Internal vs external controls explained: a guide for auditors

- John C. Blackshire, Jr.

- May 15

- 11 min read

TL;DR:

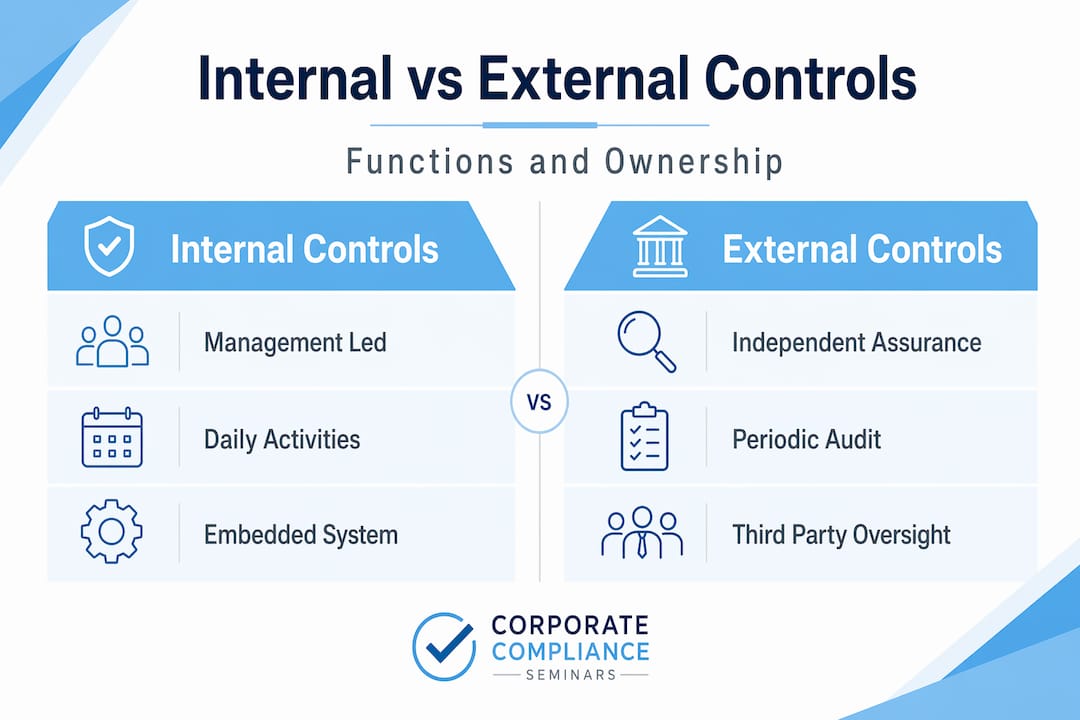

Internal controls are management-owned policies and procedures embedded in daily operations, not performed by auditors. External controls, such as audits, are independent evaluations that provide assurance but do not manage controls. Combining continuous monitoring with periodic audits enhances risk management and ensures control effectiveness.

Audit and compliance professionals face a persistent confusion that quietly undermines control frameworks: the belief that internal controls are either the same as an audit or that external audits replace them. They are not the same, and neither replaces the other. Understanding the internal vs external controls explained distinction is foundational for anyone designing control environments, assessing risk, or navigating regulatory requirements. Internal controls are owned by management, not by auditors. External audits evaluate them. That distinction sounds simple, but its practical implications run deep.

Table of Contents

Defining internal controls: management’s embedded risk management system

Understanding external controls: independent assurance through audits

Monitoring internal controls versus auditing controls: operational distinctions

Auditor’s assessment of internal controls: design, implementation, and operating effectiveness

Common misconceptions and challenges in internal and external control integration

Applying internal vs external controls for effective risk management and compliance

Why viewing internal and external controls as partners—not substitutes—improves audit outcomes

Explore expert CPE training to master internal and external controls

Key Takeaways

Point | Details |

Internal controls ownership | Internal controls are management-owned embedded processes to reduce risk and ensure compliance. |

External controls role | External controls consist of independent audits providing assurance over financial statements. |

Audit assessment stages | Auditors assess control design, implementation, and test operating effectiveness when relying on controls. |

Monitoring vs auditing | Monitoring is continuous management activity; auditing is periodic independent evaluation. |

Limitations exist | Internal controls provide reasonable but not absolute assurance due to inherent risks like override and collusion. |

Defining internal controls: management’s embedded risk management system

Internal controls are not a department. They are not a checklist you hand to your external auditor once a year. Internal controls are the policies, procedures, and checks embedded in an organization’s operations to protect assets, support reliable financial reporting, and ensure compliance with laws and regulations.

