Audit Report Writing Guide for Audit Professionals

- John C. Blackshire, Jr.

- May 23

- 9 min read

TL;DR:

Effective audit reports require clear structure, including an executive summary, introduction, findings with the 5 Cs framework, conclusions, and actionable recommendations. Preparing thoroughly beforehand and focusing on concise, audience-appropriate writing aligned with 2026 standards enhances report impact and compliance. Leveraging technology, avoiding common pitfalls, and treating report writing as a communication skill drive action and professional credibility.

Most auditors know their findings cold. The challenge is translating that technical knowledge into a report that a CFO, audit committee, or regulatory reviewer can act on quickly. A well-built audit report writing guide closes that gap, giving you a repeatable framework for structuring findings, writing with clarity, and meeting the compliance expectations that IIA GAIS Domain V and PCAOB QC 1000 set for 2026. This guide covers all of it: preparation, structure, writing style, common mistakes, and the quality control requirements shaping audit reporting right now.

Table of Contents

Key takeaways

Point | Details |

Prepare before you draft | Confirm audit objectives, evidence sufficiency, and report outline approval before writing a single section. |

Use the 5 Cs framework | Structure every finding around criteria, condition, cause, consequence, and corrective action for consistent presentation. |

Write for your reader | Use plain language and a constructive tone so non-technical stakeholders can understand and act on your findings. |

Stay current on standards | PCAOB QC 1000 annual evaluation and IIA GAIS Domain V reporting requirements take full effect in 2026. |

Deliver on time | Reports issued within 3 to 5 business days of fieldwork completion drive faster corrective action from management. |

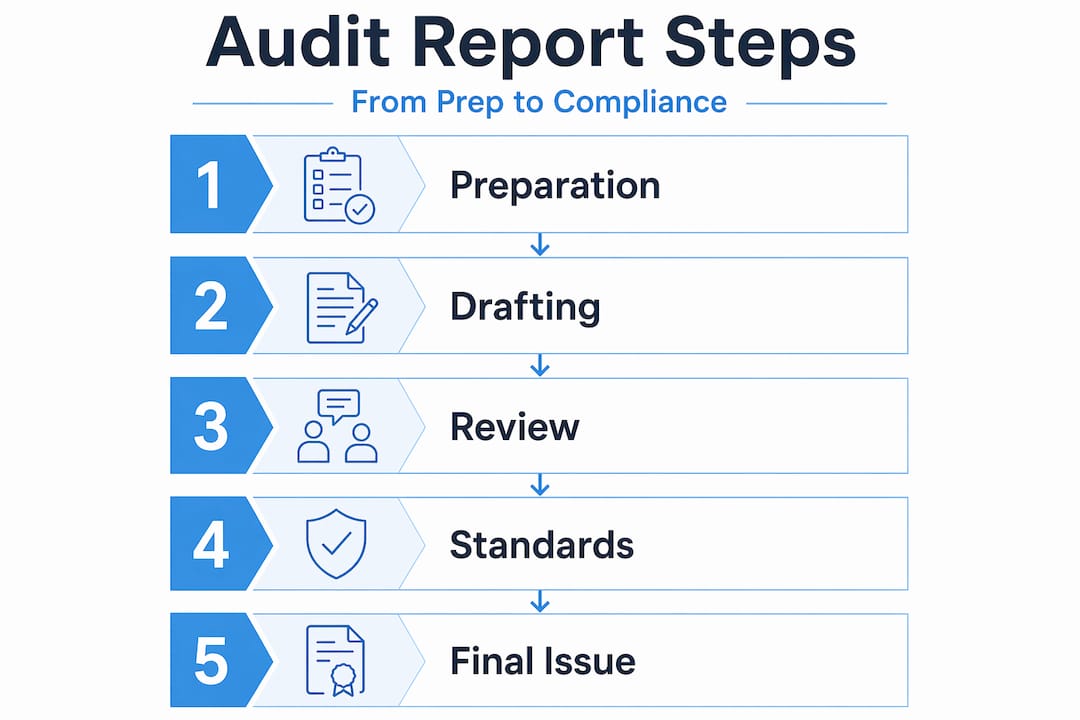

Your audit report writing guide starts with preparation

The biggest drafting problems do not start during drafting. They start before it. When audit objectives are vague, when evidence hasn’t been fully tested for sufficiency, or when reviewers haven’t signed off on the report outline, the writing process turns into an expensive rework cycle.

Audit report drafting works best as an iterative process that begins with outline approval and evidence sufficiency checks before any full drafting begins. That outline is more than a table of contents. It links each planned observation directly to the criteria and evidence supporting it, which filters out unsupported claims early, before they find their way into a draft and require painful revision later.

