Audit documentation best practices: The professional's guide

- John C. Blackshire, Jr.

- May 17

- 9 min read

TL;DR:

Poor audit documentation often results from misusing it as a post-fieldwork task rather than an active process integrated into engagement execution.

Compliance with standards like PCAOB AS 1215 and ISA 230 requires detailed, self-contained workpapers that enable an experienced auditor to understand without follow-up.

Meeting strict deadlines and establishing real-time documentation habits are crucial for maintaining audit quality and defending files during regulatory inspections.

Poor audit documentation is rarely about carelessness. Most auditors who struggle with it are simply working under the wrong model — treating documentation as a post-fieldwork task rather than an active part of the engagement. That misalignment is at the root of most audit documentation best practices failures, and it tends to surface at the worst possible time: during regulatory inspection or litigation. This guide will walk you through the formal standards that govern documentation, the critical 2026 deadline changes you need to know, and the practical habits that separate defensible audit files from ones that invite scrutiny.

Table of Contents

Understanding audit documentation requirements and standards

Navigating deadlines and retention: Meeting 2026 PCAOB and ISA timelines

Integrating documentation into audit workflows for real-time quality

Auditing internal audits: Aligning documentation with risk and planning

Why audit documentation is the new foundation of audit quality and trust

Explore expert training to master audit documentation best practices

Understanding audit documentation requirements and standards

Audit documentation doesn’t exist in a vacuum. Two primary frameworks govern what your files must contain and how they must be organized: PCAOB AS 1215 for public company audits in the United States, and ISA 230 (International Standard on Auditing 230) for international engagements. Knowing which standard applies to your engagement is step one. Understanding what each demands is where effective audit documentation begins.

PCAOB AS 1215 requires documentation that goes well beyond “here’s what we did.” The standard specifies that AS 1215 requires sufficient detail) to understand the purpose, source, and conclusions drawn, with organized links to significant findings. That last part matters. A workpaper that notes a conclusion without tracing back through the evidence chain is incomplete by definition, even if the conclusion itself is correct.

ISA 230 takes a similarly outcome-focused approach. The standard’s practical test is whether an experienced auditor without prior engagement connection can understand the file, emphasizing timely preparation. This “experienced auditor test” is one of the most useful internal quality checks you can apply to your own files before submission. Ask yourself: if someone competent picked this up cold, would they follow it without calling me?

Here’s what both standards require in practice:

Clear identification of each workpaper: engagement name, period, preparer, reviewer, and date

Purpose and objective: what the procedure was designed to accomplish

Source of evidence: where the data, confirmations, or samples came from

Work performed: specific steps taken, sampling criteria, and scope

Findings and exceptions: everything noted, including items resolved as immaterial

Conclusions: a clear statement linking back to the audit objective

A ready-to-use audit documentation checklist can help your team ensure each file element is present before sign-off, especially on complex engagements where multiple team members contribute to a single workpaper.

Navigating deadlines and retention: Meeting 2026 PCAOB and ISA timelines

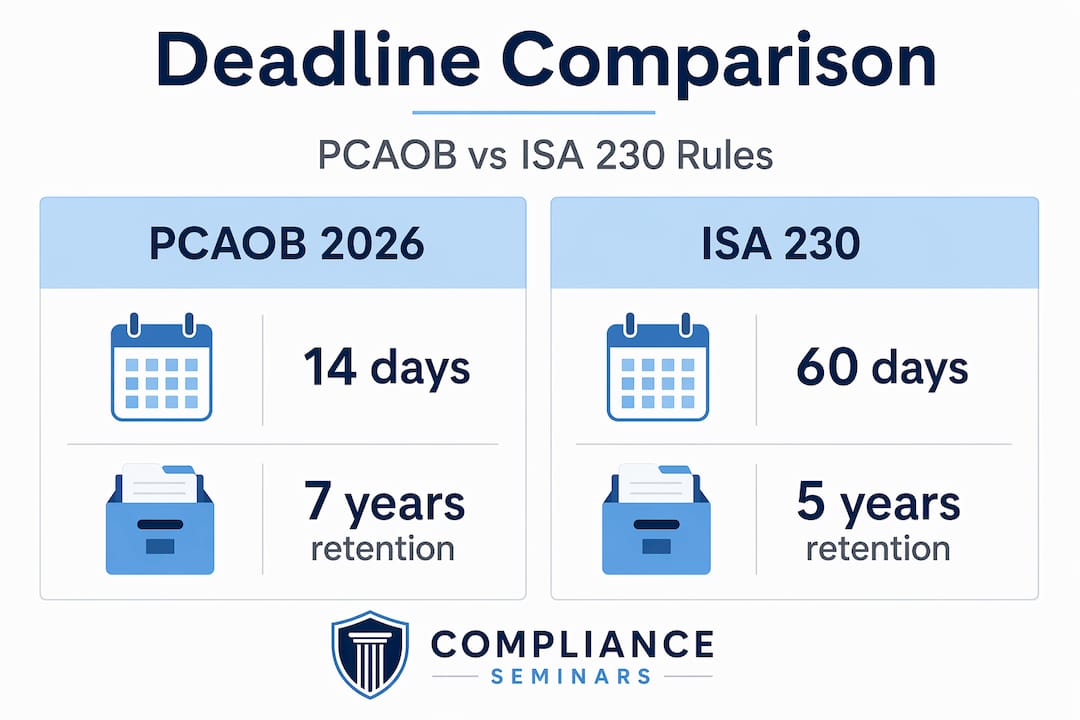

With the standards established, the next pressure point is time. The PCAOB made a significant change effective 2026 that many audit teams are still adjusting to: final audit documentation assembly is now required within 14 days after report release, reduced from the previous 45-day window. That is not a small adjustment. It fundamentally changes how you sequence fieldwork, evidence collection, and supervisory review.

