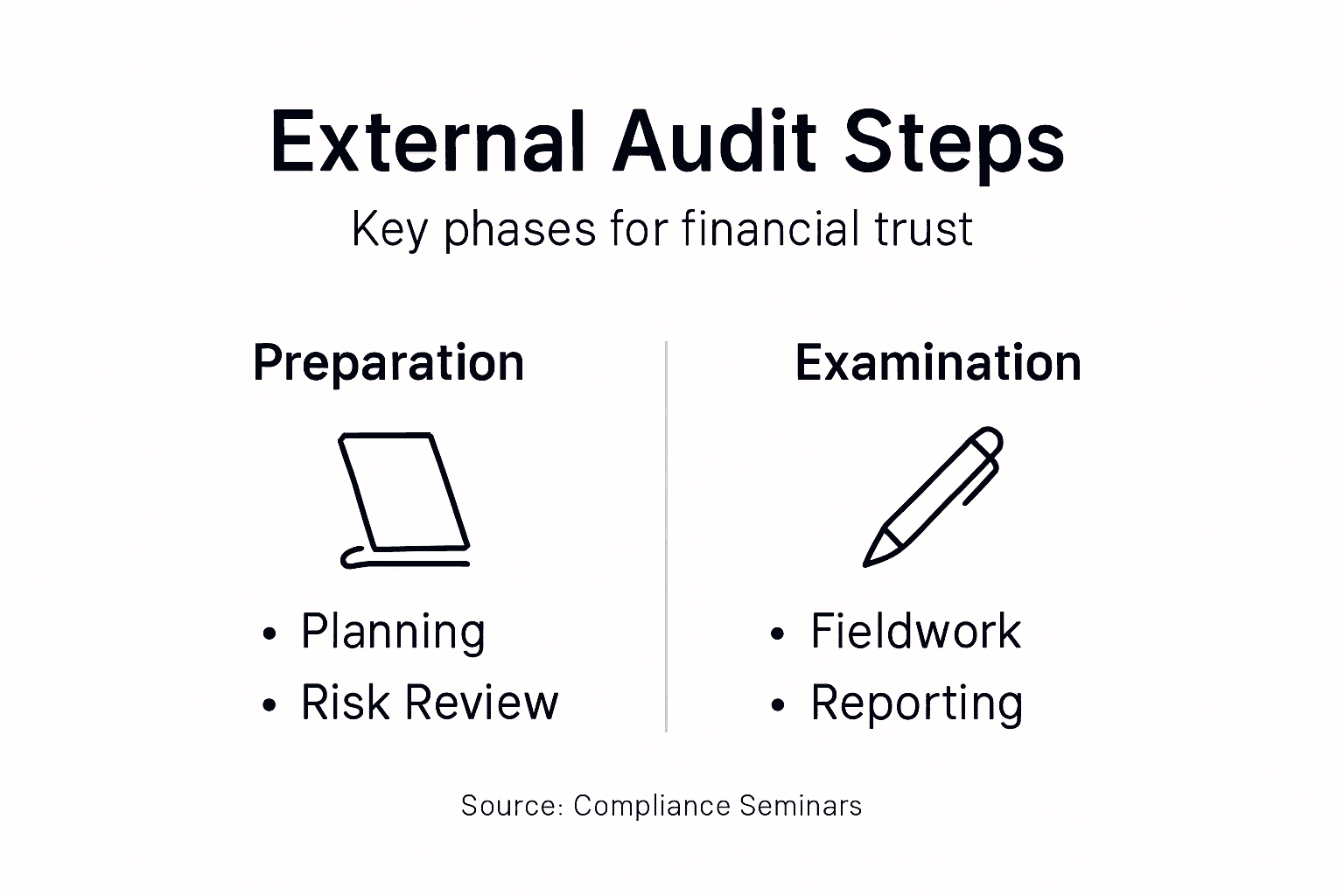

Major Steps in the External Audit Cycle

The external audit cycle follows a structured sequence designed to ensure thorough examination of your financial statements. Understanding each phase helps you prepare effectively and work collaboratively with your auditors to complete the engagement efficiently.

Phase 1: Planning

Planning sets the foundation for the entire audit. Your auditors gather background information about your organization, understand your business operations, and define the scope and objectives of the audit engagement.