Before you write, confirm the following:

Audit objectives and scope are documented and agreed upon with engagement leadership

Evidence sufficiency has been assessed at the finding level, not just overall

Materiality thresholds and severity definitions are established and consistently applied

Report format has been selected and approved (short-form, long-form, or memo-style)

Reviewer assignments are in place so that subject matter reviewers and quality control reviewers both have defined roles

The reviewer’s role during preparation is often underestimated. Getting a non-auditor to read the draft outline, not just the finished draft, surfaces clarity problems at the lowest possible cost.

Pro Tip: Create a one-page report outline that maps every planned finding to its supporting evidence before drafting. If you cannot fill in that map cleanly, you do not yet have a reportable finding.

Core structure of an effective audit report

Understanding how to write an audit report starts with knowing what every section must accomplish. Readers skim. Decision-makers read selectively. Your structure has to deliver the right information at every level of engagement.

Here are the core components every audit report should include, in order:

Executive summary. This goes first but gets written last. It should fit on a single page and answer five questions: why the audit was performed, what was tested, what was found (with severity counts), the overall conclusion, and what happens next. The executive summary functions as an answer sheet for management, and it needs to prioritize conclusions over background.

Introduction. State the audit’s scope, objectives, and methodology. This section tells readers what you examined and how. Keep it factual and brief.

Findings section. This is where the 5 Cs framework earns its value. The 5 Cs of audit observations, which are criteria, condition, cause, consequence, and corrective action, create a consistent structure for every finding that makes severity ratings and management responses far easier to track.

Conclusion and opinion. State your overall assessment plainly. If you are writing a financial audit report, this is where your opinion on financial statement accuracy lives. For operational or compliance audits, summarize overall risk exposure.

Recommendations. Every recommendation must be specific, assigned to an owner, and tied to a timeline. Vague recommendations are not recommendations. They are wishes.

Pro Tip: Use visuals and tables to summarize finding severity counts and status in the executive summary. A simple dashboard view lets executives scan your key message in under 60 seconds.

The table below compares two approaches to documenting a single finding, one that uses the 5 Cs and one that does not:

Approach | Example | Reader Impact |

Without 5 Cs | “Access controls were insufficient.” | No context, no cause, no path forward. |

With 5 Cs | Criteria: Policy requires MFA. Condition: 40% of admin accounts lack MFA. Cause: No enforcement mechanism. Consequence: Elevated breach risk. Action: Implement MFA enforcement by Q3 2026. | Clear, prioritized, actionable. |

Writing style that builds credibility and drives action

Even a well-structured report fails if the writing alienates your audience. Audit reports reach many different readers, including board members, operations managers, external regulators, and finance teams. That range demands a style that is clear to all of them without being condescending to any.

The European Court of Auditors drafting guidance defines good audit reports as objective, complete, clear, convincing, relevant, accurate, constructive, and concise. Notice that “technically impressive” is not on that list. Clarity and usefulness outrank complexity every time.

A few principles to apply:

Write to a general professional audience. If a finding cannot be explained without three paragraphs of technical setup, the finding itself needs to be restructured.

Use a constructive tone, not a prosecutorial one. Objective reports avoid blaming management and focus on facts with appropriate weight given to both strengths and weaknesses. A blame-forward report gets rejected. A fact-forward report gets acted on.

Keep sentences short and paragraphs focused. Aim for one idea per paragraph. If your paragraph covers three distinct points, split it.

Avoid acronyms without introduction. Define every term the first time it appears, even terms you consider standard.

Build in a readability review. Before finalizing, have someone outside the audit team read the report and flag any sentences they had to read twice.

The iterative review process is not a sign of weak drafting. It is a sign of professional rigor. Every pass tightens logic, removes ambiguity, and strengthens the credibility of your conclusions.

Pro Tip: After completing a draft, read the executive summary and recommendations aloud. If you stumble or lose your place, your reader will too. Rewrite until both sections flow without hesitation.

Compliance with 2026 audit reporting standards

Two regulatory developments reshape audit report writing requirements in 2026. If you are not already building them into your process, you are behind.

The first is PCAOB QC 1000, which requires registered public accounting firms to perform annual quality control evaluations and report their results beginning December 15, 2025. This standard has direct implications for how audit documentation is maintained, how engagement deficiencies are tracked post-issuance, and how firm leadership is held accountable for quality failures. Compliance-seminars has published detailed preparation guidance for firms working through the QC 1000 implementation process.

The second is IIA GAIS Domain V, which governs how internal audit functions communicate results. Domain V sets expectations for report content, timeliness, and the communication of significant risk exposures. Internal auditors who rely on outdated IIA standards are producing reports that fall short of current professional expectations.

