Understanding the role of ethics in auditing for professionals

- John C. Blackshire, Jr.

- Mar 21

- 8 min read

Updated: Mar 31

Auditor objectivity is often assumed to be absolute, but the reality is far more complex. Ethics in auditing extends beyond following rules to actively managing biases, navigating conflicts, and maintaining integrity under commercial pressure. As regulatory scrutiny intensifies and stakeholder expectations grow, audit professionals must understand how ethical principles directly impact audit quality, credibility, and professional standing. This guide explores the foundational ethical standards auditors rely on, the practical dilemmas they face, and how internal audit functions and compliance frameworks reinforce ethical conduct across organizations.

Table of Contents

Key Takeaways

Point | Details |

Ethics boosts audit quality | Ethical principles increase evidence rigor and consistency, improving audit quality and credibility. |

Objectivity not absolute | Auditors must maintain constant self awareness to manage personal biases and conflicts. |

Lapses incur penalties | Ethical breaches can carry severe penalties even when audit quality remains intact. |

Training reinforces ethics | Ethics training and internal audits help sustain ethical behavior and strengthen effectiveness. |

How ethical principles improve audit quality

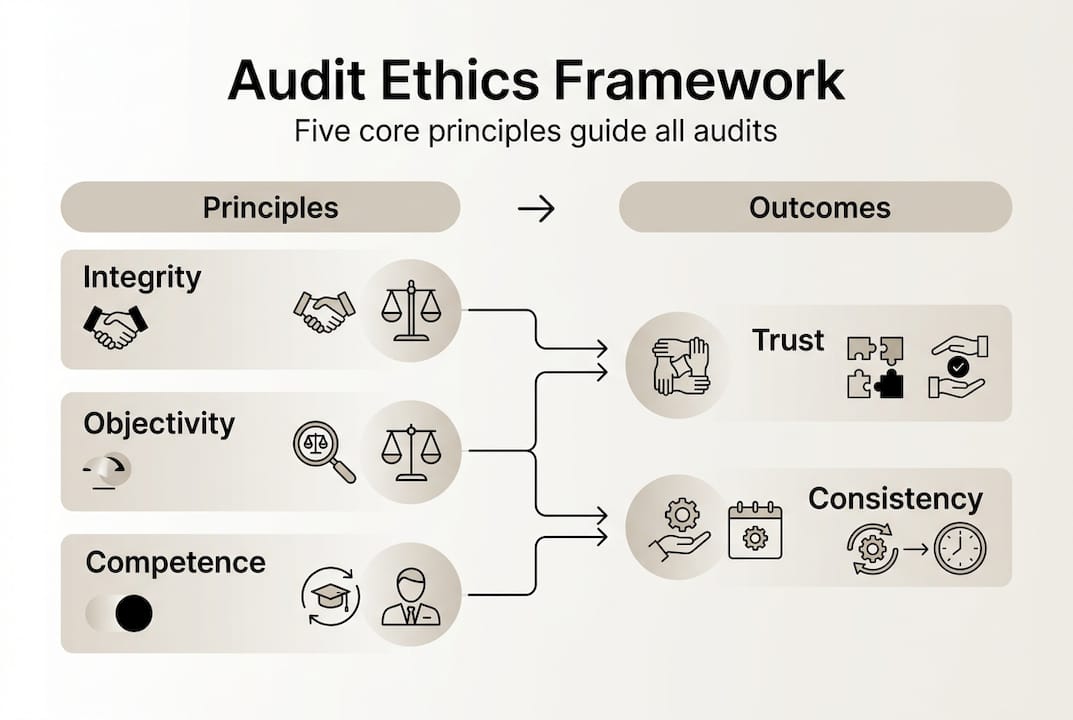

Auditors operate within a framework of five core ethical principles: integrity, objectivity, professional competence and due care, confidentiality, and professional behavior. These principles are not abstract ideals but practical tools that directly enhance the reliability and rigor of audit engagements. When auditors consistently apply these standards, they ensure thorough evidence collection, unbiased evaluation, and transparent reporting that stakeholders can trust.

Research demonstrates that ethical principles enhance audit quality by improving the depth of evidence evaluation and consistency in applying auditing standards across engagements. This consistency matters because it reduces the risk of manipulation, fraud, and selective reporting that can undermine audit credibility. When auditors prioritize integrity, they resist pressure to overlook material issues or adjust findings to satisfy client preferences.

Professional competence requires auditors to maintain current knowledge of standards, regulations, and industry developments. This ongoing learning ensures that auditors can identify emerging risks and apply appropriate procedures to address them. Confidentiality protects sensitive information while professional behavior maintains the reputation of the auditing profession as a whole. Together, these principles create a culture where audit quality is the non-negotiable standard.