During this phase, auditors will:

Review prior year audit findings and management letters

Understand your industry, regulatory environment, and business risks

Identify significant accounts and transaction cycles

Determine materiality levels and audit procedures

Establish timelines and resource requirements

This is your chance to communicate changes in your business, new systems implementations, or organizational restructurings that could affect the audit.

Phase 2: Risk Assessment

Risk assessment for auditors identifies where misstatements are most likely to occur. Your auditors evaluate both the design and operating effectiveness of your internal controls, then focus their testing efforts on high-risk areas.

Auditors examine:

Control activities over transaction processing

Segregation of duties in critical functions

Authorization and approval procedures

System access controls and security measures

This risk-focused approach allows auditors to concentrate resources where they matter most, rather than spreading effort across low-risk areas.

Phase 3: Fieldwork and Evidence Gathering

Fieldwork is where auditors actively test your financial records. They evaluate controls, test transactions, and collect evidence to support the amounts presented in your financial statements.

Key fieldwork activities include:

Testing internal controls over transaction processing

Selecting transactions and testing them for accuracy and proper authorization

Confirming account balances with external third parties

Verifying existence of assets through physical inspection

Evaluating management’s accounting estimates

Assessing the completeness and accuracy of account reconciliations

Effective fieldwork requires organized documentation and responsive management—delays in providing supporting evidence extend the audit timeline and increase costs.

Phase 4: Reporting

Reporting communicates audit findings to management and those charged with governance. Your auditors will issue an audit opinion on whether your financial statements are fairly presented in accordance with applicable accounting standards.

The report includes:

The auditor’s opinion on financial statement fairness

Any identified control deficiencies or material weaknesses

Significant accounting judgments or estimates

Compliance with applicable regulations

Phase 5: Follow-Up

Follow-up ensures management addresses findings and implements corrective actions. Auditors track whether previously identified issues have been resolved and verify the effectiveness of implemented solutions.

This phase demonstrates accountability and supports continuous improvement in your financial reporting and control environment.

This table summarizes the major phases of the external audit cycle and their contributions:

Phase | Key Activities | Purpose |

Planning | Scope setting, timeline, risk review | Prepares auditors, ensures engagement focus |

Risk Assessment | Control evaluation, risk targeting | Identifies critical audit areas |

Fieldwork | Evidence gathering, testing | Supports audit opinion with documentation |

Reporting | Opinion issuance, findings | Communicates results to stakeholders |

Follow-Up | Action review, issue tracking | Verifies corrective measures and progress |

Pro tip: Assign a single point of contact for audit requests and maintain a centralized location for supporting documentation—this dramatically reduces the back-and-forth communication and keeps your audit on schedule.

Legal Requirements and Regulatory Oversight

External audits operate within a complex web of legal frameworks and regulatory requirements designed to protect investors, creditors, and the public. As a chief audit executive or external auditor, understanding these obligations is not optional—they define how you conduct your work and what standards you must meet.

Statutory and Accounting Standards

Your external audits must comply with applicable accounting standards and statutory requirements established by your jurisdiction. These frameworks ensure consistency in how financial statements are prepared and audited across organizations.

Key compliance areas include:

Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS)

Statutory filing requirements and deadlines

Industry-specific accounting regulations

Jurisdictional requirements for financial statement presentation

The standards you follow depend on whether your organization is public, private, or in a specific regulated industry like banking or insurance.

Auditor Independence and Ethics

Regulatory frameworks mandate strict auditor independence requirements to ensure your opinion carries credibility. You cannot serve in management roles, maintain financial interests in your audit clients, or have relationships that compromise objectivity.

Independence requirements extend to:

Family relationships with client personnel

Prior employment at the audit client

Providing non-audit services that could bias your judgment

Financial relationships or investments in the client

These restrictions exist because stakeholders rely on your objectivity. Any perception of bias undermines the entire audit process.

PCAOB and SEC Oversight

Public company audits in the United States fall under the Public Company Accounting Oversight Board (PCAOB) and Securities and Exchange Commission (SEC) oversight. The PCAOB inspects audit firms, enforces auditing standards, and disciplines firms that fail to meet standards.

The Sarbanes-Oxley Act requires:

Auditor attestation on internal control effectiveness

Quarterly certifications from management

Auditor rotation after five years

Restrictions on non-audit services

Regular PCAOB inspections of audit firms

These requirements significantly impact how you structure your audit procedures and documentation.