The table below summarizes where each standard impacts your reporting process:

Standard | Key Reporting Requirement | Impact Area |

PCAOB QC 1000 | Annual QC evaluation and reporting; respond to post-issuance deficiencies | Documentation, leadership accountability |

IIA GAIS Domain V | Communicate results clearly, timely, and with appropriate risk context | Report content, delivery, format |

AS 2901 | Document how engagement deficiencies are identified and addressed | Post-issuance review and correction processes |

Integrating these standards into your drafting workflow is not a separate compliance exercise. Reviewing your report against these requirements should be a standard checklist step before any report is issued.

For teams looking to get hands-on training on these standards, the PCAOB QC 1000 CPE training offered through Compliance-seminars covers the specifics in a format designed for practicing auditors.

Common pitfalls and how to avoid them

Even experienced auditors fall into habits that undermine their reports. Recognizing these patterns is the first step toward fixing them.

Too much background, too little finding. Some reports spend two pages explaining the regulatory environment before presenting a single finding. That context belongs in an appendix, not the opening section.

Inconsistent severity ratings. Using “high,” “critical,” and “significant” interchangeably across a report destroys credibility. Define your rating scale in the introduction and apply it uniformly.

Missing the audience. A report written for an IT security team will not land with an audit committee. Know who your primary reader is and write to their level of technical familiarity.

Late delivery. Reports issued within 3 to 5 business days after fieldwork completion encourage prompt corrective action. Reports issued three weeks later become historical documents.

Ignoring technology support. AI tools can draft sections, standardize language, and summarize fieldwork notes effectively. Use them to handle routine writing tasks, and redirect that time toward analysis and stakeholder communication.

Pro Tip: Before issuing, run your report through an audit report checklist that verifies every finding has a severity rating, an owner, a deadline, and a management response. If any of those four elements are missing, the finding is not ready to publish.

My honest take on where audit reports actually fail

I have reviewed hundreds of audit reports over the years, and the failure pattern is almost always the same. It is not a lack of knowledge. It is a disconnect between what the auditor found and what the reader needs to do.

Reports get dense because auditors are trained to document everything. That habit protects you during a regulatory review, but it buries the reader when the report is 45 pages long and the three findings that actually matter are on pages 28 through 31. The reports I have seen drive real change are the ones where the writer made a deliberate choice about what to foreground and what to move to the appendix.

The transition to PCAOB QC 1000 and IIA GAIS Domain V is forcing a useful reckoning. These standards require auditors to account for quality, not just completeness. That means leadership accountability for report quality is now a documented expectation, not an informal norm. I think that is genuinely good for the profession.

What I have learned from watching teams navigate these changes is that the auditors who adapt fastest are the ones who treat report writing as a communication skill, not just a documentation task. They read their reports the way a skeptical CFO would. They cut aggressively. They test their recommendations against the question “Is this specific enough for someone to act on tomorrow?” If the answer is no, they rewrite.

That discipline, more than any template or checklist, is what separates reports that collect dust from reports that drive action.

— John

Sharpen your audit reporting skills with CPE training

Writing effective audit reports is a skill that develops through practice, feedback, and exposure to current standards. Compliance-seminars offers in-person CPE audit training events across multiple U.S. cities, with courses specifically focused on audit report writing, PCAOB quality control standards, and IIA reporting requirements. For professionals who prefer a shorter format, the internal auditor CPE webinars deliver focused, one to two credit sessions on audit writing and compliance topics. All courses are NASBA-recognized and built for CPA, CIA, and CFE professionals who need practical, standards-based instruction they can apply immediately. Explore the art of internal audit report writing course for a deep dive into the craft.

FAQ

What is the standard structure of an audit report?

A standard audit report includes an executive summary, introduction, findings section using the 5 Cs framework, conclusion or opinion, and recommendations with assigned owners and timelines.

How do the 5 Cs improve audit findings documentation?

The 5 Cs, which are criteria, condition, cause, consequence, and corrective action, provide a consistent structure for every finding, making severity ratings easier to apply and management responses easier to track.

What does PCAOB QC 1000 require for audit reporting in 2026?

PCAOB QC 1000 requires registered firms to complete annual quality control evaluations and reporting beginning December 15, 2025, with direct implications for documentation standards and leadership accountability.

How soon should an audit report be issued after fieldwork?

Audit reports should be issued within 3 to 5 business days after fieldwork completion to maintain relevance and encourage timely corrective action from management.

How can auditors use AI in report writing without losing quality?

AI tools can draft sections, standardize language, and summarize notes effectively, but professional judgment must govern all conclusions and recommendations. Use AI for efficiency, not as a substitute for expert analysis.

Recommended

Comments