Auditor Reporting: Structure, Methods, and Best Practices

- John C. Blackshire, Jr.

- Apr 30

- 10 min read

TL;DR:

Auditor reporting is a critical professional judgment with significant implications for stakeholders.

The standard US report includes specific components like a scope and opinion paragraph, following PCAOB standards.

Effective audits depend on sufficient, reliable evidence and transparent communication of key issues.

Auditor reporting is widely misunderstood. Many compliance professionals treat the auditor’s report as a routine sign-off, a box checked at the end of a financial cycle. That view is costly. As PCAOB guidance confirms, auditor reporting involves issuing a written independent auditor’s report expressing an opinion on whether financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework. That is not a formality. It is a carefully constructed professional judgment with real consequences for investors, boards, regulators, and the public.

Table of Contents

Key Takeaways

Point | Details |

Definition and purpose | Auditor reporting provides an independent opinion on financial statement accuracy for regulatory and stakeholder trust. |

Core report structure | Standard reports follow PCAOB/GAAP format with key sections outlining scope, findings, and auditor opinion. |

Forming audit opinions | Auditors use evidence and rigorous methodology to ensure financial statements are free from material misstatements. |

Role of explanatory paragraphs | Explanatory paragraphs highlight important matters without modifying the audit opinion itself. |

Regulatory oversight impact | PCAOB inspections drive higher reporting standards and accountability for audit quality. |

What is auditor reporting and why does it matter?

Auditor reporting is the formal process through which an independent auditor communicates conclusions about the financial statements of an organization. It is the tangible output of the entire audit engagement, the moment where months of evidence gathering, analysis, and professional judgment converge into a written opinion.

“An auditor’s report is not just a signature on a document. It is an attestation of financial integrity on which markets, regulators, and the public depend.”

The audit opinion itself sits at the heart of this process. But the opinion is only as meaningful as the independence and ethical grounding behind it. Auditors are required to maintain strict objectivity, free from relationships or interests that could compromise their judgment. This is not theoretical. When independence breaks down, the reliability of the entire report collapses. Think of high-profile corporate collapses over the last two decades. In nearly every case, auditor independence was compromised or questioned.

Understanding why audit matters is especially critical in financial services, where the stakes tied to erroneous or misleading reporting are enormous.

Who relies on audit reports?

Investors and shareholders use audit reports to make capital allocation decisions

Regulators such as the SEC use them to monitor market integrity

Company leadership and boards use them to evaluate internal controls and governance

Lenders and creditors use them to assess financial risk before extending credit

Employees and pension fund trustees rely on them for the long-term viability picture

The regulatory reporting importance of structured auditor output cannot be overstated. When reports are clear, timely, and substantive, they drive better decisions across every stakeholder group. When they are vague or formulaic, they erode trust without anyone immediately noticing.

Having established the significance of auditor reports, next we break down their essential components.

The anatomy of a standard US auditor report

A well-structured auditor’s report is not left to personal preference. PCAOB and the pre-reorganized auditing standards framework define the required elements with precision. The standard US report includes a title, addressee, introductory paragraph identifying the statements audited, a scope paragraph describing the nature of the audit, and an opinion paragraph stating whether the financial statements present fairly in conformity with GAAP.

Here is how each section functions in practice:

Title: Must clearly identify the document as the “Independent Auditor’s Report,” signaling the auditor’s objectivity to the reader.

Addressee: Typically addressed to the board of directors or shareholders, establishing who commissioned the audit and to whom the opinion is directed.

Introductory paragraph: Identifies the specific financial statements reviewed, the periods covered, and management’s responsibility for those statements.

Scope paragraph: Describes the nature of the audit, referencing applicable auditing standards and confirming that the audit was planned and performed to obtain reasonable assurance.

Opinion paragraph: States the auditor’s professional conclusion, whether the financial statements present fairly in all material respects in accordance with GAAP.

Auditor’s signature: The firm name and engagement partner’s signature provide accountability.

Date: Signals through-date of the auditor’s responsibility for subsequent events.

Auditor’s address: City and state of the issuing office, supporting transparency and accountability.

Pro Tip: Pay close attention to the date on the auditor’s report. If the date is well after the balance sheet date without explanation, it may signal complications in gathering evidence or subsequent event issues that warrant a closer look.

