What is continuous auditing? Methods, compliance & ROI

- John C. Blackshire, Jr.

- Mar 31

- 9 min read

Updated: Apr 8

Most audit professionals were trained to think of an audit as a point-in-time event. You gather evidence, test controls, write findings, and move on. But that model is increasingly out of step with the speed of modern business risk. Recent studies show continuous auditing delivers measurable ROI and efficiency gains that periodic audits simply cannot match. This article covers what continuous auditing actually is, how it works technically, how it aligns with SOX, PCAOB, and AICPA standards, what the evidence says about its real-world results, and how you can start integrating it into your internal controls program.

Table of Contents

How continuous auditing works: Methodologies and technical foundations

Continuous auditing and regulatory compliance: SOX, PCAOB, and AICPA alignment

ROI, case studies, and critical limitations of continuous auditing

How to integrate continuous auditing into internal controls and compliance programs

Advance your audit skills with expert-led CPE and compliance training

Key Takeaways

Point | Details |

Continuous auditing defined | It is ongoing, technology-enabled assurance that replaces periodic and manual audit steps with real-time monitoring. |

Enables regulatory alignment | Continuous auditing supports SOX Section 404, PCAOB, and AICPA standards for stronger compliance evidence. |

ROI and efficiency | Case studies show reduced control failures, cost savings, and faster response to risk than periodic audits. |

Not one-size-fits-all | Some areas require traditional audits due to data limits, judgment needs, or skills gaps that technology alone can’t solve. |

Actionable next steps | Success demands skilled teams, strong IT controls, and phased implementation tailored to your current audit environment. |

Defining continuous auditing: What it is and why it matters

Continuous auditing is a technology-enabled approach that allows auditors to collect and evaluate evidence on an ongoing basis rather than at scheduled intervals. Think of it as shifting from a quarterly snapshot to a live feed. The goal is to detect anomalies, control failures, and compliance gaps in near real time, rather than weeks or months after the fact.

The distinction from traditional auditing is significant. Periodic audits rely on sampling and retrospective analysis. Continuous auditing, by contrast, provides written assurance over time rather than through a single engagement, enabling auditors to maintain independent oversight across the full transaction population.

Feature | Traditional auditing | Continuous auditing |

Frequency | Periodic (quarterly/annual) | Ongoing or near real-time |

Coverage | Sample-based | 100% of transactions |

Detection speed | Weeks to months | Hours to days |

Evidence collection | Manual or batch | Automated data feeds |

Anomaly response | Reactive | Proactive |

The core benefits are worth stating plainly:

Proactive anomaly detection before issues escalate into material findings

Full population testing rather than statistical sampling

Improved compliance posture through continuous evidence trails

Faster response cycles that align with how regulators now expect controls to operate

Organizations that adopt continuous auditing report measurable reductions in control failures and faster identification of fraud indicators, fundamentally changing the value audit delivers to the business.

For professionals looking to strengthen their foundation, audit excellence with CCS training and a solid internal controls implementation guide are practical starting points. You can also explore a dedicated course on continuous auditing and monitoring to go deeper on the mechanics.

