Streamline your external audit workflow: step-by-step guide

- John C. Blackshire, Jr.

- May 4

- 9 min read

TL;DR:

Effective external audits require a continuous, risk-based workflow supported by thorough documentation and automation strategies. Regular review, data analytics, and ongoing professional development ensure sustained audit quality and compliance with PCAOB standards. Building a flexible, questioning process helps organizations adapt to changing risks and technology, minimizing audit deficiencies and enhancing reliability.

Audit season has a way of exposing every gap you hoped wasn’t there. Missed documentation, unclear ownership of controls, last-minute scrambles to satisfy auditor requests — these aren’t rare edge cases; they’re the predictable result of treating external audits as an event rather than a continuous process. The good news is that a structured, risk-based workflow transforms that chaos into something manageable. This guide walks chief audit executives and compliance officers through every phase of an effective external audit workflow, from preparation through post-audit verification, with practical steps grounded in PCAOB standards, automation strategies, and real-world accountability.

Table of Contents

Key Takeaways

Point | Details |

Start with risk-based planning | Begin your audit with a top-down approach to identify and prioritize high-risk areas per standards. |

Prepare documents and roles | Thorough preparation of documentation and team assignments is crucial for audit success. |

Automate for efficiency | Incorporate automation and analytics to streamline workflows and minimize human error. |

Review and troubleshoot | Regularly review the process for common pitfalls and take corrective action where needed. |

Verify effectiveness | Use post-audit data and analytics to confirm your workflow delivers reliable, compliant results. |

What you need to prepare for an external audit

Before executing anything, you must set the right foundation and assemble all preparation resources. Skipping this step is the single fastest way to create problems that compound later in the audit cycle.

Start with a clear inventory. Identify all significant accounts, financial statement assertions, and relevant process-level controls. Then map each to the corresponding entity-level controls that govern the environment. PCAOB AS 2201 mandates a top-down risk-based approach for integrated audits of financial statements and internal control over financial reporting (ICFR), starting from entity-level controls to significant accounts and assertions. That top-down lens isn’t optional — it defines where your preparation energy belongs.

Preparation checklist: controls, documentation, and team roles

Use the table below as a starting reference. Customize it for your organization’s size, industry, and regulatory context.

Preparation area | What to have ready | Owner |

Entity-level controls | Control matrices, policy documentation, board minutes | CAE / Compliance Officer |

Process-level controls | Walkthroughs, flowcharts, test evidence | Process owners |

Financial documentation | Trial balances, reconciliations, supporting schedules | Controller / CFO |

IT general controls | Access logs, change management records, system documentation | IT Audit Lead |

Prior audit findings | Management responses, remediation status, updated control evidence | Internal Audit |

Engagement logistics | Auditor access credentials, secure data room, NDA agreements | CAE / Legal |

Beyond documentation, the right technology infrastructure matters. Secure document portals, access-controlled collaboration platforms, and version-tracked workpaper tools reduce both risk and friction during fieldwork. A solid risk assessment framework helps prioritize where documentation gaps pose the greatest exposure.

Here is what your preparation team should look like at minimum:

Chief Audit Executive: overall accountability for audit readiness

External audit liaison: single point of contact for the engagement team

Process owners: responsible for providing control evidence by deadline

IT audit support: manages system access and data extraction

Legal and compliance: reviews sensitive disclosures and regulatory items

Pro Tip: Set up a secure, permission-based data room at least four weeks before fieldwork begins. Load all prior-year workpapers, updated control matrices, and key financial schedules there. This one action cuts auditor information requests by a significant margin and signals organizational maturity to the engagement team.

Strong audit management best practices reinforce that preparation is not an administrative task — it is a control activity in its own right. When preparation is treated with that level of seriousness, the rest of the workflow runs smoother.