Unqualified vs. qualified opinions are a common point of confusion. An unqualified (or clean) opinion means the financial statements present fairly with no material exceptions. A qualified opinion signals that, except for a specific matter, the statements are fairly presented. Beyond these, adverse opinions and disclaimers of opinion represent far more serious findings. Knowing the difference is fundamental for any compliance professional reading these documents.

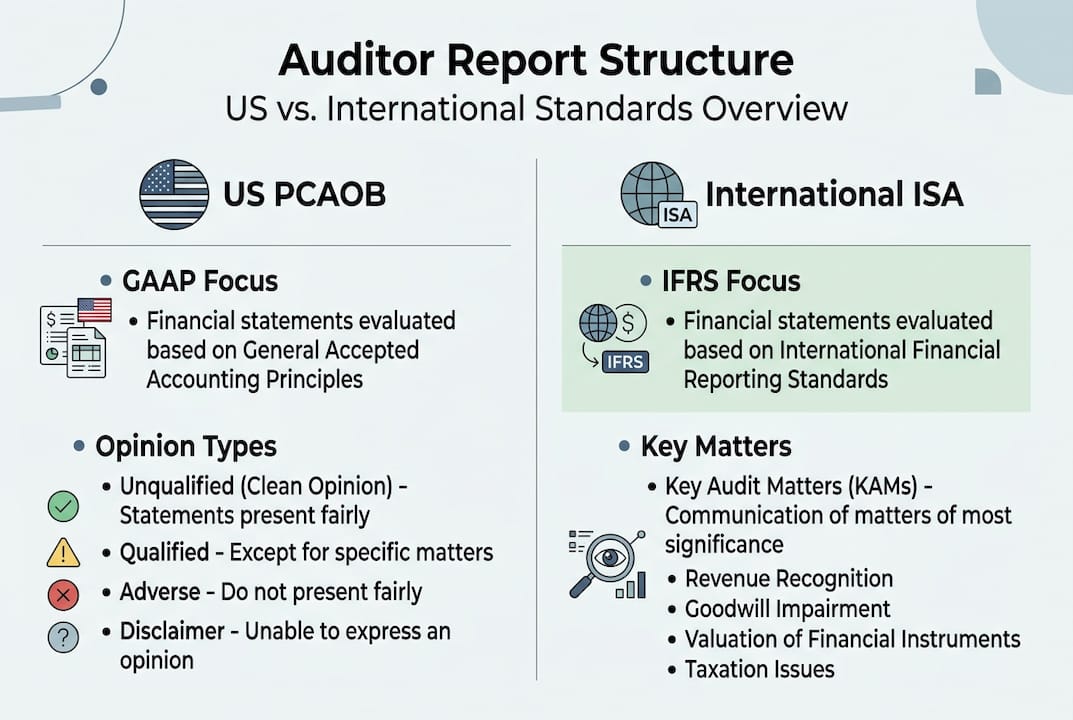

Feature | US PCAOB Standards | International (ISA) Standards |

Primary focus | GAAP conformity and ICFR | Financial statement fair presentation |

Key Audit Matters (KAM) | Required for accelerated filers | Required for listed entities globally |

Internal control reporting | Integrated ICFR audit required | Separate management report, not integrated |

Independence statement | Implied through report structure | Explicitly stated in the report |

Reasonable assurance emphasis | Strong | Strong |

Staying current with PCAOB standard references is especially important given how frequently these standards are cited and tested during inspections. The Big Four 2023 inspection data reveals patterns in which standards are most commonly scrutinized, and audit professionals who know those patterns are better prepared.

With the basic structure of auditor reports clear, the next step addresses how auditors form their opinions.

Forming the auditor’s opinion: Evidence and methodology

The audit opinion is only as strong as the evidence behind it. This is where professional judgment is most visible and most vulnerable. According to PCAOB AS 1105, auditors form their opinion based on sufficient appropriate audit evidence, evaluating whether statements are free from material misstatement due to error or fraud.

What counts as sufficient appropriate audit evidence?