Reporting Obligations

Your audit reports must include specific elements mandated by law and professional standards. For public companies, your audit opinion must address not only fair presentation of financial statements but also management’s assessment of internal control effectiveness.

Regulatory requirements dictate your audit opinion language, what you report to the audit committee, and timelines for submitting findings to regulators.

You must report significant deficiencies and material weaknesses in internal controls, and in certain situations, you have obligations to communicate directly with regulatory authorities rather than just management.

Navigating Jurisdictional Differences

If your organization operates across multiple jurisdictions, you face varying legal requirements. What applies in one state or country may differ significantly elsewhere. International standards aim to harmonize audit practices globally, but local regulations always take precedence.

Stay informed about:

Changes to auditing standards issued by the PCAOB or AICPA

New regulations affecting your industry

Jurisdiction-specific filing requirements

Updates to independence rules and ethics standards

Pro tip: Subscribe to PCAOB enforcement releases and inspection reports—they reveal common audit failures and help you avoid the same pitfalls that regulators are penalizing other firms for missing.

Roles, Responsibilities, and Key Stakeholders

External audits involve multiple parties with distinct roles and responsibilities. Understanding who does what—and why—helps you appreciate how audits serve different stakeholder needs while maintaining independence and objectivity.

The External Auditor’s Role

External auditors are independent professionals tasked with examining your financial statements and providing an objective opinion on their accuracy. They do not work for your organization; instead, they serve stakeholders who need confidence in your financial reporting.

Your auditors’ core responsibilities include:

Reviewing financial records for accuracy and completeness

Assessing compliance with accounting standards and regulations

Evaluating internal controls over financial reporting

Testing transactions and verifying account balances

Detecting and reporting misstatements or fraud

Issuing a formal audit opinion on financial statement fairness

External auditors maintain independence by adhering to professional standards and ethical principles throughout the engagement. They communicate audit findings clearly to management and those charged with governance.

Management’s Responsibilities

Management bears primary responsibility for financial statement accuracy and internal control effectiveness. You cannot delegate these duties to auditors—they verify your work but do not perform it.

Management must:

Prepare complete and accurate financial statements

Establish and maintain effective internal controls

Provide timely, honest responses to auditor inquiries

Disclose all known errors, irregularities, and fraud

Support auditors’ access to records, personnel, and facilities

Failure to fulfill these responsibilities undermines audit quality and raises red flags with regulators and stakeholders.

The Audit Committee

The audit committee serves as a bridge between management and external auditors. This independent board committee oversees audit planning, monitors audit progress, and receives audit findings before financial statements are finalized.

The audit committee ensures:

Auditor independence and appropriate firm rotation

Audit scope addresses key business risks

Management responds to audit findings promptly

Adequate resources support the audit process

Regulators expect audit committees to demonstrate genuine oversight, not rubber-stamp management decisions.

Key Stakeholders Relying on Audit Findings

External audit reports serve multiple audiences beyond management. Investors, creditors, regulators, and the public all depend on your auditor’s opinion when evaluating financial health and making decisions.

Stakeholders include:

Investors and shareholders: Use audit opinion to assess investment value

Lenders and creditors: Evaluate repayment ability and creditworthiness

Regulators: Verify compliance with financial reporting requirements

Government agencies: Monitor tax compliance and regulatory adherence

Public: Maintains confidence in financial market integrity

Your external auditor serves these stakeholders first—their primary obligation is not to management but to the broader investing public.

This stakeholder focus explains why auditors must remain independent from management pressure and why audit findings must be communicated clearly.

Pro tip: Ensure your audit committee meets with external auditors privately, without management present—this creates space for auditors to raise sensitive concerns and demonstrates genuine governance oversight to regulators.

Risks, Liabilities, and Best Practice Issues

External auditors operate in a high-stakes environment where professional judgment directly impacts stakeholder decisions. Understanding the risks you face, your legal liabilities, and best practice safeguards helps you conduct audits that withstand scrutiny and protect your firm’s reputation.

Detection Risks and Professional Judgment

Auditors face significant risks related to failing to detect material misstatements or fraud. You cannot examine every transaction, so you rely on sampling, analytical procedures, and professional skepticism to identify problems that management might overlook or intentionally conceal.