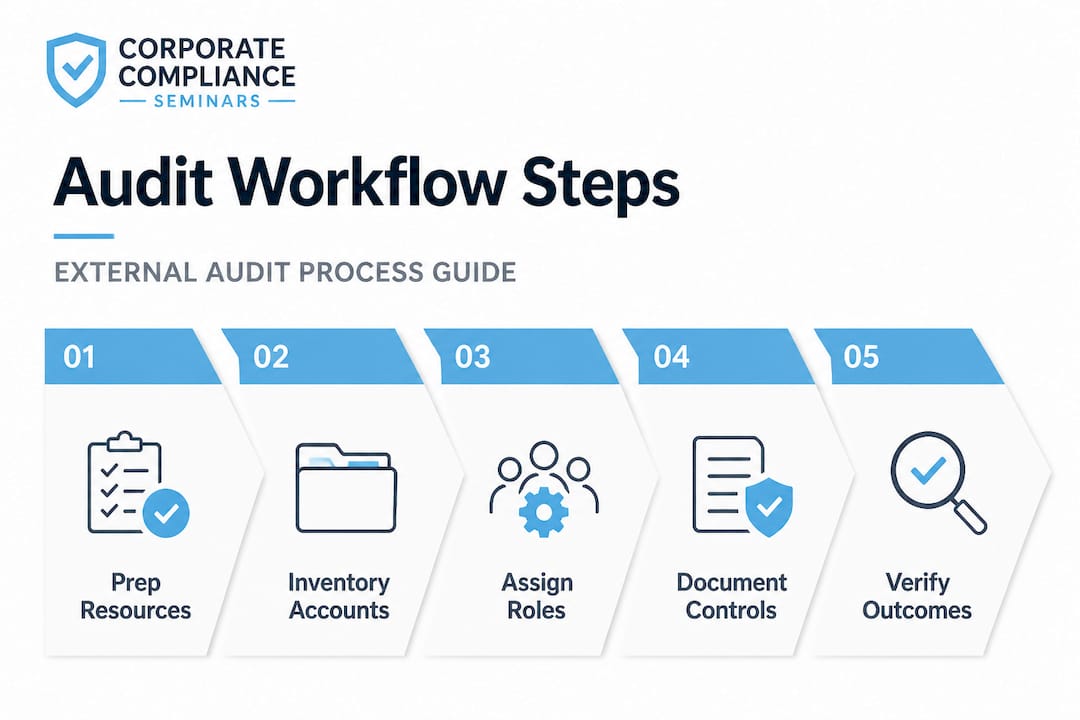

Step-by-step external audit workflow

With preparation complete, you can move confidently into a structured external audit process. Each phase below serves a specific purpose, and each carries compliance obligations that deserve your full attention.

The five-phase workflow

Risk-based planning. This is where scope decisions happen. Review your prior-year audit results, update your entity-level risk assessment, and align scope with the most significant financial statement areas and ICFR controls. Detailed audit planning steps should reflect current-year changes in your business, such as new systems, acquisitions, or changes in key personnel. The planning phase sets the tone — both for the auditors and your internal team.

Engagement launch. Hold an opening meeting with the engagement team. Confirm scope, timelines, communication protocols, and escalation procedures. This is when you clarify materiality thresholds and agree on preliminary audit strategy. Surprises at this stage are acceptable; surprises during fieldwork are not.

Fieldwork execution. Auditors test controls and substantive procedures. Your role is to facilitate, not obstruct. Provide requested documentation promptly, flag any control exceptions early, and keep a log of open requests with assigned owners and due dates. Per PCAOB AS 2201 standards, chief audit executives should prioritize risk-based planning, integrate automation for efficiency, and prepare for common deficiencies like revenue and ICFR through robust data testing.

Review and quality control. Before the draft report is issued, conduct an internal review of all significant findings and management comment letters. This is where you assess the severity of any identified deficiencies and prepare remediation plans. Don’t wait for the final report to start thinking about your response.

Reporting and wrap-up. The audit report is issued, management responses are finalized, and remediation plans are formally documented. Retain all evidence, close the data room securely, and schedule a retrospective with your team to capture lessons learned.