Relevance: The evidence must logically support the assertion being tested

Reliability: Evidence from independent external sources is more reliable than internally generated documents

Sufficiency: The volume and variety of evidence must be enough to support a reasonable conclusion

Documentation: Working papers must clearly record what was gathered, how it was evaluated, and what conclusion it supports

The methodology behind a typical audit opinion involves several structured steps. First, the auditor performs risk assessment procedures to identify areas where material misstatement is most likely. Second, they design substantive procedures and tests of controls tailored to those risks. Third, they gather evidence through inquiry, observation, inspection, confirmation, recalculation, and analytical procedures. Fourth, they evaluate the aggregate findings and form their opinion.

Evidence Type | Reliability Level | Example |

External confirmation | High | Bank confirmation letters |

Auditor-generated | High (if well-designed) | Recalculations of depreciation |

Internal documents | Medium | Management-prepared reconciliations |

Verbal inquiry alone | Low | Informal conversations with staff |

Pro Tip: When reviewing audit working papers or evaluating an audit engagement, check whether reliance on low-reliability evidence (such as inquiry alone) is documented with compensating procedures. Sole reliance on management inquiry, without corroboration, is a consistent finding in PCAOB inspection reports and a red flag for engagement quality. Review engagement metrics analysis for current data on where firms fall short.

Material misstatement assessment involves both quantitative and qualitative dimensions. A misstatement may be small in dollar terms but material if it affects a key covenant, a regulatory threshold, or an executive compensation metric. Auditors must weigh both dimensions carefully.

Common pitfalls in audit evidence include over-reliance on analytical procedures without corroboration, accepting representations from management without independent verification, and failing to adequately document the rationale for conclusions. These are not obscure risks. They appear repeatedly in PCAOB deficiency reports.

Now, let’s address what happens when issues arise or unusual circumstances must be highlighted, which is where the explanatory paragraph comes in.

Explanatory paragraphs: When and why they are included

Not every audit finding warrants a modified opinion. Sometimes an auditor needs to draw attention to a matter without changing the overall conclusion. That is precisely the purpose of the explanatory paragraph, a formal addition to the report that communicates important information while leaving the opinion intact.

PCAOB pre-reorganized standards are explicit: explanatory paragraphs are added for going concern doubt, emphasis of matter, inconsistency with other information, and similar circumstances, without modifying the opinion itself.

“An explanatory paragraph informs without altering. It is the auditor’s way of saying: here is something you need to know, even though it does not change my overall conclusion.”

The most common triggers for explanatory paragraphs include:

Going concern doubt: When substantial doubt exists about an entity’s ability to continue operating for the next twelve months, GAAS and PCAOB standards require disclosure, even within an otherwise clean report. This is one of the most significant signals a reader can receive.

Emphasis of matter: When the auditor wants to highlight a specific issue already disclosed in the financial statements, such as a significant subsequent event or a major accounting policy change.

Inconsistency with other information: When information in a document containing audited financial statements (like an annual report) is materially inconsistent with the audited statements themselves.

Change in accounting principle: When management adopts a new accounting standard or changes a principle, and the auditor concurs, a paragraph noting the change is added.

Other information audited by other auditors: When part of the audit was conducted by a different firm, the principal auditor may include reference to that fact.

Understanding the distinction between an explanatory paragraph and a modified opinion is critical. A qualified opinion changes the conclusion. An explanatory paragraph does not. For professionals reviewing reports on behalf of boards or investors, conflating the two leads to misinterpretation of risk. Reviewing the specific language of an unqualified opinion alongside its explanatory paragraphs gives the full picture.

Lastly, understanding how external oversight and inspections reinforce or challenge the quality of auditor reports ties the process together.

Regulatory oversight: How PCAOB inspections shape auditor reporting

The audit report does not exist in a vacuum. Behind every published opinion is a firm subject to regulatory inspection. The PCAOB’s inspection program is the primary mechanism for holding registered audit firms accountable for the quality of their work.

According to a PCAOB inspection guide, inspections assess audit quality through firm reports that identify deficiencies, with trend data and charts available for both global network and non-affiliate firms. That data tells a sobering story. Deficiency rates in certain high-risk areas, particularly revenue recognition, estimates, and going concern assessments, remain persistently elevated across major firms.