Key detection risks include:

Sophisticated fraud schemes designed to bypass controls

Creative accounting that technically complies with standards but misrepresents economic reality

Management override of controls that your testing assumes are operating

Collusion among multiple personnel to conceal misstatements

Complex transactions you do not fully understand initially

These risks demand ongoing professional education and robust audit methodologies. You must balance thoroughness with efficiency—auditors who spend too little time on high-risk areas expose themselves to liability, while those who over-test low-risk areas waste client resources and lose competitiveness.

Legal and Professional Liabilities

Auditor independence and regulatory compliance directly impact your firm’s legal exposure. Regulators impose liability mechanisms designed to ensure you maintain high standards and ethical conduct throughout engagements.

Liability sources include:

Failure to comply with auditing standards (PCAOB, AICPA)

Inadequate documentation supporting your conclusions

Insufficient professional skepticism when evaluating management representations

Violations of independence requirements

Poor communication of significant findings to those charged with governance

Regulators actively enforce these standards through inspections, enforcement actions, and fines against firms that fall short.

Fraud Detection and Professional Skepticism

Management fraud poses your greatest challenge. Unlike employee theft, management fraud often involves false financial statement assertions that sophisticated auditors must identify through careful analysis and healthy skepticism.

Effective fraud detection requires:

Questioning unusual transactions or account fluctuations

Understanding management incentives and pressures

Evaluating the tone at the top and control culture

Testing management-level controls and journal entries

Confirming significant transactions with third parties

Professional skepticism means assuming management is honest while remaining alert to evidence suggesting otherwise—not cynicism, but thoughtful verification.

Best Practices for Mitigating Risks

Top-performing audit firms address these risks through consistent practices that demonstrate quality and reduce liability exposure.

Best practices include:

Implementing standardized audit methodologies across all engagements

Requiring documented supervisory review of all significant conclusions

Maintaining robust engagement quality reviews before audit completion

Conducting regular training on emerging fraud schemes and accounting issues

Performing firm-wide inspections to identify deficiencies early

Maintaining clear engagement partner accountability for audit quality

Firms that invest in quality controls outperform competitors and build strong reputations with regulators.

Pro tip: Document your professional skepticism throughout the audit—explain why you accepted or rejected specific management representations, what evidence changed your audit approach, and how you addressed identified risks; this documentation demonstrates quality and protects your firm if findings are later questioned.

Strengthen Your External Audit Process with Expert Training

Navigating the complexities of the external audit process demands not only thorough knowledge but also practical skills to manage risk assessment, auditor independence, and regulatory compliance. This article highlights the critical steps and challenges auditors and management face to ensure financial trust. If you are seeking to sharpen your expertise in these key areas and master concepts like risk assessment for auditors, audit cycle phases, and professional skepticism this is your chance to gain that competitive edge.

Explore comprehensive courses, webinars, and seminars designed for audit professionals at Compliance Seminars tailored specifically to meet rigorous standards from CPA, CIA, and CISA certifications. Equip yourself with the tools to confidently execute external audits that satisfy regulatory requirements such as PCAOB and SEC oversight and learn best practices to mitigate legal liabilities while delivering clear audit reporting.

Take action now to enhance your audit effectiveness and build unwavering stakeholder confidence by visiting our learning platform. Unlock your potential with training grounded in real-world audit challenges and industry expertise. Your next audit cycle deserves your best preparation.

Frequently Asked Questions

What is the purpose of an external audit?

An external audit provides an independent examination of a company’s financial statements, ensuring they accurately reflect its financial position and comply with applicable accounting standards. This builds trust for stakeholders like investors, regulators, and creditors.

How is an external audit different from an internal audit?

External audits are performed by independent auditors who provide objective assessments of financial statements, while internal audits focus on improving internal processes and controls for management. External audits are often required by law, whereas internal audits are usually voluntary.

What are the major phases of the external audit process?

The external audit process typically consists of five major phases: Planning, Risk Assessment, Fieldwork and Evidence Gathering, Reporting, and Follow-Up. Each phase plays a critical role in ensuring a thorough examination of the financial statements.

What should organizations do to prepare for an external audit?

Organizations should prepare comprehensive documentation, including organized transaction files and supporting schedules, before the audit begins. This not only helps reduce audit time and costs but also demonstrates the strength of their control environment.

Recommended

Comments