Organizations benefit when auditors embed ethical principles into every phase of an engagement. During planning, ethical awareness helps identify potential conflicts of interest or scope limitations. During fieldwork, it guides evidence gathering and professional skepticism. During reporting, it ensures findings are communicated accurately without distortion or omission. Internal auditor basic training programs emphasize these principles as foundational to effective audit practice.

Pro Tip: Revisit ethical standards during audit planning and review sessions to maintain vigilance and ensure team alignment on ethical expectations throughout the engagement.

The practical impact of ethical principles extends beyond individual engagements. When audit firms consistently demonstrate ethical behavior, they build reputational capital that attracts clients, retains talent, and withstands regulatory scrutiny. Audit excellence training programs help firms institutionalize these principles across their practice.

“Ethics in auditing is not about perfection but about creating systematic processes that identify, evaluate, and address ethical risks before they compromise audit quality.”

Objectivity challenges and managing ethical dilemmas in auditing

The pursuit of objectivity is central to auditing, yet complete objectivity is a myth that requires constant self-awareness to manage inherent biases. Auditors bring personal experiences, cognitive shortcuts, and unconscious preferences to every engagement. Recognizing these limitations is the first step toward mitigating their impact on professional judgment.

Common ethical dilemmas auditors face include conflicts of interest when personal relationships or financial incentives create competing loyalties, pressure to overlook findings when clients threaten to change auditors, and confidentiality challenges when legal or regulatory obligations conflict with client expectations. These situations require structured decision-making frameworks rather than relying solely on intuition or past practice.

A practical approach to ethical dilemmas follows these steps:

Identify the ethical issue and stakeholders affected by potential decisions

Assess the impact of each possible action on audit quality, professional standards, and public interest

Consult relevant ethical codes, firm policies, and regulatory guidance to clarify obligations

Escalate to firm leadership or ethics committees when conflicts cannot be resolved at the engagement level

Balancing commercial pressures with ethical principles is particularly challenging in competitive markets where client retention and fee pressure create incentives to compromise. Ethical accounting dilemma guidance emphasizes that accountants must prioritize integrity and transparency even when it risks business relationships. This balance is not about choosing between ethics and business success but recognizing that long-term credibility depends on consistent ethical behavior.

Pro Tip: Develop a formal escalation path and ethical decision framework within your audit team so that dilemmas are addressed systematically rather than left to individual judgment under pressure.

Soft skills play a crucial role in navigating ethical challenges. Communication skills help auditors articulate concerns without creating unnecessary conflict. Emotional intelligence enables recognition of when personal biases or client pressure are influencing judgment. Critical thinking supports evaluation of complex situations where ethical obligations may not be immediately clear. Auditor soft skills webinar programs address these competencies as essential complements to technical expertise.

Organizations can support auditor objectivity by implementing rotation policies, conducting independent quality reviews, and creating cultures where raising ethical concerns is encouraged rather than penalized. When auditors feel supported in making difficult ethical decisions, they are more likely to maintain objectivity even under significant pressure. Soft skills for auditors training reinforces these capabilities.

“The most dangerous ethical failures occur not when auditors consciously choose to compromise but when they fail to recognize that compromise is happening.”

The role of internal audits and compliance in fostering ethical conduct

Internal audit functions serve as critical mechanisms for detecting unethical behavior and promoting ethical norms within organizations. Empirical studies show that internal audits promote ethical behavior and effectiveness through learning exchanges and relational trust among work unit members. This influence extends beyond compliance monitoring to actively shaping organizational culture.

Internal auditors foster ethical conduct by:

Providing independent assessments that identify control weaknesses and ethical risks before they escalate

Facilitating learning opportunities where employees understand the rationale behind ethical standards

Building relational exchanges that create trust and open communication about ethical concerns

Modeling ethical behavior through their own adherence to professional standards

Compliance frameworks reinforce auditor ethics by establishing clear expectations and consequences for ethical breaches. In group audits, all component auditors must comply with ethical standards including independence requirements. Failures to meet these standards can result in fines even when audit quality itself is not questioned, emphasizing that ethics compliance is a standalone regulatory priority.

The distinction between internal and external audit responsibilities highlights different ethical emphases:

Dimension | Internal audit | External audit |

Primary focus | Operational improvement and risk management | Financial statement accuracy and compliance |

Ethical emphasis | Fostering organizational ethical culture | Maintaining independence from management |

Stakeholder accountability | Management and board | Shareholders and public interest |

Ethical risk | Organizational capture and loss of objectivity | Client pressure and fee dependence |

Organizations benefit ethically and operationally when internal audit functions have appropriate independence, adequate resources, and direct reporting lines to audit committees. These structural elements protect auditors from pressure to compromise ethical standards in favor of operational convenience or management preferences. Internal auditing 101 basics training emphasizes these organizational dynamics.