Manual vs. automated audit workflow: a comparison

Workflow step | Manual approach | Automated approach |

Document collection | Email requests, spreadsheet tracking | Automated request management via audit portal |

Control testing | Sample-based, labor-intensive | Continuous control monitoring, larger populations |

Evidence organization | Manual filing, version risk | Centralized workpaper system with version control |

Status tracking | Spreadsheets, status meetings | Real-time dashboards with assigned ownership |

Deficiency reporting | Manually compiled findings lists | Automated flagging and escalation workflows |

Post-audit review | Ad hoc retrospective | Structured analytics with benchmark comparison |

Audit workflow automation is not a futuristic concept. Many organizations already use it to reduce documentation errors and increase testing coverage. The efficiency gains are real, but they require careful implementation to avoid creating new control gaps.

Pro Tip: Build formal review checkpoints at the end of each workflow phase, not just at the conclusion of fieldwork. A brief internal sign-off at the planning stage, mid-fieldwork, and pre-reporting catches misalignments before they become audit findings.

Troubleshooting and common audit workflow pitfalls

Even with a good process, challenges arise. Here is how to avoid and remedy the most common ones that show up in real engagements and PCAOB inspection reports.

The most consistent pattern I see across organizations that struggle with external audits is not a lack of controls. It is a lack of control evidence. You may have strong processes in place, but if the evidence is incomplete, inconsistent, or poorly organized, auditors cannot rely on it. The result is expanded testing, delayed timelines, and findings that could have been avoided.

“Audit failures tied to revenue recognition and ICFR deficiencies remain among the most frequently cited issues in PCAOB inspection reports. Robust data testing is not a best practice — it is a baseline expectation.” This underscores why common deficiencies in Big 4 inspection reports are so instructive for compliance officers planning their next cycle.

Common pitfalls and how to address them

Incomplete documentation: Assign a single owner to every key control with a hard deadline for evidence submission. Use a tracker visible to all stakeholders.

Missed or shallow risk assessments: A risk assessment that hasn’t been updated since last year is not a risk assessment. It is a relic. Refresh it before every audit cycle.

Insufficient data testing: Especially for revenue recognition and ICFR, robust data testing is a non-negotiable standard. Test larger populations using analytics tools rather than relying on small manual samples.

Communication breakdown with the engagement team: Designate a single internal liaison. Multiple points of contact create conflicting messages and slow the process.

Late management responses to findings: Start drafting management responses the moment a finding is verbally communicated — not when the draft report arrives. This buys critical thinking time.

Overlooked IT general controls: Access provisioning failures and change management gaps are recurring sources of material weaknesses. Include IT audit in every workflow phase, not just as an afterthought.

The value of audit analytics in troubleshooting cannot be overstated. When you use data to spot anomalies before auditors do, you shift from reactive to proactive. That shift is the difference between a clean opinion and a difficult conversation with your audit committee.

Verifying audit workflow effectiveness with data and analytics

Now confirm your improved workflow performs to the highest standard by reviewing execution outcomes. This is the phase most organizations skip, which is exactly why the same problems recur year after year.

A structured post-audit workflow review is not the same as a debrief. It is a disciplined, data-supported assessment of whether your process delivered reliable results and where it fell short.

Five-step post-audit verification process

Collect performance metrics. Gather data on auditor request fulfillment time, document rejection rates, number of open findings, and time to close each phase. These are your workflow health indicators.

Compare against prior-year benchmarks. Did your average response time to auditor requests improve? Did the number of repeated findings decrease? Benchmarking workflow performance against prior cycles reveals whether your process improvements actually moved the needle.

Map findings to workflow failures. Every audit finding should trace back to a specific weakness in the workflow. Was it a documentation gap? A missed control test? A communication failure? Mapping findings to root causes prevents superficial fixes.

Assess compliance standard alignment. Review each workflow phase against PCAOB AS 2201 requirements and your organization’s specific regulatory obligations. Integration of automation for efficiency and robust data testing should be visible in your results data.

