Why Internal Controls Matter for Auditors

- Леонид Ложкарев

- Feb 8

- 7 min read

Every multinational corporation faces ongoing pressure to maintain financial integrity and meet regulatory demands across diverse markets. Strengthening internal control frameworks becomes more than a checkbox exercise when risks range from data breaches to financial misstatements. This overview clarifies what effective internal controls truly mean, dispels common misconceptions, and highlights practical strategies that help internal auditors and compliance officers support their organizations’ long-term compliance and operational resilience.

Table of Contents

Key Takeaways

Point | Details |

Importance of Internal Controls | Internal controls are essential for protecting resources, ensuring financial accuracy, and maintaining compliance with regulations. |

COSO Framework | The COSO Framework provides a structured approach for implementing internal controls focused on evaluation and continuous improvement. |

Control Types | Utilize a balanced approach that includes preventive, detective, and corrective controls for robust risk management. |

Addressing Weaknesses | Regularly assess and improve internal control systems to mitigate vulnerabilities and reduce organizational risks. |

Internal Controls: Core Definition And Misconceptions

Internal controls represent a systematic framework designed to protect organizational resources, ensure reliable financial reporting, and maintain regulatory compliance. Far more than mere bureaucratic procedures, these mechanisms provide a strategic approach to managing operational risks and maintaining business integrity.

At its core, an internal control system encompasses policies, procedures, and practices implemented by an organization to achieve several critical objectives:

Financial Reporting Accuracy: Ensuring financial statements are accurate, complete, and reliable

Operational Efficiency: Promoting effective and efficient business operations

Regulatory Compliance: Adhering to applicable laws, regulations, and internal policies

Asset Protection: Safeguarding organizational assets from potential fraud or misuse

Contrary to common misconceptions, internal controls are not about creating unnecessary barriers or displaying distrust. Instead, they represent a proactive risk management strategy that provides reasonable assurance rather than absolute guarantees. Organizations across all sizes and industries require robust internal control frameworks.

Most professionals misunderstand internal controls as rigid, bureaucratic processes that impede business performance. However, effective controls are dynamic and adaptable, designed to support organizational goals while mitigating potential risks. They are not about restricting activities but creating structured environments where strategic objectives can be achieved systematically and securely.

Pro tip: Treat internal controls as living systems that evolve with your organization’s changing needs, not static rulebooks.

COSO Framework And Main Control Types

COSO (Committee of Sponsoring Organizations of the Treadway Commission) represents a pivotal framework for understanding and implementing comprehensive internal control strategies across organizations. Established as a systematic approach to internal controls, the framework provides organizations with a structured methodology to evaluate and enhance their risk management processes.

The COSO Framework comprises five interconnected components that form a holistic approach to internal controls:

Control Environment: Sets the tone of an organization, establishing fundamental principles of integrity and ethical standards

Risk Assessment: Identifies and analyzes potential risks that could impact organizational objectives

Control Activities: Implements specific policies and procedures to mitigate identified risks

Information and Communication: Ensures relevant information flows effectively throughout the organization

Monitoring: Continuously evaluates the effectiveness of internal control systems

Each component plays a critical role in creating a robust internal control system. The control environment, for instance, serves as the foundation, representing the organizational culture and leadership’s commitment to maintaining high standards of governance. Risk assessment allows organizations to proactively identify potential vulnerabilities, while control activities translate risk management strategies into actionable procedures.

Professionals should understand that the COSO Framework is not a static document but a dynamic system that requires continuous refinement. Organizations must regularly reassess their internal controls to ensure they remain aligned with changing business landscapes, technological advancements, and emerging regulatory requirements.

Pro tip: Conduct periodic comprehensive reviews of your COSO Framework implementation to ensure continuous improvement and adaptation.