Internal auditors can enhance their ethical impact by adopting change management principles that engage stakeholders rather than simply issuing findings. Using Saul Alinsky’s principles in internal audits demonstrates how auditors can foster ethical change by building coalitions, understanding power dynamics, and creating sustainable improvements rather than superficial compliance.

Navigating limitations: when ethical proclamations may falter

Ethics statements and corporate social responsibility reports are increasingly common, yet research reveals a troubling pattern. Studies show that CSR reporting firms exhibit higher misbehavior rates both before and after issuing ethics proclamations, suggesting these statements may legitimize rather than prevent misconduct. This finding challenges auditors to look beyond surface-level ethics declarations when assessing organizational integrity.

The phenomenon occurs because ethics proclamations can create a halo effect where stakeholders assume ethical behavior without demanding evidence. Organizations may use ethics statements strategically to deflect scrutiny while actual practices remain unchanged or even deteriorate. For auditors, this means that formal ethics policies, codes of conduct, and CSR reports cannot substitute for rigorous evidence gathering and professional skepticism.

Auditors must apply critical judgment when evaluating ethical compliance:

Verify ethics claims through observation, testing, and corroboration rather than accepting declarations at face value

Assess whether ethics programs have substantive implementation or exist primarily for public relations purposes

Identify gaps between stated ethical commitments and actual organizational behavior or incentive structures

Evaluate whether ethics violations result in meaningful consequences or are overlooked when inconvenient

Maintaining professional skepticism in ethics evaluation is essential because management has strong incentives to present favorable ethics narratives. Auditors who assume good faith based on ethics statements risk missing material issues that could affect audit conclusions. This skepticism should be calibrated rather than cynical, recognizing that many organizations genuinely pursue ethical improvement while remaining alert to those that do not.

Pro Tip: Incorporate ethics risk assessments as part of audit planning to identify and address possible ethics gaps before they compromise the engagement or organizational performance.

The implications extend to how auditors communicate findings. When ethics proclamations exist alongside evidence of misconduct, auditors face difficult decisions about how directly to address the disconnect. Diplomatic communication that preserves working relationships must be balanced against the obligation to report material issues clearly. Develop CPE training program resources help auditors build these communication skills.

Understanding these limitations does not diminish the value of ethics in auditing but reinforces that ethics requires ongoing vigilance rather than one-time declarations. Auditors who recognize this reality are better positioned to identify genuine ethical risks and contribute to meaningful improvements in organizational conduct.

Enhance your auditing ethics with expert training

Navigating the ethical complexities of modern auditing requires more than good intentions. It demands specialized knowledge, practical frameworks, and ongoing skill development that keeps pace with evolving standards and emerging risks. Continuing professional education focused on ethics equips auditors with tools to recognize dilemmas, apply decision frameworks, and maintain integrity under pressure.

Specialized ethics CPE courses provide practical training in ethical decision-making, compliance requirements, and risk management tailored to audit professionals. These programs go beyond theoretical principles to address real-world scenarios where ethical choices have immediate consequences for audit quality and professional credibility. Regular upskilling ensures auditors maintain the competence required for credible, high-quality audits that meet regulatory expectations.

Whether you are building foundational skills or deepening expertise in specific ethical challenges, internal auditor basic training and advanced programs offer pathways for professional growth. Access a comprehensive 2026 CPE event calendar featuring in-person seminars and webinars across multiple cities, designed to fit your schedule while delivering the practical insights you need to excel in today’s demanding audit environment.

Frequently asked questions

What is the role of ethics in auditing?

Ethics in auditing ensures that auditors maintain integrity, objectivity, and professional behavior throughout engagements, which directly enhances audit quality and stakeholder trust. Ethical principles guide evidence evaluation, reporting accuracy, and resistance to client pressure that could compromise findings.

How do auditors maintain objectivity when facing conflicts of interest?

Auditors maintain objectivity by recognizing personal biases, following structured decision frameworks, and escalating conflicts to firm leadership or ethics committees when needed. Formal policies like engagement rotation and independent quality reviews provide additional safeguards against compromised objectivity.

Why are ethical lapses penalized even when audit quality is not questioned?

Regulatory bodies treat ethics compliance as a standalone priority because ethical standards protect public trust in the auditing profession beyond individual engagement quality. Violations demonstrate systemic risks that could affect multiple engagements and undermine confidence in audit reliability.

How do internal audits promote ethical behavior in organizations?

Internal audits foster ethical behavior by creating learning opportunities, building relational trust, and providing independent assessments that identify ethical risks before they escalate. This proactive approach shapes organizational culture rather than simply detecting violations after they occur.

Can ethics training improve audit effectiveness?

Ethics training improves audit effectiveness by equipping auditors with frameworks to navigate dilemmas, recognize biases, and apply professional skepticism consistently. Regular training ensures auditors maintain current knowledge of standards and develop the judgment required for complex ethical decisions.

Recommended

Comments