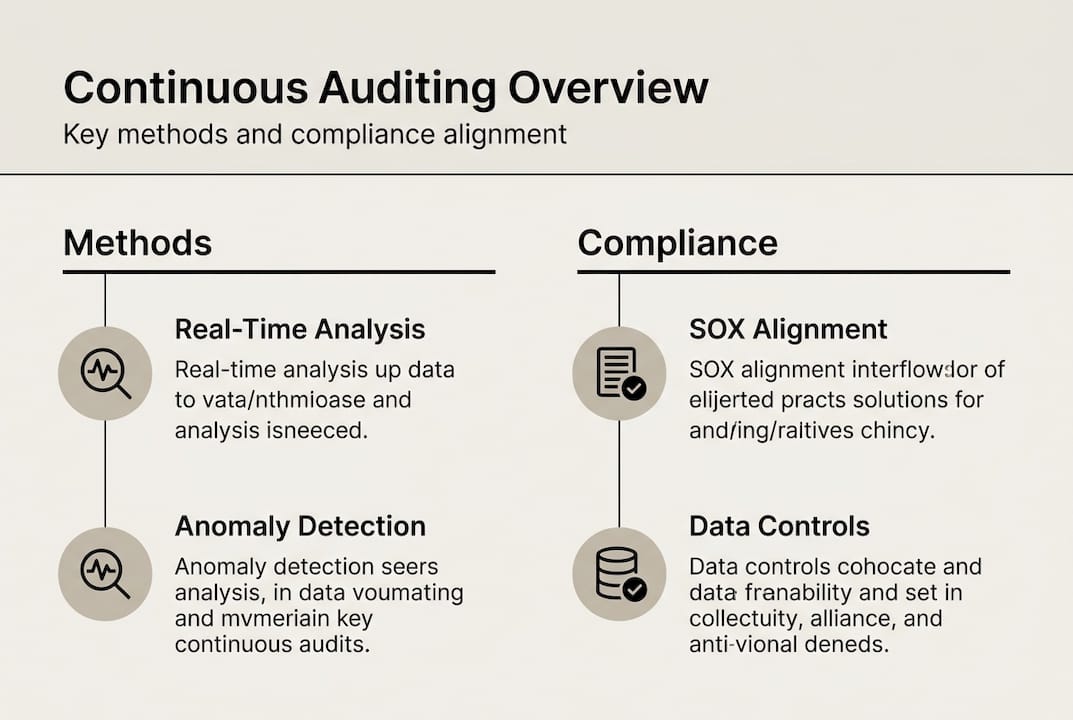

How continuous auditing works: Methodologies and technical foundations

Understanding the technical architecture behind continuous auditing helps you evaluate what your organization actually needs to implement it. The methodology rests on three core components working together.

Core methodologies include real-time transaction analysis, electronic record validation, and anomaly detection using analytics and AI. These are not separate tools but interconnected layers of a single audit infrastructure.

Technique | Function | Example use case |

API/ETL data feeds | Pull live data from source systems | ERP transaction ingestion |

Rule-based alerts | Flag transactions outside defined parameters | Duplicate payments, threshold breaches |

AI/ML analytics | Detect patterns and outliers at scale | Vendor fraud, unusual journal entries |

Automated controls testing | Assess control effectiveness continuously | Segregation of duties monitoring |

Here is how these components interact in a typical implementation:

Data feed integration. Connect your ERP, financial systems, and operational databases through API or ETL (extract, transform, load) pipelines to create a continuous data stream.

Automated controls assessment. Define control rules and thresholds within the audit platform. The system tests every transaction against these rules without manual intervention.

Exception and anomaly detection. When a transaction or pattern falls outside expected parameters, the system generates an alert for auditor review, prioritized by risk level.

Auditor review and response. Auditors investigate flagged items, document conclusions, and update control assessments in near real time.

For a deeper look at how AI fits into this picture, AI tools in internal auditing and data analytics transforms auditing are worth reviewing. The PCAOB guidance on tech-forward audit practices also outlines where the profession is heading.

Pro Tip: Do not try to automate everything at once. Start with one high-risk process, such as accounts payable or journal entry review, where anomaly detection delivers immediate value. Build confidence and internal buy-in before scaling firmwide.

Continuous auditing and regulatory compliance: SOX, PCAOB, and AICPA alignment

Regulators have not yet mandated continuous auditing by name, but the direction is clear. The frameworks governing internal controls and audit quality increasingly assume that technology-enabled, ongoing testing is the standard of care, not the exception.

Continuous auditing aligns directly with U.S. regulations including SOX Section 404 ICFR (Internal Controls over Financial Reporting), PCAOB AS 2201, and AICPA SAS 145. Each of these frameworks emphasizes the need for robust, evidence-based assessments of control effectiveness, which continuous auditing supports more thoroughly than periodic testing alone.

Here is where continuous auditing provides direct regulatory support:

SOX Section 404: Requires management and auditors to assess ICFR effectiveness. Continuous testing provides a richer, more defensible evidence base.

PCAOB AS 2201: Governs the audit of internal control over financial reporting. Ongoing monitoring strengthens the auditor’s ability to identify control deficiencies early.

AICPA SAS 145: Updated risk assessment standards that expect auditors to use data analytics and technology where available.

COSO framework: Continuous monitoring directly supports the Monitoring Activities component of the COSO Internal Control framework.

78% of Chief Audit Executives (CAEs) cite data analytics capability as a top gap in their continuous audit programs. That gap is not just a skills issue. It reflects the cultural and structural lag between what regulators expect and what most internal audit functions currently deliver.

For professionals managing SOX compliance and internal controls, continuous auditing is not a future-state aspiration. It is a present-day competitive and compliance necessity.

ROI, case studies, and critical limitations of continuous auditing

The business case for continuous auditing is backed by real numbers. Empirical benchmarks from recent case studies show 100% ROI on implementation costs, a 42% reduction in control failures, and a $127,000 per unit reduction in write-offs following adoption. These are not theoretical projections. They reflect documented outcomes from organizations that made the investment.

In practice, firms that implemented continuous auditing in accounts payable reported detecting duplicate invoices and vendor fraud within days rather than during the next audit cycle. Others used it to monitor compliance with procurement policies across thousands of transactions weekly, something no sample-based approach could achieve.

Organizations implementing continuous auditing consistently report that the speed of detection alone justifies the investment, independent of the direct cost savings.