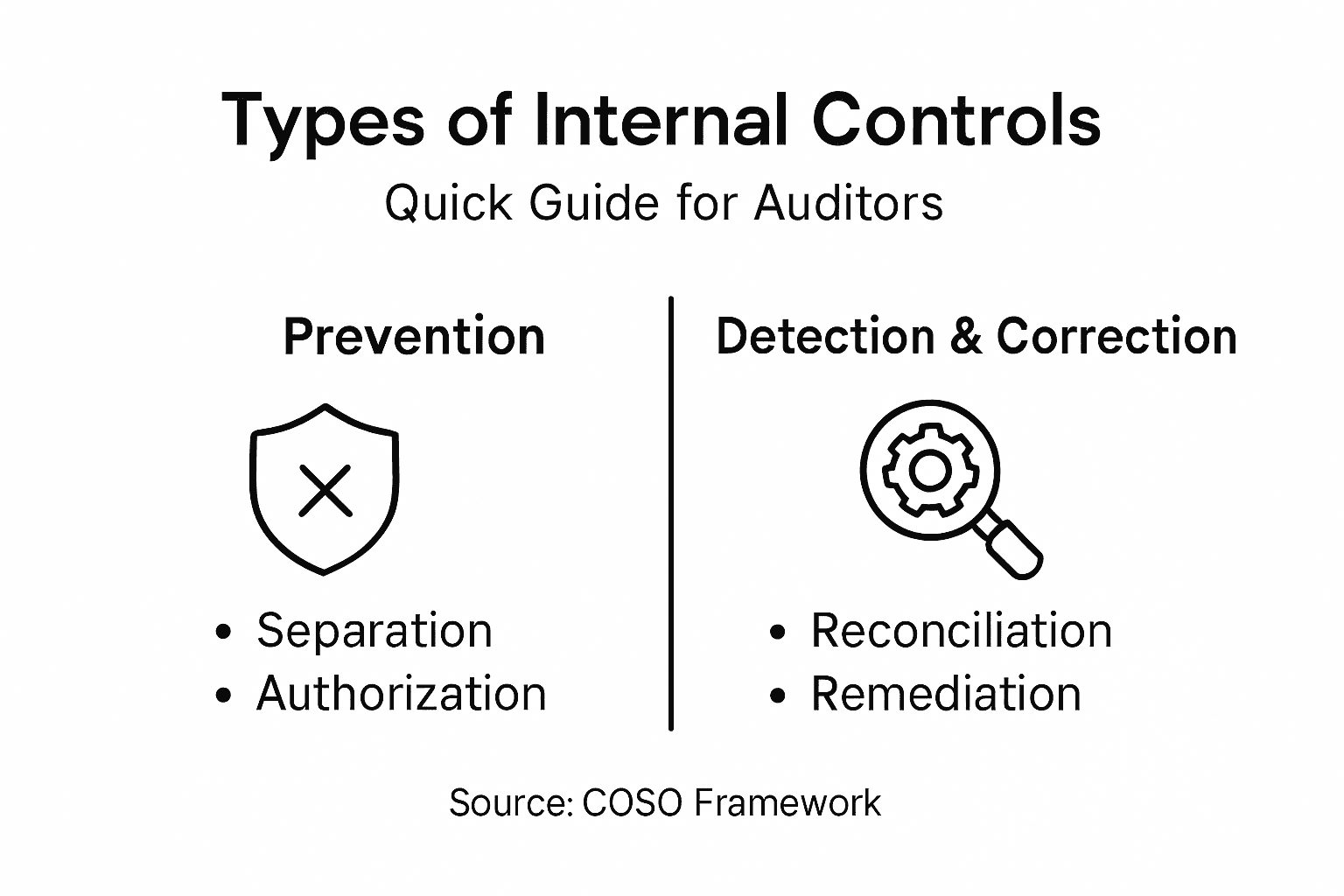

Preventive, Detective, And Corrective Controls Explained

Internal control strategies encompass three critical types of controls that work together to protect organizational resources and manage potential risks. Control mechanisms play a crucial role in creating a comprehensive approach to risk management and operational integrity.

The three primary types of internal controls include:

Preventive Controls: Stop potential risks before they occur

Access restrictions

Segregation of duties

Authorization requirements

Strong authentication protocols

Detective Controls: Identify and highlight existing issues

Regular audits

Performance reviews

Log monitoring

Reconciliation processes

Corrective Controls: Address and resolve identified problems

Incident response plans

System restoration procedures

Root cause analysis

Vulnerability patch management

Preventive controls serve as the first line of defense, creating barriers that minimize the likelihood of errors, fraud, or security breaches. These proactive measures are designed to stop potential issues before they can impact the organization. Detective controls, by contrast, function like organizational watchdogs, continuously monitoring systems and processes to quickly identify any deviations from expected standards or potential irregularities.

Here’s a summary comparing the three main types of internal controls and their organizational benefits:

Control Type | Primary Purpose | Typical Outcome | Example Benefit |

Preventive | Block risks before they arise | Reduces chances of fraud or error | Protects key resources |

Detective | Identify incidents or issues | Exposes irregularities quickly | Enables fast corrections |

Corrective | Respond to discovered problems | Restores operations after issues | Minimizes business impact |

Corrective controls represent the organization’s responsive strategy, focusing on minimizing damage and preventing future recurrences after an issue has been detected. These controls are critical for maintaining organizational resilience, allowing businesses to learn from incidents and continuously improve their risk management approach.

Pro tip: Implement a balanced approach that integrates all three control types to create a robust and dynamic risk management strategy.

Internal Controls And Regulatory Compliance Requirements

Regulatory compliance represents a critical dimension of organizational risk management, requiring sophisticated internal control mechanisms to ensure adherence to complex legal standards. Establishing comprehensive compliance frameworks demands strategic approaches that integrate systematic monitoring and continuous improvement.