By comparison, ISA 230 allows up to 60 days after the auditor’s report date for final file assembly. For firms operating under both frameworks, the operational difference is substantial.

Framework | Assembly deadline | Retention period |

PCAOB AS 1215 (2026) | 14 days post-report release | 7 years (issuers) |

ISA 230 | 60 days post-report date | 5 years (varies by jurisdiction) |

AICPA (nonissuers) | 60 days post-report release | 5 years |

Retention is equally important. For PCAOB audit standard timelines, public company files must be retained for seven years. Nonissuers under AICPA standards carry a five-year retention floor. Both figures assume no litigation hold or regulatory request requiring extended preservation.

Key retention and deadline practices to implement now:

Set an internal assembly deadline of 10 days post-report to build in a 4-day buffer under PCAOB

Confirm your document management system timestamps evidence attachment dates automatically

Maintain a retention schedule mapped to each engagement type and governing framework

Flag engagements under regulatory review or litigation for indefinite hold procedures

Pro Tip: Don’t wait for the report release date to start assembly. Final documentation is often 80% complete before the report is signed. Treat the last 20% as a closing procedure, not a separate task.

Building self-contained and defensible audit documentation

Deadlines set the boundary conditions. Documentation quality is what determines whether your file holds up when someone looks inside it. The goal is workpapers that are self-contained and clearly linked from objective through procedures, evidence, and conclusion to facilitate experienced auditor understanding without follow-up. That phrase “without follow-up” is the key. If a reviewer has to call you to understand your workpaper, the documentation has already failed its purpose.

Self-contained doesn’t mean long. It means complete. Every workpaper should include a header block with identification details, a stated objective, a description of work performed, attached or referenced evidence, and a written conclusion. The conclusion isn’t a checkbox — it’s a logical statement that connects your evidence to your objective.

Where many auditors fall short is documenting why, not just what. Recording that you performed analytical procedures on revenue is insufficient. Documenting your expectation, the variance you found, the inquiry you made, how management responded, and your assessment of that response — that is defensible documentation. Documentation must capture alternative explanations, professional skepticism, and resolution of significant matters, not just confirmatory findings.

To build files that withstand scrutiny, follow these structural practices:

Include a brief narrative explaining your judgment on any significant estimate or assumption

Cross-reference related workpapers explicitly rather than relying on general filing structure

Document management representations with the date, source, and your evaluation of their reasonableness

Note items you considered and rejected, particularly when evaluating misstatements or control deficiencies

You’ll also want to check out audit evidence practices for deeper guidance on how evidence gathering and documentation quality intersect.

Pro Tip: Read your conclusion before reading your procedures. If the conclusion makes sense on its own, the workpaper is probably well-structured. If you need the procedures section to understand the conclusion, your documentation logic may need revision.

One more caution: over-documentation can be as problematic as under-documentation. Files bloated with irrelevant exhibits, redundant analyses, and duplicate evidence can obscure the key findings and slow reviewer turnaround. Every document in the file should earn its place.

Integrating documentation into audit workflows for real-time quality

Understanding what good documentation looks like is necessary but not sufficient. You also need a workflow that produces it consistently, especially under accelerated deadlines. With a 14-day documentation assembly deadline, many firms treat workpaper completion as near-real-time processes, attaching evidence as it’s obtained and conducting supervisory review contemporaneously.

The firms that manage this well have stopped thinking of documentation as a separate phase. It is part of fieldwork execution, not a follow-on activity.

Here’s a practical workflow model you can apply immediately:

Attach evidence at the point of receipt. When you receive a confirmation, a data export, or a management schedule, attach it to the relevant workpaper the same day. Batching this task creates backlogs.

Write the preliminary conclusion immediately after performing the procedure. If you later need to revise it based on additional findings, revise it. But capturing the initial conclusion in real time preserves the integrity of your professional judgment at the time.

Schedule supervisory reviews during the engagement. Build interim review milestones into your engagement timeline so that supervisors aren’t reviewing everything at the end. This catches deficiencies early and reinforces documentation quality habits across the team.

Close each section before moving to the next. Leaving multiple open workpapers simultaneously creates completion risk. Treat each section as a closed unit once procedures are done.

Run a pre-assembly self-review at the 10-day mark. Using a standardized checklist, verify that every workpaper has a conclusion, evidence is attached, reviewer sign-offs are complete, and cross-references are accurate.