That said, honest evaluation requires acknowledging where continuous auditing falls short. It is not suitable for all audit areas and introduces its own risks around skills, independence, and cost.

Key limitations to plan for:

Data quality dependencies: Garbage in, garbage out. If source system data is inconsistent or incomplete, continuous auditing will generate noise rather than insight.

IT general controls (ITGCs): Weak ITGCs undermine the reliability of automated audit evidence. You must address the control environment before layering on continuous monitoring.

Higher initial costs: Technology licensing, integration work, and training require upfront investment that not all organizations can absorb quickly.

Independence challenges: Auditors who design the monitoring rules may face independence questions if they also rely on those rules for assurance conclusions.

Judgment-intensive areas: Continuous auditing works best for rule-based, high-volume processes. It is less effective for areas requiring significant professional judgment.

Pro Tip: Before adoption, build a cross-functional team that includes IT, finance, and internal audit. Invest in upskilling your auditors on data interpretation. The technology is only as good as the people interpreting its output. Use the audit efficiency checklist to assess your current readiness.

How to integrate continuous auditing into internal controls and compliance programs

Knowing the benefits and limitations is one thing. Building a practical path forward is another. The good news is that you do not need to overhaul your entire audit function to start. A phased approach works well and reduces the risk of implementation failure.

Strong data quality, ITGCs, and auditor skills are foundational requirements. Without them, even the best continuous auditing platform will underdeliver. Address these before you scale.

Here is a four-phase implementation framework:

Readiness assessment. Evaluate your current data infrastructure, ITGC maturity, and auditor skill levels. Identify the highest-risk processes where continuous auditing would deliver the most value.

Design. Select your platform or toolset, define control rules and alert thresholds, and map data sources to audit objectives. Involve IT and compliance stakeholders from the start.

Pilot. Launch in one process or business unit. Monitor alert volumes, false positive rates, and auditor response times. Refine your rules based on early results.

Review and scale. After 90 days, assess what worked and what did not. Expand to additional processes with lessons learned applied. Build training into each expansion phase.

Data privacy and ITGC integrity remain foundational throughout. Every automated alert is only as reliable as the controls governing the underlying data. Do not skip that foundation in the rush to scale.

For ongoing guidance, the internal controls best practices resource and the CPE insights blog offer practical frameworks that align with where the profession is heading.

Pro Tip: Start with one process and build momentum through early wins. A successful pilot in accounts payable or payroll creates the internal credibility you need to expand the program with leadership support.

Why conventional audit wisdom may be holding you back

Here is an uncomfortable truth most audit leaders avoid saying out loud: the biggest risk in auditing today is waiting for perfect conditions while fraud and errors go unchecked.

We hear the objections regularly. The cost is too high. The technology is not mature enough. The disruption is not worth it. But these objections consistently overestimate the risk of acting and underestimate the cost of waiting. Every month without continuous monitoring is a month where anomalies compound, control failures go undetected, and your audit function delivers less value than it could.

Audit culture that waits for regulatory mandates before adopting better methods is not being cautious. It is being slow. The firms and internal audit functions that experiment early build skills, refine processes, and improve control environments faster than those that hold back.

Continuous auditing is not just a compliance tool. It is a path to genuine audit excellence, and it changes how leadership perceives the audit function’s value. Explore how leveraging AI in audit fits into this broader shift. The professionals who lead this change will define what high-quality auditing looks like for the next decade.

Advance your audit skills with expert-led CPE and compliance training

If this article has clarified what continuous auditing can do for your organization, the logical next step is building the skills to implement it well. Understanding the concept is only the beginning. Executing it requires hands-on knowledge of data analytics, control frameworks, and regulatory alignment.

At compliance-seminars.com, we offer internal auditor CPE webinars and in-person courses designed specifically for audit and compliance professionals navigating these changes. Check the CPE event calendar to find upcoming sessions on continuous auditing, internal controls, and data analytics. Whether you are just starting or looking to scale an existing program, explore all CPE training options to find the right fit for your team.

Frequently asked questions

How does continuous auditing improve internal controls?

Continuous auditing enables real-time testing and full-transaction coverage, helping organizations quickly identify and address control failures before they become material findings.

Is continuous auditing required by SOX or PCAOB?

While not formally mandated, continuous auditing aligns closely with SOX 404, PCAOB AS 2201, and modern risk assessment standards, often supporting more robust and defensible compliance evidence.

What are the limitations of continuous auditing?

It requires high-quality data, strong IT general controls, and skilled auditors, and it may not suit audit areas that depend heavily on professional judgment rather than rule-based testing.

Does continuous auditing reduce audit costs?

Studies show significant ROI along with reduced control failures and write-offs, though initial investments in technology and training are required before those savings materialize.

Recommended

Comments