Management designs, implements, and maintains them. That ownership is non-negotiable. When something breaks in the control environment, management answers for it first.

The COSO framework remains the professional standard for organizing internal controls into five components:

Control environment: The foundation of tone, values, and accountability set by leadership

Risk assessment: Management’s process of identifying and analyzing risks to achieving objectives

Control activities: The specific policies and procedures that address identified risks (approvals, reconciliations, access controls, segregation of duties)

Information and communication: Systems that capture and share relevant information across the organization

Monitoring activities: Ongoing and separate evaluations to assess whether controls remain effective

Understanding why internal controls matter starts here. Controls are designed to provide reasonable assurance, not absolute assurance. Human error, judgment calls, and changing business conditions mean no system is perfect. That qualifier has real consequences for how auditors calibrate their reliance on controls.

Controls fall into three functional types. Preventive controls stop errors before they occur (access restrictions, authorization requirements). Detective controls identify problems after the fact (reconciliations, exception reports). Corrective controls address identified issues and restore proper functioning. Effective control frameworks use all three. Auditors frequently see organizations that invest heavily in preventive controls and neglect corrective ones, which is exactly where control gaps become audit findings.

For practical examples of internal controls in action, consider how a three-way match in accounts payable prevents unauthorized payments before disbursement, while a monthly bank reconciliation detects discrepancies after the fact.

Understanding external controls: independent assurance through audits

External controls, in the audit and compliance context, refer to oversight and assurance activities conducted by parties independent of management. The most significant of these is the external audit, performed by licensed public accounting firms under standards set by bodies like the PCAOB or IAASB.

Here is the critical difference between internal and external controls in this context: internal controls are management-embedded processes, while external assurance is conducted by independent external auditors who provide an opinion on financial statements. External auditors do not manage controls. They evaluate whether the numbers are reliable.

Key characteristics of external controls through auditing include:

Independence: External auditors have no operational role in the organization and must remain free from conflicts of interest

Periodic, not continuous: External audits happen at defined intervals, typically annually, not as a daily oversight mechanism

Assurance-focused: The output is an opinion or report for stakeholders, regulators, or the board, not an operational fix

Scope-bound: External auditors assess what is necessary to form their opinion, not the entirety of internal control design

Standards-driven: Work is governed by professional standards that define what external auditors can conclude and cannot conclude

Understanding internal audit standards alongside external audit requirements reveals an important nuance: both functions evaluate controls, but internal audit is an in-house function aligned with management’s objectives, while external audit serves shareholders, regulators, and the public interest.

How do external controls work in practice? An external auditor arrives, assesses the control environment, selects testing procedures, and ultimately renders an opinion. They rely on the importance of internal controls being well-designed, because strong internal controls reduce the amount of substantive testing needed. Weak controls mean more work, more cost, and greater risk of a qualified opinion.

Monitoring internal controls versus auditing controls: operational distinctions

This is where many professionals conflate two distinct activities that serve different purposes at different intervals.

Continuous monitoring is management’s daily responsibility. In COSO-style frameworks, “monitoring activities” include ongoing evaluations built into routine operations and separate evaluations (such as internal audits) to determine whether controls remain present and functioning effectively. These are two distinct mechanisms, not interchangeable ones.

Ongoing internal control monitoring is a continuous management responsibility, covering transaction reviews, reconciliations, approvals, and exception reporting. Independent internal control audits are periodic evaluations of whether controls are designed and operating effectively. Both are necessary. Neither substitutes for the other.

Here is how to keep the distinction operationally clear:

Daily monitoring examples: Automated system alerts for unusual transactions, supervisory review of journal entries, daily cash reconciliations, access log reviews

Periodic auditing examples: Quarterly internal control assessments, annual SOX compliance testing, internal audit engagements covering specific processes, external auditor walkthroughs

Documentation requirements: Monitoring requires real-time evidence capture (logs, approvals, timestamps). Auditing requires formalized workpapers, testing results, and documented conclusions.

Ownership accountability: Monitoring is owned by process owners and management. Auditing is owned by the audit function, whether internal or external.