What PCAOB inspectors focus on:

Sufficiency and appropriateness of audit evidence in specific engagement areas

Auditor independence and quality control at the firm level

Compliance with PCAOB auditing standards in both process and documentation

Tone at the top: whether firm leadership genuinely prioritizes audit quality

Engagement partner oversight and review procedures

The practical consequences of deficiency findings are significant. Firms with repeated findings face enhanced oversight, potential restrictions on new client acceptance, and reputational damage that affects their competitive position. For audit professionals, deficiency findings in their engagements can affect career trajectory and licensure.

Reviewing deficiency trends in inspections from the 2023 Big Four cycle reveals specific areas where firms consistently fall short. Revenue testing, management’s use of estimates, and internal control over financial reporting remain at the top of the deficiency list. Separately, industry-specific inspection issues show that financial services, real estate, and technology sectors generate disproportionately high deficiency rates.

For compliance professionals supporting external audit activities, understanding inspection findings is not optional. It shapes the questions you should be asking your external auditors and the benchmarks you apply when evaluating engagement quality.

A fresh perspective on audit reporting: Process, outcome, and trust

Here is something the standard textbook will not tell you: the audit profession has spent decades perfecting process and has sometimes lost sight of outcome. An audit report that technically complies with every PCAOB standard can still fail its real audience.

I have seen clean opinions issued on companies that subsequently collapsed. The process was followed. The checklists were completed. The working papers were thorough. And yet investors received no meaningful warning because the reporting was procedurally correct but substantively thin. That is the tension that few people in this profession talk about openly.

There is a growing call, particularly from investor advocacy groups, for severity grading in audit opinions, a clearer signal that distinguishes “technically compliant but flagged” from “genuinely sound.” Current binary structures (clean vs. modified) leave too much interpretive work to readers who may lack the sophistication to decode explanatory paragraph language.

What actually builds trust in auditor reporting is not just compliance with the right standards. It is timeliness, specificity, and candid disclosure. Investors do not need more boilerplate. They need to know which risks are real, which estimates are highly uncertain, and where management’s judgment was most aggressively applied.

The profession is capable of delivering that. But it requires audit professionals who are willing to push beyond minimum standards and consider what the report communicates to its actual audience. Improving audit outcomes requires not just technical mastery but a commitment to transparent communication.

Pro Tip: When drafting or reviewing explanatory paragraphs, ask yourself: “Would a sophisticated investor reading this understand what we are actually signaling?” If the answer is no, the language needs work, regardless of whether it meets the technical standard.

Advance your audit expertise with specialized CPE training

Understanding auditor reporting at this level of depth requires more than reading standards. It demands structured, expert-led education that bridges theory and practice.

At Compliance Seminars, we offer internal auditor CPE webinars designed specifically for audit and compliance professionals who need practical, regulation-aligned training. Whether you are building foundational skills through our auditor skills training or advancing into complex PCAOB reporting territory, our curriculum is built around real-world application. Our instructors bring Big 4 experience directly into the classroom, online and in-person. Discover why professionals choose us to meet their CPE requirements and sharpen their professional edge.

Frequently asked questions

What are the core components of an auditor’s report?

A US auditor’s report includes a title, addressee, introductory, scope, and opinion paragraphs, along with the auditor’s signature, date, and address, as defined in PCAOB pre-reorganized standards.

What triggers an explanatory paragraph in an audit report?

Explanatory paragraphs are required under PCAOB standards for issues like going concern doubts, emphasis of matter, or informational inconsistencies, but they do not change the underlying audit opinion.

How do auditors form opinions on financial statements?

Auditors rely on sufficient appropriate evidence gathered through inspection, confirmation, recalculation, and inquiry, evaluating whether financial statements are free from material misstatement due to error or fraud.

Why are PCAOB inspections important for audit quality?

PCAOB inspections identify engagement-level deficiencies and firm-wide quality control gaps, using inspection report data to track trends and enforce accountability across registered audit firms.

What is the difference between US PCAOB and international auditor report standards?

US PCAOB standards require integrated internal control audits and GAAP conformity, while international ISA standards require explicit independence statements and Key Audit Matters disclosures, though both prioritize reasonable assurance over material misstatement.

Recommended

Comments