Key regulatory compliance requirements typically involve multiple critical domains:

Data Protection Standards

GDPR requirements

HIPAA privacy regulations

Personal information security protocols

Financial Reporting Regulations

Sarbanes-Oxley (SOX) compliance

SEC disclosure requirements

Internal financial control standards

Industry-Specific Compliance

Banking regulations

Healthcare compliance protocols

Technology sector reporting mandates

The intricate landscape of regulatory requirements demands that organizations develop robust internal control systems capable of adapting to evolving legal frameworks. These systems must not only prevent potential violations but also provide comprehensive documentation and transparent reporting mechanisms that demonstrate ongoing compliance and organizational accountability.

Use this reference table for key regulatory areas and example standards organizations must meet:

Compliance Domain | Common Standard | Typical Requirement |

Data Protection | GDPR, HIPAA | Secure personal data |

Financial Reporting | SOX, SEC | Accurate financial disclosure |

Industry Specific | Banking, Healthcare, Tech | Sector-specific controls |

Successful regulatory compliance is not about mere checkbox exercises but creating a proactive culture of risk management. Internal auditors play a crucial role in bridging organizational practices with regulatory expectations, ensuring that control mechanisms are not just implemented but continuously refined and aligned with emerging legal standards.

Pro tip: Develop a dynamic compliance tracking system that allows real-time monitoring and immediate reporting of potential regulatory deviations.

Risks, Costs, And Common Weaknesses In Control Systems

Internal control weaknesses represent significant organizational vulnerabilities that can expose businesses to substantial financial and reputational risks. Identifying control system deficiencies is crucial for maintaining operational integrity and preventing potential financial misconduct.

Common internal control weaknesses typically manifest in several critical areas:

Operational Vulnerabilities

Inadequate segregation of duties

Insufficient authorization procedures

Limited management oversight

Technical Deficiencies

Outdated technological infrastructure

Weak cybersecurity protocols

Ineffective access management systems

Administrative Gaps

Incomplete documentation processes

Inconsistent policy enforcement

Poor risk assessment methodologies

The potential costs associated with these weaknesses extend far beyond immediate financial implications. Organizations can face significant consequences, including regulatory penalties, reputational damage, increased audit expenses, and potential legal liabilities. These risks underscore the importance of developing comprehensive, dynamic internal control frameworks that can adapt to evolving organizational and regulatory landscapes.

Effective risk mitigation requires a proactive approach that goes beyond simple compliance. Internal auditors must continuously assess control systems, identifying potential vulnerabilities and implementing strategic improvements. This involves not just detecting weaknesses but understanding their root causes and developing systematic solutions that address underlying organizational challenges.

Pro tip: Implement a continuous monitoring system that provides real-time insights into potential control weaknesses and enables immediate corrective action.

Strengthen Your Internal Controls Knowledge with Expert Training

Auditors face mounting challenges in designing and evaluating effective internal controls that ensure financial accuracy and regulatory compliance. As highlighted in the article, understanding frameworks like COSO and mastering preventive, detective, and corrective controls are critical to mitigating operational risks and avoiding costly weaknesses. Without continuous education, staying ahead of evolving regulatory demands and emerging control deficiencies can feel overwhelming.

Take control of your professional growth now by exploring comprehensive courses and seminars at Compliance Seminars. Gain practical insights on internal control frameworks, risk assessment, and compliance standards from instructors with Big 4 experience. Whether you prefer live webinars or in-person events, our trainings fulfill CPE requirements for CPA, CIA, CISA, and CFE certifications. Do not wait until vulnerabilities threaten your organization. Visit Compliance Seminars today and empower yourself with the knowledge to identify weaknesses, implement effective controls, and elevate your auditing impact.

Frequently Asked Questions

What are internal controls and why are they important for auditors?

Internal controls are systematic frameworks that organizations implement to protect resources, ensure financial reporting accuracy, and maintain regulatory compliance. For auditors, effective internal controls are essential as they help identify and mitigate risks, ensuring the integrity of financial statements and organizational operations.

How does the COSO framework relate to internal controls in auditing?

The COSO framework offers a structured approach to internal controls through five interconnected components: control environment, risk assessment, control activities, information and communication, and monitoring. Auditors rely on this framework to evaluate the effectiveness of internal controls and assess organizational risk management practices.

What types of internal controls should auditors focus on during their assessments?

Auditors should focus on three main types of internal controls: preventive controls, which block risks before they occur; detective controls, which identify existing issues; and corrective controls, which address and resolve problems once detected. A balanced approach incorporating all types is crucial for effective auditing.

How can internal control weaknesses impact an organization during audits?

Weaknesses in internal controls can expose organizations to financial misconduct, regulatory penalties, and reputational damage. Auditors must identify these weaknesses to enhance risk management and ensure compliance with regulations, thus safeguarding the organization against potential losses.

Recommended

Comments