“The most common audit documentation failures I’ve seen aren’t about what happened in the field. They’re about what wasn’t captured at the time it happened, and reconstructed later under deadline pressure. The result looks like audit work, but it doesn’t hold up under examination.” — Observation consistent with inspection risk findings from practitioners, noting that late documentation and sign-offs create questions about whether effective supervision actually occurred.

Managing these audit documentation timeline challenges requires realistic staffing models that account for documentation time, not just fieldwork time.

Auditing internal audits: Aligning documentation with risk and planning

Beyond external audit, internal audit teams face their own documentation challenges. The most impactful improvement internal auditors can make is linking documentation to the engagement planning and risk assessment process from the start, not as a retrospective exercise.

Internal audit documentation that aligns engagement plans with risk assessments materially improves review efficiency and completeness verification across evidence packages. The logic is straightforward: if every evidence package traces back to a documented risk, reviewers can verify coverage quickly, gaps become visible immediately, and quality assurance is faster and more reliable.

Practical steps to align documentation with risk and planning:

Prepare the risk register before fieldwork begins, not in parallel. It should be a living document that guides evidence selection, not a post-hoc summary.

Map each workpaper to a specific risk or control objective in your engagement plan. This creates traceability from risk assessment through evidence to conclusion.

Use the risk register as a completion checklist during file assembly. If a documented risk has no associated evidence, that is a gap requiring resolution.

Carry over open items from prior engagements into the current risk register when relevant. This prevents recurring issues from going undocumented.

Effective internal audit planning best practices also recommend building documentation expectations into the engagement planning memo, so all team members understand the required format and level of detail before fieldwork starts. This small step eliminates significant rework at the end of the engagement.

Why audit documentation is the new foundation of audit quality and trust

Here is where I want to share a perspective that goes beyond the checklist.

Audit documentation has shifted roles over the past decade. It was once treated as the written record of work already done — important, but secondary to the judgment and expertise that produced it. Today, it functions differently. Documentation is the primary lens through which regulators, quality reviewers, and courts evaluate whether an audit was actually performed with rigor, and whether effective supervision occurred.

The 2026 PCAOB deadline compression is a reflection of this shift, not a cause of it. When regulators reduced the assembly window from 45 days to 14, they were sending a message: if you can’t assemble your file within two weeks, questions arise about whether the work was completed before the report was signed. That is a credibility question, not just an administrative one.

Documentation failures are increasingly treated not as technicalities but as evidence of deeper execution and supervision breakdowns, affecting audit credibility directly. I’ve seen audit teams with strong execution records sustain serious inspection findings because the documentation didn’t reflect what they actually did. The audit was solid. The paper trail wasn’t. And from a regulator’s viewpoint, those two things are the same.

The practical implication is this: documentation quality and audit quality are no longer separable. When you review audit inspection findings trends from PCAOB inspections at Big 4 firms, documentation-related findings consistently appear among the most cited. Not because large firms lack expertise, but because even experienced teams underestimate how much the paper trail matters once the engagement closes.

Build documentation habits that reflect the audit you actually performed, not a summary constructed under deadline pressure. That is what defensibility looks like in practice.

Explore expert training to master audit documentation best practices

Keeping pace with evolving audit documentation standards requires more than good intentions. It requires targeted, structured learning tied to current regulatory requirements.

At Compliance Seminars, we offer CPE training specifically designed for auditors who need to meet the demands of the 2026 PCAOB framework and beyond. Our PCAOB AS 1215 CPE training covers the new assembly deadlines, documentation requirements, and practical workpaper techniques in a format recognized by NASBA. If you prefer live instruction, our 2026 CPE event calendar includes in-person events across multiple U.S. cities. Internal auditors can also access targeted internal auditor CPE webinars covering documentation standards, risk-based planning, and quality assurance. All courses are delivered by instructors with Big 4 experience who understand what inspectors actually look for.

Frequently asked questions

What are the main audit documentation standards I need to follow?

The primary standards are PCAOB AS 1215 for public company audits and ISA 230 for international engagements. Both require that AS 1215 documentation be sufficient) and organized for clear understanding by an experienced auditor.

How soon must the final audit documentation be assembled under the 2026 PCAOB rules?

Starting in 2026, PCAOB AS 1215 requires final assembly within 14 days after the audit report release date, a significant reduction from the prior 45-day window.

What makes audit documentation “self-contained” and why is it important?

Self-contained documentation explains objectives, procedures, evidence, and conclusions fully enough that a well-prepared workpaper allows an experienced auditor to follow the logic without additional questions, which is essential for defensibility during reviews or inspections.

How can internal auditors link documentation to risk assessments effectively?

Prepare your risk register before fieldwork begins and map each evidence workpaper to a specific risk or control objective. Aligning engagement plans and risk assessments significantly improves internal audit review efficiency and reduces gaps in coverage.

Why has audit documentation become a critical factor in audit quality reviews?

Regulators now view documentation gaps as signals of deeper performance or supervision problems, not minor oversights. Documentation failures are treated as indicators of execution breakdowns, making thorough and timely files foundational to credible audit opinions.

Recommended

Comments