Remediation path: Monitoring findings typically trigger immediate management correction. Audit findings generate formal reports with management responses and remediation timelines.

Pro Tip: When assessing a control environment, ask process owners to walk you through what they do every day to keep controls operating. That conversation almost always reveals monitoring gaps that no policy document mentions.

Evaluating internal controls effectively requires understanding both layers. Organizations that monitor well tend to have fewer audit surprises. Those that rely solely on the annual audit to catch problems find those problems arrive with significant business consequences attached.

Auditor’s assessment of internal controls: design, implementation, and operating effectiveness

Professional auditing standards create a structured three-stage framework for how auditors assess internal controls. Understanding this framework is essential for both auditors performing the work and compliance professionals preparing for it.

The three stages are:

Design evaluation: Does the control, if it operates as intended, address the relevant risk? This is a conceptual assessment. An auditor asks whether the control is even capable of preventing or detecting a material misstatement.

Implementation confirmation: Has the control actually been put into place and is it being used? A well-designed control that nobody follows is worthless. Auditors confirm implementation through inquiry, observation, and inspection.

Operating effectiveness testing: Is the control working consistently and correctly over the relevant period? This stage only becomes necessary when the auditor plans to rely on controls to reduce substantive testing under ISA 330.

That third stage is where significant audit effort concentrates in highly controlled environments like financial services or public companies under SOX. If auditors choose not to rely on controls, they skip operating effectiveness testing and go directly to broader substantive procedures.

Characteristic | Control design | Operating effectiveness |

Core question | Is the control logically sound? | Is the control actually working? |

Timing | At planning stage | During fieldwork |

Evidence type | Walkthroughs, documentation review | Sample testing, re-performance |

Failure consequence | Redesign required immediately | Expanded substantive testing |

Responsibility owner | Management | Auditor (testing), Management (fixing) |

A well-documented internal control checklist supports all three stages. It helps auditors move efficiently through design and implementation while concentrating testing resources on high-risk areas where control reliance matters most.

The key lesson here: control existence does not equal control operation. I have seen organizations with elaborate control documentation where the actual control activity had quietly stopped occurring months earlier. That gap between paper and practice is precisely what operating effectiveness testing is designed to uncover.

Common misconceptions and challenges in internal and external control integration

The most costly misconceptions in this space are not technical. They are conceptual.

Misconception one: internal controls “are the audit” or “produce the audit opinion.” They do not. Auditors evaluate controls. Management owns and operates them. Conflating these two roles creates accountability gaps where neither side feels fully responsible for control quality.

Several other persistent misconceptions and real risks deserve attention:

Assuming documentation equals operation: Written policies confirm intent, not execution. Auditors who rely heavily on documentation without testing actual transactions miss operating failures regularly.

Underestimating management override risk: Management can circumvent even well-designed controls. No control environment is immune. The stronger the tone at the top, the lower this risk, but it never disappears entirely.

Collusion defeats segregation of duties: Two employees working together can neutralize a segregation of duties control entirely. This is an inherent limitation no control design fully eliminates.

Ignoring corrective controls: Organizations that focus exclusively on preventive and detective controls leave themselves without a reliable mechanism to address failures when they occur.

Treating residual risk as zero after controls: Controls reduce risk to a residual level. That level is never zero. Audit conclusions must account for what remains after controls operate.

Pro Tip: When reviewing why internal controls fail, look first at changes in personnel, system migrations, or rapid business growth. These three scenarios consistently produce control breakdowns that neither monitoring nor auditing catches quickly enough.

The audit committee’s role in this landscape is critical. An independent, informed audit committee creates a governance layer that supports both management’s control responsibilities and external auditors’ independence. Without effective audit committee oversight, both sides of the internal-external control equation suffer.

Applying internal vs external controls for effective risk management and compliance

With the conceptual foundation established, the practical application becomes clearer. The difference between internal and external controls in management is not just academic. It drives how you structure your audit approach, communicate findings, and build sustainable compliance programs.

Here is a structured approach to applying this understanding in practice:

Map controls to risk categories: Start with the risk assessment. Every significant control should trace back to a specific identified risk. If it does not, question whether the control serves a current purpose.

Assess design before testing: Investing time upfront in design evaluation prevents wasted testing effort on controls that cannot address the relevant risk regardless of how well they operate.

Coordinate internal and external audit plans: Share audit coverage maps to eliminate redundant testing and fill gaps. External auditors often benefit from internal audit’s deeper organizational knowledge.