Update the workflow for the next cycle. Treat the workflow as a living document. Update it based on what the analytics reveal, not on instinct or habit. AI compliance with audit analytics is an emerging area where organizations are beginning to apply machine learning models to verify whether prior control failures were truly remediated.

Pro Tip: Use benchmarking to compare your current workflow performance not just to your own history but to publicly available PCAOB inspection data for your industry. This gives you an external calibration point and helps you set realistic improvement targets.

The analytics step closes the feedback loop. Without it, your workflow is a hypothesis. With it, it becomes a tested, continuously improving system.

The uncomfortable truth about external audit workflows

With the evidence-based approach fully covered, consider this broader perspective on lasting success with external audits.

Here is what most workflow guides do not say: the organizations that struggle most with external audits are not the ones with weak controls. They are the ones with rigid, unchallenged processes that haven’t kept pace with their changing risk environment. A workflow built for 2021 may be genuinely harmful in 2026, especially if your business has scaled, adopted new technology, or entered new regulatory jurisdictions.

Many audit teams treat their workflow as a checklist to complete rather than a system to interrogate. That is a significant error in judgment. The moment you stop questioning whether your workflow still fits your actual risk profile is the moment it starts creating blind spots.

I have seen organizations invest heavily in audit technology — sophisticated platforms, automated testing tools, real-time dashboards — and still produce inconsistent results. The technology was sound. The thinking behind it was stale. Automation amplifies your process. If the process is flawed, automation makes the flaw bigger and faster.

The real discipline is in the review. Not just reviewing what the auditors found, but reviewing how your workflow performed, where your team’s judgment fell short, and what the data is telling you about risk areas you may have underweighted. A strong mastering risk assessment practice is not a one-time activity — it is a continuous professional obligation.

Guidelines and standards are a floor, not a ceiling. PCAOB AS 2201 tells you the minimum expected behavior. The organizations that consistently receive clean opinions and strong audit committee feedback are the ones that treat the standard as a starting point and build judgment, rigor, and honest self-assessment on top of it.

Enhance your audit workflow with leading CPE training

Structured workflows get you started, but sustained workflow excellence requires ongoing learning. The audit standards landscape changes, inspection findings shift in focus, and new technologies reshape what “best practice” means in practice.

If your team is ready to move beyond checklists and build genuine audit workflow competency, compliance-seminars.com offers NASBA-recognized CPE courses and events designed specifically for audit and compliance professionals. From integrated audit standards to automation and analytics, the curriculum is grounded in real-world practice, not theory. Browse the 2026 CPE event calendar to find in-person training in a city near you, or explore Internal Auditor CPE webinars for flexible, targeted professional development that fits demanding schedules. Your workflow is only as strong as the professionals managing it.

Frequently asked questions

What is the top-down risk-based approach in external audits?

The top-down risk-based approach prioritizes entity-level risks and controls, directing auditor attention to areas with the highest likelihood of material misstatement, as required under PCAOB AS 2201. It prevents wasted effort on lower-risk areas while ensuring thorough coverage where it counts.

How can workflow automation improve external audits?

Automation reduces manual errors, accelerates document collection, and enables testing of larger control populations, all of which directly support the efficiency requirements outlined in PCAOB AS 2201. The key is ensuring automation is built on a sound process foundation, not used to mask process weaknesses.

What are the most common deficiencies found in external audit workflows?

Incomplete risk assessments, insufficient documentation, and inadequate data testing — especially around revenue recognition and ICFR — are the most frequently cited deficiencies in PCAOB inspection reports. Addressing these proactively during preparation significantly reduces audit risk.

How do analytics help verify audit workflow effectiveness?

Analytics provide quantitative, cycle-over-cycle feedback on response times, finding rates, and control failure patterns, giving you objective evidence of where your workflow succeeded and where it needs to improve. This transforms post-audit review from a subjective conversation into an actionable, data-supported planning session.

Recommended

Comments