Document deficiencies promptly and specifically: Vague findings generate vague responses. Document what failed, when, how often, and what the potential financial impact is. Management needs specificity to remediate effectively.

Communicate throughout the cycle, not just at year end: Waiting until the annual report to surface control concerns is one of the most avoidable audit failures. Timely communication allows management to act before risks materialize.

Revisit control design when the business changes: Updating internal controls as the organization evolves is a management discipline, but auditors should prompt this conversation during planning.

“External assurance and internal controls are not competing systems. They are distinct functions with distinct owners, operating under different standards, serving different audiences. The most effective compliance programs treat them as partners, not substitutes.” (External controls in management context)

Evaluating internal controls with this integrated mindset shifts audit work from reactive testing to genuine risk management. The goal is not just a clean opinion. It is a control environment that actually protects the organization.

Why viewing internal and external controls as partners—not substitutes—improves audit outcomes

Here is a perspective I do not see stated plainly enough in most audit guidance: organizations that treat external audits as their primary control mechanism are systematically underprepared.

I have seen this pattern repeatedly. Management invests minimally in internal controls because “the auditors will catch it.” The auditors arrive, identify gaps, and issue findings. Management patches the findings. The cycle repeats. Nothing structurally improves. This is expensive, reactive compliance theater, and it serves nobody well.

The truth is that strong internal controls are not redundant when external auditors exist. They are what make external audit practical and efficient. When controls are well-designed and consistently operating, external auditors reduce their substantive testing, engagements proceed faster, and audit costs decrease. That is a direct operational benefit to the organization, not just a conceptual virtue.

The independence of external assurance is what gives it credibility with regulators, investors, and lenders. But that independence only produces meaningful conclusions when it is evaluating a control environment that management actually owns and operates. Independence without a functioning internal control system produces expensive opinions of limited assurance value.

The accountability gap I worry most about in practice sits between these two functions: situations where management assumes internal audit or external audit “handled it,” and audit functions assume management “fixed it.” Neither assumption gets tested. Understanding why internal controls fail almost always reveals this gap.

The highest-performing audit functions I have encountered treat internal controls and external assurance as genuinely complementary. Internal audit functions as a continuous improvement partner to management, testing controls throughout the year and surfacing issues early. External auditors arrive with a clear, well-controlled environment that lets them focus their professional judgment where it matters most. Both sides are better for it, and the organization carries less residual risk. That is what understanding audit standards in practice actually looks like.

Explore expert CPE training to master internal and external controls

If this guide clarified how internal controls and external assurance fit together, the next step is applying that clarity in your day-to-day audit and compliance work. Developing that applied skill takes more than reading. It takes structured, standards-based training from professionals who have done this work at the highest levels.

Compliance Seminars offers CPE-accredited training designed specifically for auditors, compliance officers, and risk managers who need more than theory. The 2026 in-person CPE event calendar includes engagements across multiple U.S. cities covering internal control assessment, SOX compliance, and auditing standards. For those who prefer live online instruction, internal auditor CPE webinars cover practical audit methodology in focused, applicable sessions. For professionals specifically working with the COSO framework, our COSO framework training course bridges framework theory with real audit and compliance application. All programs qualify for NASBA-recognized CPE credit.

Frequently asked questions

What is the main difference between internal and external controls?

Internal controls are management-implemented policies and procedures embedded in daily operations to manage risk, while external controls refer to independent assurance activities like external audits that provide validation of financial statements to stakeholders and regulators.

Why do auditors test operating effectiveness of controls?

Auditors test operating effectiveness when they plan to rely on controls to reduce substantive testing, confirming that controls are not only designed appropriately but also functioning consistently in practice throughout the audit period.

How does monitoring differ from auditing internal controls?

Monitoring is a continuous management responsibility embedded in daily operations, while auditing is a separate, periodic evaluation performed independently to verify whether controls are properly designed and actually operating effectively over time.

Can internal controls eliminate all risks?

No control system eliminates all risks because inherent limitations like management override and collusion exist in every organization, meaning controls provide reasonable assurance only, never absolute assurance.

How do internal audit and internal controls differ?

Internal controls are management processes that mitigate operational and financial risk, while internal audit is an independent function that evaluates whether those management-owned controls are properly designed and operating effectively across the organization.

Recommended

Comments